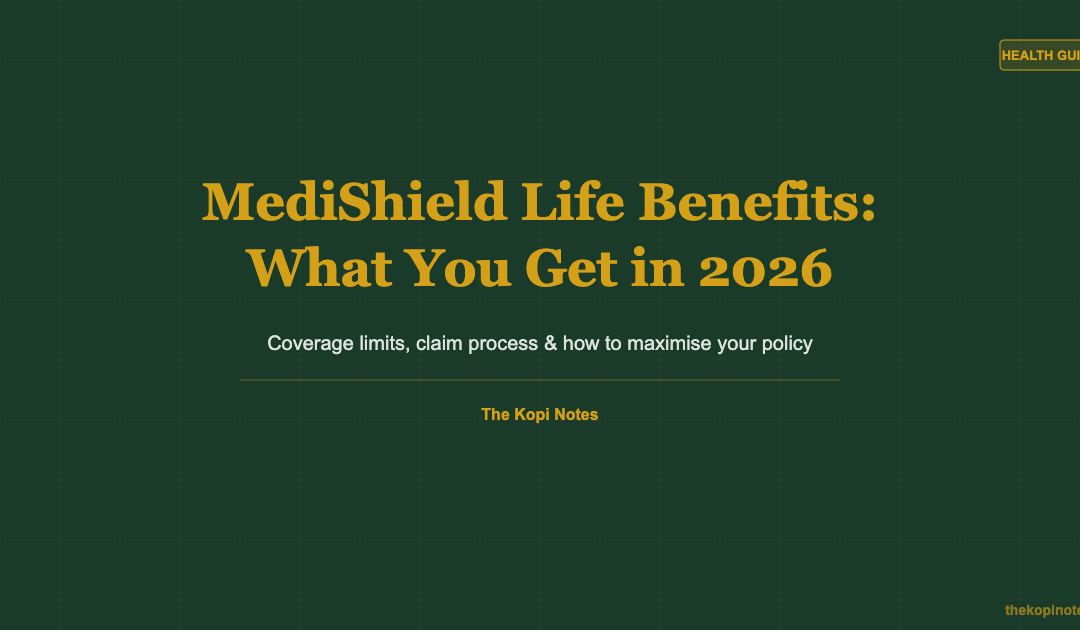

MediShield Life Benefits: What You Get in 2026

Singapore’s national health insurance scheme — and how it protects you

MediShield Life benefits cover every Singapore citizen and PR from birth. The scheme pays for large, unexpected hospital bills by reimbursing a portion of your inpatient and day-surgery costs at Class B2 and C wards. It covers ward charges, surgical fees, outpatient cancer drugs, and kidney dialysis — up to specific claim limits. On top of these limits, you share a small co-insurance portion (10%) and a deductible ($3,000/year for adults under 80). Most Singaporeans pair MediShield Life with an Integrated Shield Plan for fuller coverage.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

- MediShield Life automatically covers all Singapore citizens and PRs — premiums are deducted from Medisave.

- It pays for large hospital bills at B2/C ward rates — you still pay a deductible and 10% co-insurance.

- Upgrading to an Integrated Shield Plan (ISP) raises your coverage ceiling to private hospital rates.

Table of Contents

- What is MediShield Life?

- What MediShield Life Covers (Key Benefits)

- Coverage Limits and Claim Caps in 2026

- Deductible and Co-insurance Explained

- How Much Does MediShield Life Cost?

- MediShield Life vs Integrated Shield Plan

- How to Make a MediShield Life Claim

- How to Maximise Your MediShield Life Benefits

- Frequently Asked Questions

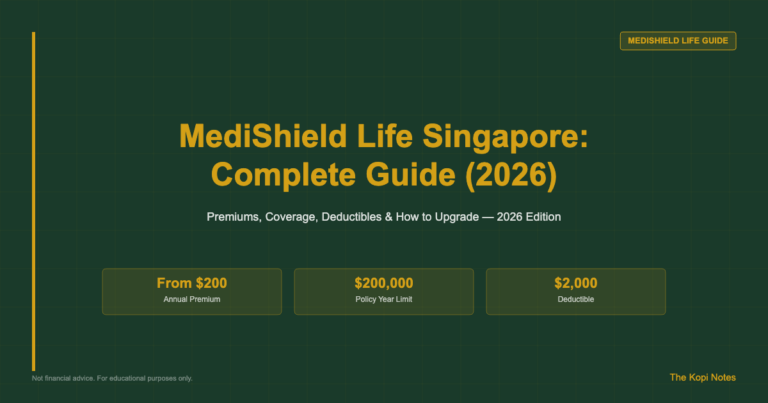

What is MediShield Life?

MediShield Life is Singapore’s mandatory national health insurance scheme. It was launched in November 2015, replacing the older MediShield plan. Every Singapore citizen and permanent resident is automatically enrolled from birth. You cannot opt out.

The scheme is run by the CPF Board and designed to help Singaporeans pay for large, unexpected hospital bills. Premiums are paid through your Medisave account — so in most cases, you do not need cash for your insurance premium.

MediShield Life covers inpatient hospitalisation (ward stays, surgeries) and selected outpatient treatments like cancer drug therapy and kidney dialysis. It is calibrated to Class B2 and C ward standards at public hospitals.

If you stay in a B2 or C ward at a public hospital, MediShield Life covers a substantial portion of your bill. For higher ward classes or private hospitals, you need an Integrated Shield Plan.

What MediShield Life Covers (Key Benefits)

MediShield Life covers a wide range of hospital and selected outpatient treatments. Here is what is included:

Inpatient Benefits

Daily ward and treatment charges: Covers your bed, meals, nursing care, and standard ward treatments. Claim limit up to $700 per day.

ICU charges: Covers up to $1,800 per day for intensive care admission, monitoring, and critical care equipment.

Surgical procedures: Covered based on a surgical table. Complex operations (Table 7A and above) can claim up to $4,000 or more per procedure.

Implants and consumables: Special implants used in surgery (cardiac stents, joint replacements) are claimable up to $7,500 per year.

Pregnancy complications: Serious complications during delivery are covered up to $900 per day.

Outpatient Benefits

Cancer drug therapy: Outpatient chemotherapy and targeted therapy at approved hospitals is covered up to $3,000 per month — crucial since cancer drugs can cost tens of thousands per cycle.

Kidney dialysis: Regular dialysis for end-stage kidney disease is covered up to $1,500 per month at approved centres.

Psychiatric treatment: Inpatient psychiatric treatment is claimable at up to $100 per day, for up to 60 days per year.

What is NOT Covered

- General outpatient GP or specialist visits for non-emergency conditions

- Dental treatment (unless due to an accident requiring hospitalisation)

- Cosmetic procedures and elective treatments not medically necessary

- Treatments overseas (except partial coverage for emergency hospitalisation abroad)

Coverage Limits and Claim Caps in 2026

MediShield Life pays up to specific claim limits per treatment type. After the limit is reached, you pay the remainder out of pocket — or via an ISP if you have one.

| Treatment / Benefit | Claim Limit | Co-insurance |

|---|---|---|

| Daily ward & treatment (B2/C) | Up to $700/day | 10% |

| ICU charges | Up to $1,800/day | 10% |

| Surgical procedures (Table 7A+) | Up to $4,000+ | 10% |

| Outpatient cancer drug therapy | Up to $3,000/month | 10% |

| Kidney dialysis | Up to $1,500/month | 10% |

| Implants & consumables | Up to $7,500/year | 10% |

| Psychiatric inpatient | Up to $100/day (60d/yr) | 10% |

Source: CPF Board, MediShield Life Scheme, June 2026

The overall annual claim limit is $150,000 per year — covering most realistic hospital scenarios.

Deductible and Co-insurance Explained

Even after MediShield Life pays its portion, you cover two cost-sharing components. Understanding these tells you exactly how much you pay out of pocket.

The Deductible

The deductible is the first chunk of your hospital bill that you pay before MediShield Life kicks in. Think of it like the excess on a car insurance policy.

- $3,000 per year for adults aged 80 and below

- $2,000 per year for adults aged 81 and above

Once you have paid $3,000 in deductible in a policy year, you do not pay it again for subsequent claims that year.

Co-insurance

Co-insurance is the percentage of the remaining claimable bill you pay after the deductible. For MediShield Life, the standard co-insurance rate is 10% for most claim types.

Example: if your claimable bill (after deductible) is $10,000, you pay $1,000 and MediShield Life pays $9,000.

Worked Example (SGD)

You are admitted to a Class B2 ward for 5 nights. Total subsidised bill: $8,000.

- Total bill: $8,000

- Less deductible (your share): $3,000

- Remaining claimable: $5,000

- MediShield Life pays 90%: $4,500

- Your co-insurance (10%): $500

- Total out-of-pocket: $3,500 (deductible + co-insurance)

Without MediShield Life, you would pay the full $8,000. The scheme protected $4,500 of your exposure. Adding an Integrated Shield Plan can reduce your out-of-pocket to as low as $550 for the same stay.

How Much Does MediShield Life Cost?

MediShield Life premiums are fully payable from your Medisave account. Premiums increase with age, reflecting higher hospitalisation risk. Here are the approximate annual premiums for 2026:

| Age Group | Annual Premium (SGD) | Monthly Equivalent |

|---|---|---|

| 1–20 | $100–$150 | ~$8–13 |

| 21–30 | $175–$225 | ~$15–19 |

| 31–40 | $250–$320 | ~$21–27 |

| 41–50 | $400–$530 | ~$33–44 |

| 51–60 | $735–$965 | ~$61–80 |

| 61–70 | $1,200–$1,600 | ~$100–133 |

| 71–80 | $2,000–$2,600 | ~$167–217 |

Source: CPF Board, MediShield Life premium table 2026. Exact premiums vary by age band within each group.

Premium subsidies are available for lower-income households via Additional Premium Support (APS) — applied automatically, no separate application needed. If you have an ISP, your ISP premium is paid on top of and separately from your MediShield Life premium — both are Medisave-payable up to MOH withdrawal limits.

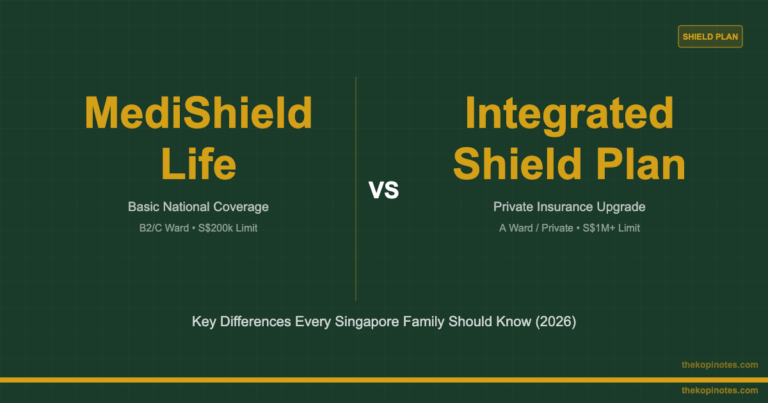

MediShield Life vs Integrated Shield Plan

MediShield Life is the base layer of Singapore’s healthcare financing. An Integrated Shield Plan (ISP) is an optional private insurance product that sits on top — extending coverage to higher ward classes and private hospitals.

| Feature | MediShield Life | Integrated Shield Plan |

|---|---|---|

| Coverage | B2/C ward (public hospital) | Up to private hospital |

| Provider | Government (CPF Board) | Private insurers (AIA, Prudential, Great Eastern, etc.) |

| Annual claim limit | $150,000/year | Unlimited or very high |

| Deductible | $3,000/year | Varies ($0–$3,500) |

| Co-insurance | 10% | 5–10% (reduced with rider) |

| Medisave payable? | Yes (fully) | Yes (up to withdrawal limit) |

Source: MOH, CPF Board, individual ISP provider brochures, 2026

For most Singaporeans, an ISP is worth the extra premium. The five main ISP providers are AIA, Prudential, Great Eastern, Income (NTUC), and Singlife. Compare them in our Integrated Shield Plan comparison guide.

For planning your long-term healthcare budget, use the Singapore retirement calculator to model healthcare costs alongside your CPF savings.

How to Make a MediShield Life Claim

In most cases, you do not have to do anything. MediShield Life claims are processed automatically by the hospital.

For Inpatient Claims

- Get admitted to a Singapore hospital with your NRIC/FIN.

- The hospital submits your claim directly to CPF Board upon discharge — no paperwork from you.

- You receive a discharge bill showing total charges, MediShield Life payment, and your remaining share.

- Pay your balance using Medisave or cash. Government subsidies are applied first.

For Outpatient Claims (Cancer / Dialysis)

- Ensure your treatment centre is approved by CPF Board.

- The centre submits claims on your behalf each cycle.

- You pay your co-insurance share only after the deductible is met.

View all your MediShield Life claims and coverage status via the CPF digital portal or the CPF app. Disputes must be raised within 1 year of the bill date.

How to Maximise Your MediShield Life Benefits

1. Stay in the Right Ward Class

MediShield Life is calibrated to B2/C ward rates. Upgrading to B1 or A ward does not increase your claimable amount — you pay the difference out of pocket. Staying in B2 means MediShield Life covers a much higher proportion of your bill.

2. Use Approved Outpatient Centres

For cancer drug therapy and dialysis, confirm your centre is on the CPF Board’s approved list. Non-approved private clinics are not eligible for outpatient MediShield Life coverage.

3. Top Up with an Integrated Shield Plan

An ISP is the single most effective way to reduce out-of-pocket exposure. Our best Integrated Shield Plan guide shows how a good ISP can cut your out-of-pocket to below $1,000 for most hospital stays. Platforms like Endowus (referral code: 2V343) and Syfe (code: SRPRFFFCD) can help you grow the savings that fund your Medisave top-ups.

4. Keep Your Medisave Topped Up

MediShield Life premiums are deducted from Medisave. If your Medisave runs low, you pay in cash. Keep Medisave funded — especially as you approach your 50s and 60s when premiums rise sharply. Voluntary Medisave top-ups give you an income tax deduction too.

5. Review Coverage Limits Annually

MOH periodically updates MediShield Life coverage limits. Cancer drug and surgical procedure caps have been expanded multiple times. Stay updated. For retirement planning, use the Singapore retirement calculator to model your healthcare costs over time.

Frequently Asked Questions

Does MediShield Life cover pre-existing conditions?

What is the annual claim limit for MediShield Life?

Can I use Medisave to pay my deductible and co-insurance?

Is MediShield Life the same as an Integrated Shield Plan?

Does MediShield Life cover overseas hospitalisation?

What happens if I upgrade to a higher ward class?

The Bottom Line

MediShield Life is a genuinely useful foundation for every Singaporean’s healthcare financing. It automatically covers large inpatient bills, requires no cash premiums if your Medisave is funded, and cannot exclude you based on pre-existing conditions.

However, the $3,000 annual deductible and per-treatment claim caps can leave a meaningful gap for complex conditions. The right move for most Singaporeans is to pair MediShield Life with a suitable Integrated Shield Plan.

Check our Integrated Shield Plan comparison to find the plan that best matches your budget and ward preference. For broader financial planning, the Singapore retirement calculator helps you model healthcare costs alongside CPF savings and investment income.

The Kopi Notes may receive a referral fee if you sign up via the links above. This does not affect our editorial independence. All content is for educational purposes only and is not financial advice.

Get Free Insurance Advice

Speak with a licensed insurance advisor. No obligation, no cost.

By submitting this form, you agree to our Privacy Policy.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.