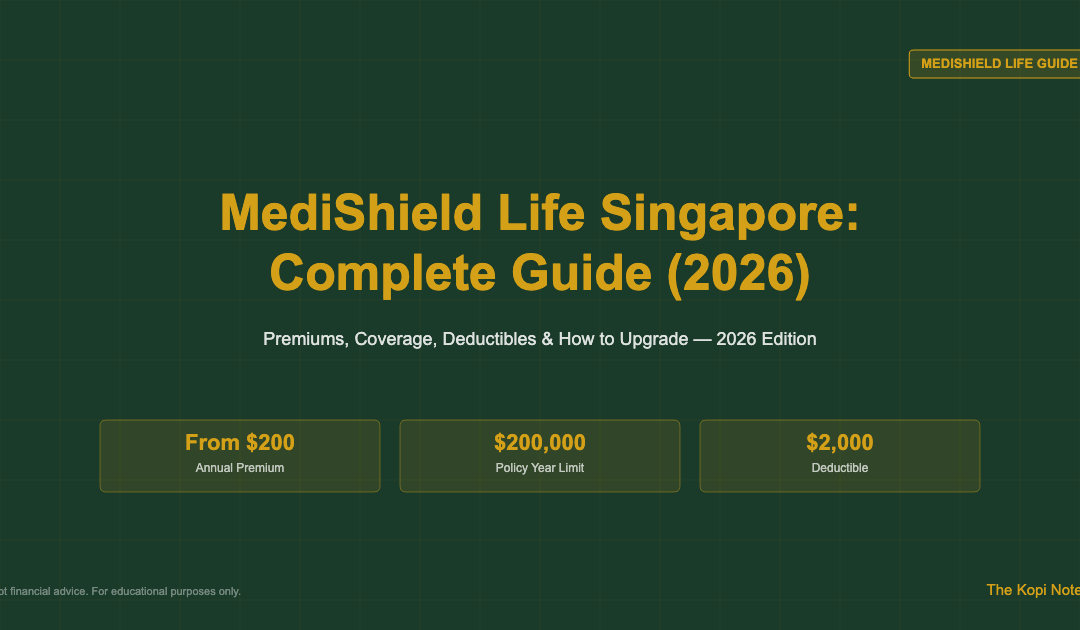

MediShield Life Singapore: Complete Guide (2026)

MediShield Life is Singapore’s mandatory national health insurance scheme, covering all Singapore Citizens and Permanent Residents from birth for life. It pays out for large hospital bills in Class B2/C wards at public hospitals and selected outpatient treatments, with a $200,000 annual claim limit and premiums fully payable via MediSave. For Singaporeans who want access to higher ward classes or private hospitals, an Integrated Shield Plan (ISP) can be added on top.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

📋 In This Guide

- What Is MediShield Life?

- What MediShield Life Covers

- Premiums: How Much Does It Cost?

- Deductible and Co-Insurance Explained

- Subsidies and Support for Lower-Income Singaporeans

- MediShield Life vs Integrated Shield Plan

- Should You Upgrade to an ISP?

- How to Make a MediShield Life Claim

- Frequently Asked Questions

What Is MediShield Life?

MediShield Life is Singapore’s national health insurance scheme, administered by the CPF Board under the Ministry of Health. It replaced the older MediShield scheme in November 2015 with two critical upgrades: universal coverage (no one can opt out or be excluded) and lifelong protection (it never lapses as long as premiums are paid).

Every Singapore Citizen and Permanent Resident is automatically enrolled. Premiums are deducted from your MediSave account annually — you do not need to pay cash unless your MediSave balance is insufficient. MediShield Life sits at the foundation of Singapore’s three-tier healthcare financing framework:

- Tier 1 — MediShield Life: Covers subsidised hospitalisation and outpatient treatments at public hospitals (Class B2/C wards)

- Tier 2 — Integrated Shield Plans (ISPs): Private insurer top-ups covering higher wards (A, B1) or private hospitals

- Tier 3 — ISP Riders: Additional coverage for deductibles and co-insurance under your ISP (subject to new MOH rules from April 2026)

Understanding MediShield Life is the starting point for any Singaporean planning their healthcare finances. It determines your baseline protection and informs whether an Integrated Shield Plan comparison makes sense for your situation.

What MediShield Life Covers

MediShield Life is designed to cover large, catastrophic medical bills — not routine GP visits or small claims. Coverage applies to:

- Inpatient hospitalisation at Class B2/C wards in public hospitals

- Inpatient stays at Class A/B1 wards or private hospitals (pro-rated to B2/C equivalent rates)

- Day surgery at public hospitals

- Selected outpatient treatments: chemotherapy, radiotherapy, dialysis, and certain immunotherapy treatments

- Cell, Tissue, and Gene Therapy Products (CTGTPs) on the MOH list (introduced October 2025)

Updated Claim Limits (Effective April 2025)

Following the 2024 MediShield Life Council review, claim limits were enhanced significantly:

| Treatment / Benefit | Old Limit | New Limit (Apr 2025) |

|---|---|---|

| Normal ward (Day 1–2) | $1,000/day | $1,630/day |

| ICU ward | $2,200/day | $5,140/day |

| Annual policy year claim limit | $150,000 | $200,000 |

| Lifetime claim limit | None | None (unlimited) |

Source: Ministry of Health Singapore, MediShield Life enhancements, April 2025.

What MediShield Life Does Not Cover

Key exclusions include: cosmetic procedures, dental treatments (except hospitalised dental surgery), treatment of self-inflicted injuries, outpatient GP visits and routine health screening, and congenital conditions in most circumstances. For gaps like these, building a CPF investment strategy that includes cash reserves alongside insurance coverage is wise.

Premiums: How Much Does MediShield Life Cost?

MediShield Life premiums are age-banded — they increase as you get older, reflecting higher healthcare utilisation in later life. Premiums are set annually based on your Age Next Birthday (ANB) on the policy start/renewal date. All figures below are inclusive of 9% GST and apply for policy start/renewal dates on or after 1 April 2025.

| Age Next Birthday | Annual Premium (incl. 9% GST) |

|---|---|

| 1–20 | $200 |

| 21–30 | $295 |

| 31–40 | $503 |

| 41–50 | $637 |

| 51–60 | $903 |

| 61–65 | $1,131 |

| 66–70 | $1,326 |

| 71–73 | $1,643 |

| 74–75 | $1,816 |

| 76–78 | $2,027 |

| 79–80 | $2,187 |

| 81–83 | $2,303 |

| 84–85 | $2,616 |

| 86–90 | $2,785 |

| Above 90 | $2,826 |

Source: CPF Board MediShield Life Premium Schedule, applicable w.e.f. 1 April 2025. Includes 9% GST.

Premium Phase-in (2025–2028)

Following the 2024 Council review, premiums are being phased in gradually over three years (April 2025 to March 2028), with total premium increases capped at 35%. Crucially, MOH has committed that additional MediSave top-ups and premium subsidies will more than offset the increases for over 90% of Singaporeans. A Singaporean aged 40 in 2026, for example, pays approximately $503/year — fully deductible from MediSave, meaning zero cash outlay.

For Singaporeans tracking long-term healthcare costs alongside retirement planning, the Singapore retirement calculator can help model how rising premiums fit into your financial picture.

Deductible and Co-Insurance Explained

MediShield Life is not a first-dollar coverage scheme. It uses a deductible + co-insurance structure to discourage over-consumption and keep the scheme financially sustainable.

Inpatient Deductible

The deductible is the portion of your hospital bill you must pay before MediShield Life kicks in. For inpatient stays, the deductible is currently $2,000 per policy year for Class B2/C wards. The deductible is payable only once per policy year — subsequent hospitalisations within the same year do not require a fresh deductible. From 1 April 2027, the inpatient deductible will increase as part of the second phase of enhancements.

Outpatient Deductible (New from 1 June 2026)

A new $500 outpatient deductible per policy year was introduced on 1 June 2026. This applies to subsidised outpatient treatments (e.g. chemotherapy, dialysis) covered under MediShield Life.

Co-Insurance

After the deductible is met, MediShield Life covers a portion of your claimable bill, while you bear a co-insurance percentage. The co-insurance rate is tiered and decreasing:

- First $5,000 of claimable amount: 10% co-insurance

- Next $5,000: 5% co-insurance

- Above $10,000: 3% co-insurance

Worked example: A Singaporean in a Class B2 ward incurs a $15,000 subsidised bill. After the $2,000 deductible, the claimable amount is $13,000. MediShield Life covers: 90% × $5,000 + 95% × $5,000 + 97% × $3,000 = $4,500 + $4,750 + $2,910 = $12,160. The patient pays $840 in co-insurance out-of-pocket (or via MediSave).

These out-of-pocket amounts can be managed using your MediSave balance. If you’re building a CPF investment strategy, factor in adequate MediSave reserves for healthcare co-payments.

Subsidies and Support for Lower-Income Singaporeans

MediShield Life includes a robust subsidy framework so that no Singaporean is priced out of coverage. There are four main support tiers:

1. Premium Subsidies

Available to lower- and middle-income Singaporeans who meet both conditions: household monthly income per person ≤ $3,600, and Annual Value of residence ≤ $31,000. Eligible households can receive up to 60% subsidy on MediShield Life premiums.

2. Pioneer Generation (PG) Package

Singaporeans who were citizens before 1987 and born before 1950 receive PG subsidies of 40–60% on MediShield Life premiums, plus annual MediSave top-ups of $250–$900 depending on age — effectively making MediShield Life free for most Pioneers.

3. Merdeka Generation (MG) Package

Singaporeans born 1950–1959 and who were citizens before 1996 receive MG subsidies plus MediSave top-ups of $200/year for life, along with subsidies for ISP premiums.

4. Additional Premium Support (APS)

For Singaporeans who remain unable to afford premiums even after subsidies and lack family support, the Government has expanded APS eligibility. No one will be denied MediShield Life coverage due to inability to pay. Pairing strong insurance coverage with passive income strategies can further build the buffer for co-payments and deductibles.

MediShield Life vs Integrated Shield Plan: What’s the Difference?

MediShield Life covers subsidised treatments in Class B2/C public hospital wards. If you want access to Class A or B1 wards, or private hospitals, you need an Integrated Shield Plan (ISP) — a private health insurance policy that integrates with MediShield Life for seamless billing.

ISP Insurers in Singapore (2026)

Five insurers currently offer ISPs in Singapore: AIA (HealthShield Gold Max A/B/C), Great Eastern (Supreme Health P Plus/P/B Plus/A Plus), Income (NTUC) (Enhanced IncomeShield), Prudential (PRUShield Premier/Plus/Standard), and Singlife (Shield Plans 1–4).

New ISP Rider Rules from April 2026

From 1 April 2026, MOH introduced new requirements: all newly purchased ISP riders can no longer fully cover the mandatory inpatient deductible — policyholders must pay a minimum amount out of pocket before insurance kicks in. Existing riders purchased before April 2026 are grandfathered under transition arrangements.

For a detailed side-by-side comparison of all ISP plans, see the Integrated Shield Plan comparison guide on The Kopi Notes.

Should You Upgrade to an Integrated Shield Plan?

MediShield Life alone provides robust protection for subsidised care. Whether you should add an ISP depends on your circumstances:

Reasons to Stay with MediShield Life Only

- You are comfortable with Class B2/C public hospital wards (clinically equivalent care)

- You have limited cash flow and prefer to maximise investments

- You are eligible for Pioneer or Merdeka Generation subsidies

- You have substantial MediSave savings to cover deductibles and co-payments

Reasons to Upgrade to an ISP

- You want choice of specialist or hospital without ward restrictions

- You want to access Class A wards or private hospitals for non-emergency care

- You have dependents and want maximum peace of mind

- You are in a peak earning phase where healthcare disruption would be costly

A practical approach: keep MediShield Life as the foundation, add a mid-tier ISP (e.g. Class A ward plan), and ensure you have enough liquid savings or CPF OA for deductibles. Consider building S-REIT investments that generate dividends to cover healthcare co-payments in retirement. Those using Endowus or Syfe to invest surplus CPF can use the Endowus referral code (2V343) or Syfe referral code (SRPRFFFCD) to get started with bonuses.

How to Make a MediShield Life Claim

For most hospitalisations at public hospitals, you don’t need to do anything — the hospital automatically submits the MediShield Life claim on your behalf at discharge. The process:

- Hospitalisation occurs at a public hospital in a subsidised ward (B2/C)

- Hospital submits claim automatically via the billing system

- MediShield Life pays the hospital directly — eligible claim amount settled against your bill

- You pay the remainder — deductible + co-insurance, via MediSave or cash

- Claim notification sent via CPF online portal or mail

For outpatient treatments (chemotherapy, dialysis, etc.), the same auto-submission process applies at approved public institutions. Private hospitals and clinics not integrated with MOH billing may require manual submission — check with your provider.

Track all MediShield Life claims via the CPF website under “My MediShield Life”. You can also authorise a family member to manage claims on your behalf.

Tip: Always check your MediShield Life claim statement against the final hospital bill. If charges appear under the wrong treatment category, request a detailed bill breakdown from the hospital’s finance department.

This article is for educational purposes only and does not constitute financial or insurance advice. MediShield Life rules and premiums are subject to change by the CPF Board and Ministry of Health. Always verify current figures at cpf.gov.sg or moh.gov.sg. Consult a licensed financial adviser for personalised advice.

Frequently Asked Questions About MediShield Life

What is MediShield Life and is it compulsory?

MediShield Life is Singapore’s mandatory national health insurance scheme administered by the CPF Board. It is compulsory for all Singapore Citizens and Permanent Residents — you cannot opt out. It provides lifelong coverage for large hospital bills at Class B2/C wards in public hospitals, with premiums payable via your MediSave account.

How much does MediShield Life cost per year?

MediShield Life premiums are age-banded and include 9% GST. For 2025/2026: ages 1–20 pay $200/year; ages 31–40 pay $503/year; ages 51–60 pay $903/year; ages 66–70 pay $1,326/year; above 90 pay $2,826/year. All premiums are fully payable via MediSave — zero cash required for most Singaporeans. Lower-income households may receive subsidies of up to 60%.

Does MediShield Life cover private hospitals?

MediShield Life benefits are computed based on Class B2/C ward rates at public hospitals. If you stay in a private hospital or higher-class ward, your bill is pro-rated to B2/C equivalent rates before the MediShield Life claim is calculated — meaning significant out-of-pocket costs. To cover private hospital stays, you need an Integrated Shield Plan (ISP).

What is the difference between MediShield Life and an Integrated Shield Plan?

MediShield Life is the compulsory base layer covering Class B2/C ward subsidised bills at public hospitals. An Integrated Shield Plan (ISP) is an optional private health insurance policy that sits on top of MediShield Life, extending coverage to Class A/B1 wards or private hospitals. ISPs are offered by five private insurers: AIA, Great Eastern, Income (NTUC), Prudential, and Singlife.

What is the MediShield Life deductible in 2026?

For inpatient hospitalisation, the MediShield Life deductible is $2,000 per policy year (payable once per year). A new outpatient deductible of $500 per policy year was introduced from 1 June 2026 for subsidised outpatient treatments like chemotherapy and dialysis. Both deductibles can be paid using your MediSave balance.

Will MediShield Life cover pre-existing conditions?

Yes — MediShield Life covers pre-existing conditions. You cannot be excluded or have premiums loaded due to a pre-existing condition. This universal coverage was a key enhancement over the old MediShield scheme, ensuring all Singaporeans have baseline protection regardless of their medical history.

Can Permanent Residents use MediShield Life?

Yes. MediShield Life covers both Singapore Citizens and Permanent Residents. However, PR claims are pro-rated differently from citizens, and PRs are generally not eligible for Pioneer or Merdeka Generation subsidies unless they hold citizenship.

Get Free Insurance Advice

Speak with a licensed insurance advisor. No obligation, no cost.

By submitting this form, you agree to our Privacy Policy.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.