Not financial advice. All figures are for educational reference only. Data verified as at 28 July 2026 unless otherwise noted — see each linked insurer review for its individual fact-check date.

This guide compares Singapore’s top endowment plans side by side — examining guaranteed returns, total projected yields, premium flexibility, and surrender penalties — so you can make an informed decision with your hard-earned savings.

Key Takeaways

- There is no single “best” endowment plan in 2026 — the highest publicly disclosed guaranteed rates currently belong to AIA #Wealth Savvy (IV) and OCBC’s 2-Year Endowment, both at ~2.80% p.a., but both are tranche/campaign-based and can close or change without notice.

- Singlife’s Secure Saver series — the plan that topped this list at 3.40% p.a. guaranteed — is no longer part of Singlife’s live product lineup as at 28 July 2026 (confirmed directly on singlife.com/en/savings). We’ve flagged this clearly in the table below rather than quietly removing it.

- Not every insurer publishes a clean guaranteed % rate. HSBC Life, China Life, and Tokio Marine structure their guarantees as fixed-dollar bonuses or cash benefits instead — see “How Each Insurer’s Guarantee Actually Works” below before assuming their products are worse.

- Guaranteed returns matter most. In a volatile-rate environment, the guaranteed portion of your endowment return is the only number you can truly rely on — illustrated (non-guaranteed) figures assume a 4.25% or 3.00% investment return that isn’t promised.

- We’ve published a full standalone review for all 13 insurers below — each dated, fact-checked against the insurer’s own product pages, and linked directly from the table.

What Is an Endowment Plan?

An endowment plan is an insurance-savings hybrid that pays you a guaranteed lump sum (plus non-guaranteed bonuses) at the end of a fixed term. You pay regular or single premiums, and the insurer invests these funds on your behalf — predominantly in bonds and fixed-income assets.

Unlike pure investment products, endowment plans include a small life insurance component. If you pass away during the policy term, your beneficiaries receive a death benefit (typically 101–105% of premiums paid).

In Singapore, endowment plans are regulated by the Monetary Authority of Singapore (MAS) and offered by licensed insurers. They’re popular for specific financial goals: funding a child’s education, saving for a wedding, or parking medium-term cash.

For a broader overview of how endowments fit into Singapore’s insurance landscape, see our complete endowment plan guide.

How We Ranked the Best Endowment Plans

We evaluated every major endowment plan available in Singapore in 2026 across five criteria:

- Guaranteed yield: The minimum return you’ll receive regardless of market conditions (weighted 30%).

- Projected total return: Guaranteed + non-guaranteed bonuses at the illustrated 4.25% investment return (weighted 25%).

- Premium flexibility: Minimum entry amount, payment frequency options, and top-up features (weighted 15%).

- Surrender value profile: How quickly your policy breaks even if you need to exit early (weighted 15%).

- Insurer financial strength: Capital adequacy ratio and credit ratings (weighted 15%).

Best Endowment Plans in Singapore 2026: All 13 Insurers Compared

We’ve now published a dedicated, fact-checked review of every major life insurer offering endowment or savings-insurance plans in Singapore. Instead of a generic six-plan snapshot, here’s the full picture — 13 insurers, their current flagship plan, and exactly how each one structures its guarantee.

A note on comparability: Not every insurer publishes a clean guaranteed % per annum. Some (HSBC Life, China Life, Tokio Marine) guarantee a fixed dollar amount, a cash-benefit percentage of premium, or nothing beyond capital return — we’ve spelled out exactly what “guaranteed” means for each, rather than forcing every plan into a single column that would misrepresent how they actually work.

| Insurer / Plan | Term | Min. Premium | Guaranteed Return | Review |

|---|---|---|---|---|

| Singlife Secure Saver VII |

2 years | S$5,000 (indicative) | 3.40% p.a. (G) — tranche discontinued, no longer on singlife.com as at Jul 2026 | Full review |

| NTUC Income Gro Saver Flex Pro |

Varies by plan | Varies | Up to 3.38% p.a. (illustrated, 4.25% scenario) | Full review |

| AIA #Wealth Savvy (IV) |

3 years | S$5,000 | 2.80% p.a. (G) — AIA NOW only, limited tranche | Full review |

| OCBC 2-Year Endowment |

2 years | S$5,000 | ~2.80% p.a. (G) — campaign rate, subject to change | Full review |

| Prudential PRUAssure Growth |

3 years | S$5,000 | 1.70% p.a. (G) | Full review |

| Etiqa Enrich flex plus |

Whole-of-life (3-20yr pay) | Varies | Up to 1.65% p.a. guaranteed / 3.95% p.a. total (4.25% scenario) | Full review |

| Manulife Goal 2026 (I) |

2 years | S$5,000 | 1.44% p.a. (G) / 1.60% p.a. (illustrated) | Full review |

| FWD Save Smart Series 9 |

2 years | S$10,000 | 1.60% p.a. (G) — fully subscribed/waitlist as at Jul 2026 | Full review |

| Aviva 3-Yr Single Premium Endowment |

3 years | Varies | ~0.93% p.a. total projected yield (guaranteed + bonus) | Full review |

| Great Eastern GREAT SP |

24 months | S$10,000 | 0.70% p.a. (G) guaranteed survival benefit | Full review |

| HSBC Life Savings Protector II |

10 years (3/5-yr pay) | Varies | No published % — declared bonus ~S$5/S$1,000 (≈0.5% p.a. equivalent) | Full review |

| China Life FlexiCash Growth |

5/10/12 years | Varies | 10% of premium/yr cash benefit from Yr2 — 0% guaranteed return if withdrawn yearly | Full review |

| Tokio Marine TM Nest Egg (II) FlexiSaver |

Up to 30 years combined | Varies | No published % — fixed-dollar GMCP; Par Fund actual return 13.63% (2025, non-guaranteed) | Full review |

(G) = guaranteed rate. (I) = illustrated total return including non-guaranteed bonus at the stated investment-return scenario. Data compiled from TKN’s own dedicated insurer reviews, each individually fact-checked against official insurer sources on its publish date (see each review for its citation date) — reconfirmed as a set on 28 July 2026. Rates on single-premium/tranche-based plans (Singlife, AIA, OCBC, FWD) change frequently or close to new sales entirely; always confirm the current rate directly with the insurer before purchasing.

How Each Insurer’s Guarantee Actually Works

Plans with a clean guaranteed % per annum

AIA #Wealth Savvy (IV), OCBC’s 2-Year Endowment, Prudential PRUAssure Growth, Manulife Goal 2026 (I), FWD Save Smart Series 9, Great Eastern GREAT SP, and Etiqa’s Enrich flex plus all publish a straightforward guaranteed rate per annum. This is the easiest type to compare — and the number in our table above is the floor you’re contractually owed, regardless of how the insurer’s participating fund performs.

Plans with a fixed-dollar or cash-benefit guarantee (not a clean %)

Three insurers structure their guarantee differently, and treating their headline numbers as directly comparable percentages would be misleading:

HSBC Life Savings Protector II doesn’t guarantee a % rate at all. It guarantees a reversionary bonus of roughly S$5 per S$1,000 of cover — which works out to about 0.5% p.a. on the sum insured, based on HSBC Life’s own 2023 and 2024 declared bonus figures.

China Life FlexiCash Growth guarantees a yearly cash benefit equal to 10% of your annual premium from Year 2. That sounds generous, but if you withdraw that cash benefit every year, our own worked calculation (based on China Life’s published maturity formula) shows the guaranteed floor works out to 0% real return — you simply get back what you paid in. The guarantee only grows if you leave the cash benefits to accumulate inside the policy, and China Life doesn’t disclose the credited interest rate on accumulated amounts.

Tokio Marine TM Nest Egg (II) FlexiSaver guarantees a fixed dollar Monthly Cash Payout, not a %. Its non-guaranteed dividend is tied to the insurer’s Par Fund, which has actually returned 8.09% (2023), 7.94% (2024), and 13.63% (2025) — strong recent numbers, but non-guaranteed and not something you can bank on.

A plan that’s no longer available: Singlife Secure Saver

When we reviewed Singlife Secure Saver VII, it offered a genuinely attractive 3.40% p.a. guaranteed. As of 28 July 2026, however, Singlife’s live savings product lineup (singlife.com/en/savings) no longer lists any Secure Saver tranche at all — the short-term, single-premium endowment category has been replaced by products like Singlife Smart Saver and Singlife Heritage Income, which have different structures and haven’t yet been independently reviewed on this site. If you’re specifically looking for what Secure Saver used to offer, check Singlife’s current savings page directly rather than assuming the old rate still applies.

Endowment Plan Returns vs Other Savings Options

How do endowment plans stack up against other places to park your money? Here’s a realistic comparison:

| Savings Option | Typical Return (p.a.) | Lock-In Period | Capital Guaranteed? | Liquidity |

|---|---|---|---|---|

| High-yield savings account | 1.5–2.5% | None | Yes (SDIC insured) | High |

| Fixed deposit | 2.0–2.8% | 6–12 months | Yes (SDIC insured) | Medium |

| Short-term endowment plan | 2.5–3.5% | 2–3 years | Guaranteed component only | Low |

| Singapore Savings Bonds (SSB) | 1.6% (2-yr avg) – 2.1% (10-yr avg) | Up to 10 years | Yes (govt-backed) | High (monthly redemption) |

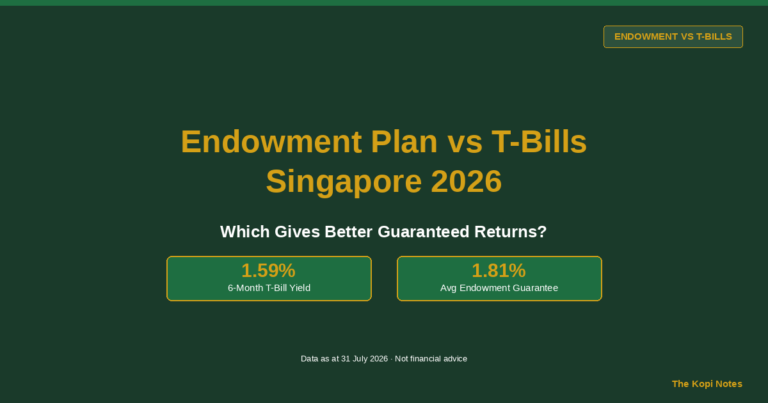

| T-bills (6-month) | ~1.55% (16 Jul 2026 auction) | 6 months | Yes (govt-backed) | Medium |

| STI ETF (ES3/G3B) | ~7% (10-yr avg) | None | No | High |

SSB and T-bill figures updated 28 July 2026 (SSB SBAUG26 tranche via ilovessb.com; T-bill BS26114W auction, 16 Jul 2026) to replace the higher 2025-era estimates previously shown — rates have fallen substantially since mid-2025 as MAS/SORA eased.

The key insight: endowment plans sit in a middle ground. They offer slightly higher guaranteed returns than fixed deposits, but at the cost of significantly reduced liquidity. For most investors, ETFs provide better long-term wealth building, while high-yield savings accounts offer better flexibility for emergency funds.

Who Should Buy an Endowment Plan?

Endowment plans aren’t for everyone. They make sense if you:

Have a specific medium-term savings goal. If you’re saving for a wedding in 3 years or a down payment in 5 years, an endowment plan’s fixed maturity date aligns perfectly with a defined goal.

Struggle with savings discipline. The penalty for early surrender creates a powerful psychological lock-in. If you know you’d dip into a savings account, an endowment plan forces commitment.

Want capital preservation with modest growth. The guaranteed return component means you won’t lose your principal (as long as you hold to maturity), unlike equities or even some bond funds.

Already have adequate emergency funds and insurance. An endowment plan should never be your first financial product. Ensure you have 6 months of expenses in liquid savings and adequate critical illness coverage first.

Who Should Avoid Endowment Plans?

Skip endowment plans if you:

May need the money before maturity. Early surrender penalties are brutal — you could lose 20–40% of premiums in the first year. If there’s any chance you’ll need the cash, a savings account or SSB is safer.

Want to maximise long-term investment returns. For horizons beyond 5 years, low-cost index funds like the CSPX or S&P 500 ETFs have historically returned 8–10% annually — far exceeding any endowment plan.

Are comparing against ILPs. If an insurance agent pitches an investment-linked policy (ILP) as an “endowment alternative,” be cautious. ILPs carry significantly higher fees and market risk with no guaranteed returns.

Common Mistakes When Choosing an Endowment Plan

Mistake #1: Focusing only on projected (non-guaranteed) returns. Insurers illustrate returns at 4.25% and 3.00% investment rates, but actual bonuses can be lower. The 2020–2022 period saw several insurers cut non-guaranteed bonuses. Always anchor your decision on the guaranteed yield.

Mistake #2: Ignoring the opportunity cost. A 3% endowment return over 3 years looks decent in isolation, but compare it against alternatives available during the same period. In 2024–2025, T-bills offered comparable yields with much shorter lock-in periods.

Mistake #3: Over-allocating to endowments. Some Singaporeans put $50,000–$100,000+ into a single endowment plan. This concentrates risk and reduces flexibility. Diversify across multiple instruments — a mix of endowments, SSBs, and ETFs creates a more resilient portfolio.

Mistake #4: Not reading the benefit illustration. Every endowment plan comes with a mandatory benefit illustration (BI) document. Read columns showing guaranteed vs. non-guaranteed values at different policy years. The BI is your single most important document.

How to Buy an Endowment Plan in Singapore

Step 1: Define your goal and timeline. Be specific about how much you need and when. This determines whether you need a 2-year, 3-year, or 5-year plan.

Step 2: Compare guaranteed yields. Use the comparison table above as your starting point. Focus on the guaranteed return column — this is your floor.

Step 3: Check the insurer’s participating fund performance. Look at the insurer’s annual bonus track record. Insurers who consistently meet their illustrated rates are preferable. You can find this data in each insurer’s par fund performance reports.

Step 4: Read the benefit illustration carefully. Pay attention to the surrender value schedule (how much you get back if you exit early) and the death benefit amount.

Step 5: Apply directly or through a trusted advisor. Many short-term endowments can be purchased directly online. For larger or longer-term plans, working with an independent financial advisor can help you negotiate better terms.

The Bottom Line

There’s no longer a single standout “best” endowment plan we can point to with confidence — the plan that used to top this list, Singlife Secure Saver VII, has been discontinued. As at 28 July 2026, the highest publicly disclosed guaranteed rates belong to AIA #Wealth Savvy (IV) and OCBC’s 2-Year Endowment (both ~2.80% p.a.), but both are tranche or campaign-based and can close without warning — check availability directly before assuming either is still open.

For longer horizons, or if none of the currently available tranches appeal, consider whether an endowment plan is truly the best use of your capital — universal life insurance or low-cost ETFs may serve you better.

Whatever you choose, remember: the best financial product is the one that fits your actual situation, not the one with the flashiest projected returns. Start with your goals, compare the guaranteed numbers using our full insurer table above, and only commit money you truly won’t need until maturity.

Looking for a brokerage to start investing in ETFs? Consider platforms like Syfe (code: SRPRFFFCD) for robo-advisory portfolios or Endowus (code: 2V343) for CPF/SRS investing.

Frequently Asked Questions

What is the best endowment plan in Singapore in 2026?

Based on guaranteed returns and overall value, the Singlife FlexiSave 3-year endowment plan offers the best combination of a 2.80% guaranteed yield, digital convenience, and low minimum premium of $10,000 for Singaporeans looking for a short-term savings vehicle in 2026.

Are endowment plans worth it in Singapore?

Endowment plans can be worth it for disciplined short-to-medium-term savings with a specific goal. They offer guaranteed returns that typically beat savings accounts and fixed deposits. However, for long-term wealth building (10+ years), low-cost index funds like ETFs generally deliver significantly higher returns with better liquidity.

What happens if I surrender my endowment plan early?

Early surrender typically results in receiving less than your total premiums paid. In the first year, you may lose 20–40% of your premiums. The surrender value increases each year and usually breaks even by the midpoint of the policy term. Always check your benefit illustration for the exact surrender value schedule.

How are endowment plan returns taxed in Singapore?

In Singapore, proceeds from endowment plans — including both guaranteed and non-guaranteed bonuses — are tax-free for individual policyholders. This is a significant advantage compared to interest income from fixed deposits, which may be taxable if earned overseas.

Can I use CPF or SRS to buy endowment plans?

Some endowment plans are approved for purchase using CPF Ordinary Account (OA) or Supplementary Retirement Scheme (SRS) funds. This can be tax-efficient as SRS contributions enjoy tax relief. Check with the specific insurer for CPF/SRS eligibility — platforms like Endowus (see our referral page linked above) also offer SRS investment options.

What is the difference between an endowment plan and an ILP?

An endowment plan offers guaranteed returns plus potential non-guaranteed bonuses, with your money managed by the insurer’s participating fund. An investment-linked policy (ILP) has no guaranteed returns — your money is invested in unit trusts, and returns depend entirely on market performance. ILPs also carry higher fees (typically 1.5–3% annually). For most people, endowment plans are the safer, more predictable choice. Learn more in our ILP guide, linked earlier in this article.

How do I compare endowment plans from different insurers?

Focus on three numbers from the benefit illustration: (1) guaranteed maturity value, (2) illustrated maturity value at the 4.25% investment return rate, and (3) the surrender value at each policy year. Also compare the minimum premium, premium payment mode (single vs. regular), and the insurer’s historical bonus track record from their par fund reports.

Which insurer currently offers the highest guaranteed endowment rate in Singapore (2026)?

As at 28 July 2026, AIA #Wealth Savvy (IV) and OCBC’s 2-Year Endowment both publicly disclose the highest guaranteed rate among currently marketed plans, at approximately 2.80% p.a. Both are tranche or campaign-based, meaning the rate and availability can change without notice — always confirm the current rate directly with the insurer before applying. Singlife Secure Saver VII previously offered a higher 3.40% p.a. guaranteed but has since been discontinued.

Has Singlife discontinued its Secure Saver endowment plan?

Based on Singlife’s own live savings product page (singlife.com/en/savings, checked 28 July 2026), the Secure Saver series no longer appears in its current lineup. Singlife’s savings range now centres on products like Singlife Smart Saver and Singlife Heritage Income, which have different structures and terms from the short-term, single-premium Secure Saver plans we previously reviewed. If you’re looking for a similarly short-term, single-premium option, compare AIA #Wealth Savvy (IV) or OCBC’s 2-Year Endowment instead.

Get Free Insurance Advice

Speak with a licensed insurance advisor. No obligation, no cost.

By submitting this form, you agree to our Privacy Policy.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.