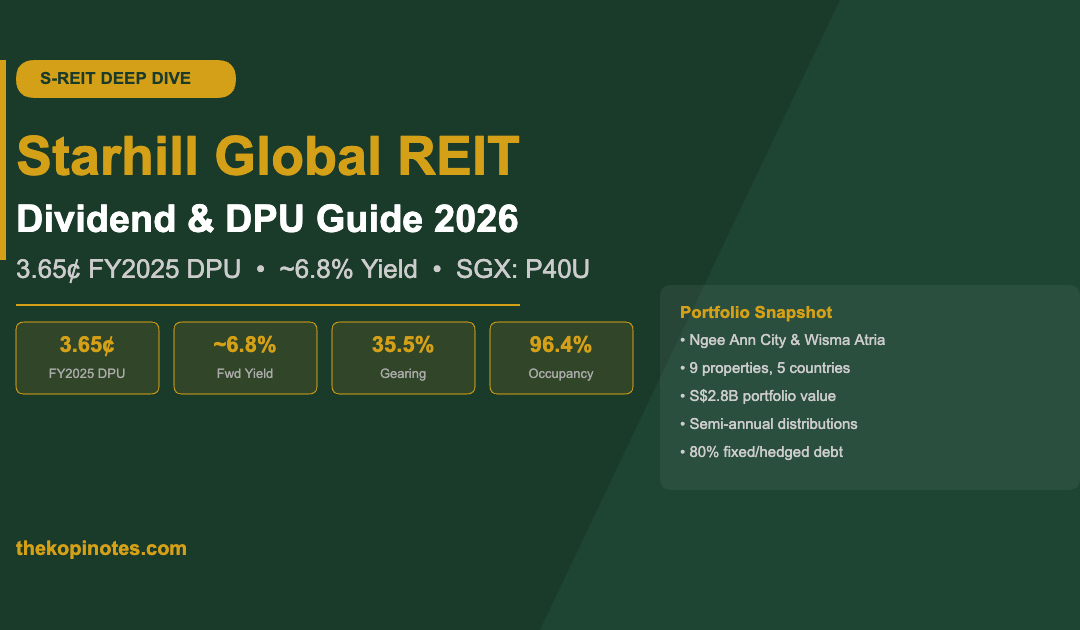

If you hold units in Starhill Global REIT (SGX: P40U) — or you’re researching it as an income investment — one question comes up every time: how reliable is the dividend, and what does the DPU trajectory look like?

This guide answers exactly that. We break down Starhill Global REIT’s full dividend history, explain the FY2025 DPU of 3.65 cents, analyse the ~6.8% forward yield, and assess whether the distribution is sustainable heading into 2026 and beyond.

Quick take: Starhill Global REIT offers one of the highest yields on the Singapore Exchange among retail REITs, backed by two prime Orchard Road assets and a well-hedged balance sheet. The FY2025 DPU recovery to 3.65¢ — up from 3.63¢ in FY2024 — signals stabilisation after years of rebuilding post-Covid. The 3QFY26 DPU of 2.05¢ (+2.5% year-on-year) points to continued modest growth.

Starhill Global REIT Overview

Starhill Global REIT is a Singapore-listed real estate investment trust that invests primarily in retail and office properties across Asia Pacific. Listed on the SGX since 2005 under ticker P40U (now also displayed as STHL), it is sponsored by YTL Corporation, a Malaysian conglomerate.

The REIT’s portfolio spans 9 properties across 5 countries — Singapore, Australia, Malaysia, Japan and China — with a combined valuation of approximately S$2.8 billion. However, its two Singapore flagship assets dominate performance: Ngee Ann City (a stake in the 190-metre Orchard Road landmark) and Wisma Atria (a prime retail and office building directly above Orchard MRT station) together contribute 63.4% of net property income.

Starhill distributes income semi-annually, with distributions typically paid in March and September each year. The fiscal year ends 30 June.

| Metric | Value (as at May 2026) |

|---|---|

| SGX Ticker | P40U / STHL |

| Sponsor | YTL Corporation Berhad |

| Portfolio Size | 9 properties, 5 countries |

| Portfolio Value | ~S$2.8 billion |

| FY2025 DPU | 3.65 cents (+0.6% YoY) |

| Forward Yield (at S$0.535) | ~6.8% |

| Gearing Ratio | 35.5% (3QFY26) |

| Portfolio Occupancy | 96.4% (3QFY26) |

| Distribution Frequency | Semi-annual |

| Analyst Consensus | BUY, TP S$0.65–S$0.68 |

Starhill Global REIT DPU History: FY2019–FY2025

Understanding Starhill’s dividend history reveals a REIT that suffered a sharp Covid-era cut in FY2020, then rebuilt distributions gradually over five years back to near pre-pandemic levels — without the benefit of a major acquisition or rights issue to juice income.

| Fiscal Year | DPU (cents) | YoY Change | Key Driver |

|---|---|---|---|

| FY2019 | 4.48¢ | — | Stable pre-Covid baseline |

| FY2020 | 2.96¢ | –33.9% | Covid-19 rent rebates, retail closures |

| FY2021 | 3.35¢ | +13.2% | Partial reopening, rental recovery |

| FY2022 | 3.80¢ | +13.4% | Full reopening, Orchard Road footfall recovery |

| FY2023 | 3.80¢ | 0.0% | Stable; Adelaide vacancy headwind |

| FY2024 | 3.63¢ | –4.5% | Adelaide Myer Centre anchor vacancy |

| FY2025 | 3.65¢ | +0.6% | Singapore recovery; FX tailwind |

Key takeaway: The FY2020 cut to 2.96¢ was the worst in the REIT’s history, driven by mandatory rental waivers during circuit breaker restrictions. The recovery since then has been methodical — FY2022 and FY2023 saw the DPU stabilise at 3.80¢, before the Adelaide vacancy weighed on FY2024. FY2025’s marginal uptick to 3.65¢ signals the floor may be in.

FY2025 Full-Year Results (Ended 30 June 2025)

Starhill Global REIT delivered a FY2025 DPU of 3.65 cents, up 0.6% year-on-year, marking a return to growth after FY2024’s dip.

The second half saw 2HFY2025 DPU of 1.85¢, unchanged year-on-year but supported by improving Singapore contributions. Full-year gross revenue rose 0.7% to S$95.8 million for the 2H period, driven by stronger performance from retail properties in Singapore and favourable net foreign currency movements.

Portfolio occupancy at 30 June 2025 stood at 94.6% (vs 97.7% at 30 June 2024), with the decline attributable to lower office occupancy at Myer Centre Adelaide following the termination of a single large tenant’s lease. The Singapore and Malaysia properties remained near full occupancy.

Gearing was 36.0% as at 30 June 2025 — well within MAS’s 50% regulatory limit — with a weighted average cost of debt that remained manageable thanks to proactive hedging.

3Q FY2025/26 Update (April 2026)

Starhill’s most recent quarterly results — for 3Q FY2025/26 ended March 2026 — showed continued stability with a hint of improvement:

| Metric | 3QFY25/26 | YoY Change |

|---|---|---|

| Gross Revenue | S$47.9M | +0.7% |

| Net Property Income | S$37.9M | 0.0% |

| DPU (quarterly) | 2.05¢ | +2.5% |

| Portfolio Occupancy | 96.4% | +1.8ppt |

| Retail Occupancy | 97.3% | Stable |

| Gearing | 35.5% | –0.5ppt |

| Fixed/Hedged Debt | 80% | Maintained |

The 2.5% DPU growth in 3QFY26 is encouraging. Strong contributions from Malaysia, Japan and China (all at 100% occupancy) helped offset lingering Adelaide softness. The Wisma Atria façade upgrade (S$2.2M, due mid-2026) is expected to enhance retail frontage appeal and support rental reversions.

Yield Analysis & Peer Comparison

At the current unit price of approximately S$0.535, Starhill Global REIT’s FY2025 DPU of 3.65¢ translates to a forward yield of ~6.8% — well above the CPF OA rate of 2.5% and Singapore Savings Bond yields of ~2.8–3.0%.

Importantly, as a Singapore REIT, distributions to individual Singapore tax residents are tax-exempt at the investor level — so that 6.8% is what you actually receive in your account, with no withholding tax applied.

| REIT | Ticker | Approx. Yield | Gearing | Sector |

|---|---|---|---|---|

| Starhill Global REIT | P40U | ~6.8% | 35.5% | Retail/Office |

| Sasseur REIT | CRPU | ~9.5% | 24.5% | Retail (China) |

| Sabana REIT | M1GU | ~7.5% | 37.0% | Industrial |

| AIMS APAC REIT | O5RU | ~6.9% | 26.8% | Industrial |

| Suntec REIT | T82U | ~6.0% | 42.5% | Retail/Office |

| Keppel REIT | K71U | ~5.4% | 40.2% | Office |

| ParkwayLife REIT | C2PU | ~4.0% | 33.4% | Healthcare |

Starhill sits in a competitive sweet spot: its yield of ~6.8% is among the highest for a Singapore-focused retail REIT, with a gearing ratio (35.5%) that is meaningfully lower than Suntec (42.5%) or Keppel (40.2%). This gives Starhill more financial flexibility and less refinancing risk.

Portfolio: Ngee Ann City & Wisma Atria

Starhill’s income engine is its two Singapore properties, which together generate nearly two-thirds of the REIT’s net property income.

Ngee Ann City is one of Singapore’s most iconic retail landmarks on Orchard Road, home to Takashimaya department store and luxury brands. Starhill holds a 27.23% interest in the strata lots. The property benefits from long anchor leases and a direct pedestrian connection to the Orchard Road shopping belt.

Wisma Atria is a seven-storey retail mall and 14-storey office tower directly above Orchard MRT station. Starhill owns 100% of the strata lots. The S$2.2 million façade upgrade scheduled for completion by mid-2026 is designed to improve street-level visibility and attract premium F&B and fashion tenants. The Australian assets (Myer Centre Adelaide) have been a drag on earnings since FY2024 but are expected to stabilise after the ongoing A$6 million food court refurbishment completes by end-2026.

| Property | Country | Type | Occupancy | NPI Contribution |

|---|---|---|---|---|

| Ngee Ann City (27.23%) | Singapore | Retail | ~100% | ~37% of portfolio NPI |

| Wisma Atria | Singapore | Retail/Office | 97.3% retail | ~26% of portfolio NPI |

| Myer Centre Adelaide | Australia | Retail/Office | Recovering | ~15% of portfolio NPI |

| Lot 10 (Malaysia) | Malaysia | Retail | 100% | ~10% of portfolio NPI |

| Japan & China properties | Japan/China | Retail/Office | 100% | ~12% of portfolio NPI |

DPU Sustainability Assessment

The key question for income investors: can Starhill maintain or grow its DPU from 3.65¢?

Factors supporting DPU stability:

- Low gearing (35.5%): Below the 45% threshold that typically triggers concern. 80% of debt is fixed or hedged, providing earnings visibility even if SORA rises.

- Long master leases: Ngee Ann City benefits from master lease structures with anchor tenants, providing predictable base income regardless of sub-tenant performance.

- Wisma Atria AEI: The façade upgrade is a relatively modest capital commitment (S$2.2M) that should drive rental uplift upon completion in mid-2026.

- Singapore retail strength: Orchard Road tourist arrivals and domestic spending have recovered well post-Covid, supporting rental reversions.

- 3.5-year average debt maturity: No near-term cliff-edge refinancing risk.

Risks to watch:

- Adelaide vacancy: Myer Centre Adelaide’s office component remains a drag. Full stabilisation depends on securing a new anchor tenant.

- FX headwinds: Australian dollar and Malaysian ringgit weakness relative to the Singapore dollar can reduce repatriated income.

- Interest rate sensitivity: 20% of debt is floating-rate. A sustained rise in SORA would compress distributable income.

- Retail sector disruption: E-commerce remains a structural headwind for physical retail, particularly in mid-tier segments.

On balance, the DPU looks sustainable at the 3.60–3.70¢ range for FY2026, with upside potential if the Adelaide refurbishment lands well and Wisma Atria’s AEI drives positive rental reversions.

For a broader view of how S-REITs stack up on gearing and yield, see our S-REIT Outlook 2026 guide. You can also model income scenarios using our free REITs Dividend Yield Calculator and S-REIT Yield vs SGS Bond Spread Calculator.

How to Buy Starhill Global REIT (CPF/SRS)

Starhill Global REIT (P40U) is listed on the Singapore Exchange (SGX) and can be purchased through any Singapore brokerage. Here’s how to invest:

Using Cash: Purchase via platforms like FSMOne (referral code P0544985) for one of Singapore’s lowest brokerage fees — 0.08%, minimum S$10. Shares are held in your CDP account, entitling you to direct dividend payments.

Using CPF Investment Scheme (CPFIS-OA): Starhill Global REIT is CPF-approved, meaning you can invest your CPF Ordinary Account savings above the first S$20,000 via CPFIS. The 2.5% OA interest you forgo is the opportunity cost — but at ~6.8% yield, the spread is compelling. Use our CPFIS Calculator to model the trade-off.

Using SRS: You can also invest via your Supplementary Retirement Scheme (SRS) account for tax relief on contributions, with dividends accumulating tax-free until withdrawal.

Via Robo-Advisors: Syfe REIT+ (use code TKNSG) provides diversified S-REIT exposure including Starhill, while Endowus offers REIT-focused funds accessible with CPF and SRS savings.

Investor Verdict

Starhill Global REIT is a HOLD to BUY for income-focused investors who want Orchard Road retail exposure with a defensive balance sheet.

The FY2025 DPU of 3.65¢ and 3QFY26’s 2.5% growth rate suggest the worst of the Covid and Adelaide drag is behind it. The ~6.8% yield at S$0.535 is attractive relative to fixed deposits and Singapore Savings Bonds, particularly given the tax-exempt nature of REIT distributions.

Analyst consensus sits at BUY with a target price of S$0.65–S$0.68, implying 21–27% total return potential including distributions. The key re-rating catalyst is the completion of both AEI projects and a sustained recovery in Adelaide occupancy.

For yield-hunters, Starhill represents a lower-risk, lower-gearing option compared to Suntec or Keppel, with prime Singapore real estate anchoring its income stream. Compare it against other high-yielding plays in our Best S-REITs 2026 guide.

Frequently Asked Questions

What is Starhill Global REIT's current dividend yield?

When does Starhill Global REIT pay dividends?

Has Starhill Global REIT ever cut its dividend?

Is Starhill Global REIT a good investment in 2026?

Can I buy Starhill Global REIT using CPF?

What is the gearing ratio of Starhill Global REIT?

What properties does Starhill Global REIT own?

How does Starhill Global REIT's yield compare to CPF and fixed deposits?

What is Starhill Global REIT's outlook for FY2026?

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.