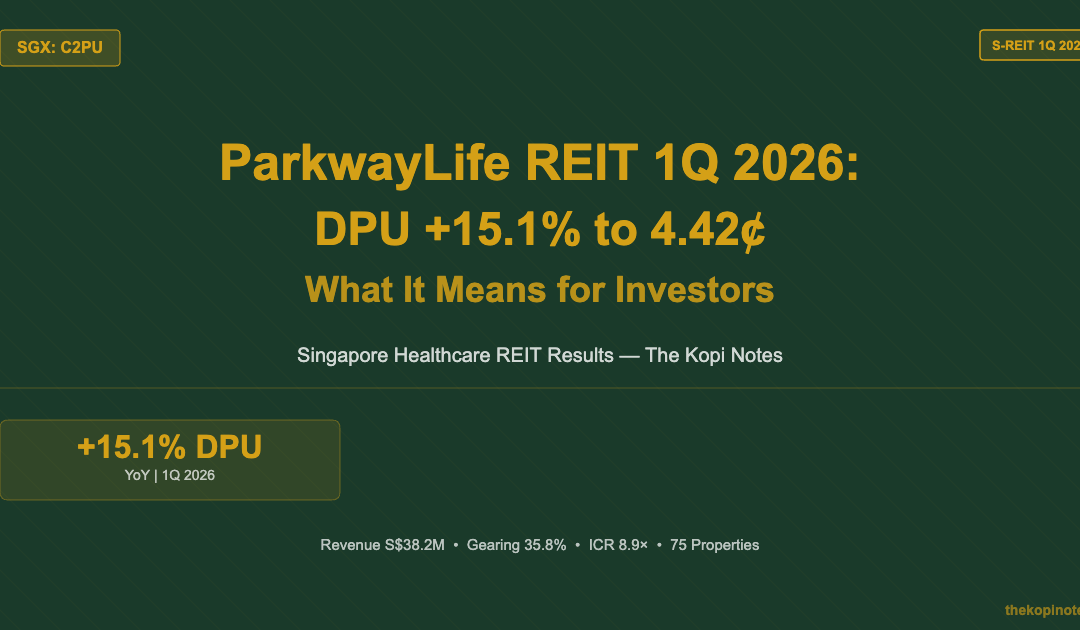

ParkwayLife REIT 1Q 2026 Results (SGX: C2PU): DPU +15.1% to 4.42¢ & What It Means for Investors

S-REIT Analysis · June 2026 · 8 min read

ParkwayLife REIT (SGX: C2PU) delivered a strong 1Q 2026, with Distribution Per Unit (DPU) rising 15.1% year-on-year to 4.42 Singapore cents. Revenue dipped slightly to S$38.2 million, but the DPU jump was driven by the end of a 3-year rent rebate and a new annual rent review formula for its Singapore hospitals. With 75 properties across Singapore, Japan, and France, a conservative gearing of 35.8%, and analyst consensus at BUY with a S$4.75 target, ParkwayLife remains one of the most defensive healthcare REITs on the SGX.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

- DPU jumped 15.1% YoY to 4.42¢ — driven by the cessation of rent rebates and a new rent review formula for its Singapore hospital leases

- Japan vacancy risk from Miyako Group liquidation affects ~1.6% of FY2026 gross revenue — manageable, with 4–8 months of security deposits retained

- Balance sheet is rock-solid: gearing at 35.8%, ICR at 8.9×, no refinancing needed until March 2027

Table of Contents

Jump to Section

- 1Q 2026 Results at a Glance

- Singapore Portfolio: The DPU Driver

- Japan Portfolio & Miyako Group Impact

- DPU History: 6 Years of Growth

- Debt Management & Balance Sheet

- Peer Comparison: Yield vs Gearing

- 1Q 2026 Financials Summary

- What This Means for Investors

- How to Buy ParkwayLife REIT in Singapore

- Frequently Asked Questions

1Q 2026 Results at a Glance

ParkwayLife REIT announced its first quarter 2026 results on 7 May 2026. The headline number that matters most to you as an income investor is the Distribution Per Unit — and it came in strong.

Here is what drove the numbers:

- Revenue: S$38.2 million (-2.1% YoY) — a slight dip, mainly from lower Japan contributions

- Net Property Income (NPI): S$35.8 million (-2.7% YoY)

- DPU: 4.42¢ (+15.1% YoY) — the big winner of the quarter

- Distribution date: Payable in late June 2026 to unitholders on record as at 19 May 2026

Revenue fell slightly, but DPU surged — how? The answer lies in the Singapore hospital leases, which we cover in the next section.

Singapore Portfolio: The DPU Driver

ParkwayLife’s three Singapore hospitals — Mount Elizabeth, Gleneagles, and Parkway East — are the backbone of its income. They contribute the majority of revenue and are leased to IHH Healthcare on long-term master leases.

Here is what changed in 1Q 2026 that boosted DPU so sharply:

- Cessation of 3-year rent rebate: From 2022 to 2024, PLife gave rental rebates to its Singapore hospital tenants. Those rebates have now fully lapsed. Full rent is being received again.

- New annual rent review formula: The lease structure for the Singapore hospitals was renegotiated. The new formula includes an annual rent step-up mechanism that kicked in at the start of 2026, directly boosting rental income.

These two structural changes explain why DPU grew 15.1% even as gross revenue dipped slightly. It is a one-off step-up effect — from this point forward, the higher base becomes the new floor.

This is actually a positive signal for long-term investors. The Singapore hospital leases are triple-net, which means PLife bears minimal operating costs. With the rebate period behind us and a new rent escalation formula in place, the recurring income floor has risen permanently.

Japan Portfolio & The Miyako Group Vacancy

ParkwayLife owns 57 nursing home and care facility properties in Japan. The Japan portfolio adds geographic diversification and provides JPY-denominated income — useful as a natural hedge when the Japanese Yen is strong.

However, 1Q 2026 brought one concern: the Miyako Group liquidation. Miyako was a regional operator leasing 5 of PLife’s Japan properties. The company went into liquidation, leaving those 5 properties vacant.

Here is the key context to keep this in perspective:

- The 5 vacant properties represent approximately 1.6% of PLife’s full-year 2026 gross revenue — a small slice of the total

- PLife has retained 4–8 months of security deposits from Miyako, providing a temporary buffer while replacement operators are found

- PLife management is actively marketing the properties to new operators

- Japan care facility demand remains structurally strong, given Japan’s rapidly ageing population

Is this a risk? Yes. But it is a manageable one. The retained security deposits largely offset near-term income loss, and the structural demand for aged care in Japan supports re-leasing. This is not a PLife-specific problem — it is a single operator failure, not a sector downturn.

DPU History: 6 Years of Consistent Growth

One of ParkwayLife REIT’s strongest selling points is its track record of growing DPU year on year. The chart below shows DPU from FY2019 through 1Q 2026 — a clear upward trend even through COVID and the Miyako headwind.

Source: ParkwayLife REIT SGX announcements, FY2019–1Q2026. Past performance is not indicative of future results.

| Financial Year | Full-Year DPU (¢) | YoY Change |

|---|---|---|

| FY2019 | 12.97 | — |

| FY2020 | 13.33 | +2.8% |

| FY2021 | 13.95 | +4.7% |

| FY2022 | 14.21 | +1.9% |

| FY2023 | 14.78 | +4.0% |

| FY2024 | 15.35 | +3.9% |

| 1Q 2026 (quarterly) | 4.42 | +15.1% YoY |

Source: ParkwayLife REIT SGX filings. FY2025 full-year DPU pending completion of remaining quarters.

Debt Management & Balance Sheet Strength

Healthcare REITs are supposed to be defensive. ParkwayLife lives up to that billing with one of the cleanest balance sheets among Singapore REITs.

| Metric | 1Q 2026 | What This Means |

|---|---|---|

| Aggregate Leverage (Gearing) | 35.8% | Well below the MAS 50% limit — ample headroom |

| Interest Coverage Ratio (ICR) | 8.9× | Earnings cover interest costs nearly 9× — very low default risk |

| Weighted Average Debt to Maturity | ~4.1 years | No refinancing cliff in the near term |

| Next Refinancing Due | March 2027 | Plenty of time to refinance at favourable rates |

| JPY Social Loan Secured | JPY 8.8B (10-year) | Long-dated social finance loan locks in stable JPY funding |

| Total Properties | 75 | Across Singapore (3), Japan (57+), France (15) |

Source: ParkwayLife REIT 1Q 2026 SGX announcement, May 2026.

The JPY 8.8 billion 10-year social loan is particularly worth noting. By securing long-dated yen-denominated financing, PLife has effectively matched its currency exposure — JPY debt funded by JPY rental income from its Japan portfolio. This is smart treasury management that reduces FX risk for unitholders.

With the ICR sitting at 8.9×, even a significant spike in interest rates would not threaten PLife’s ability to meet its debt obligations. Compare this to the sector average of 3–4× and you can see why PLife commands a premium valuation.

Peer Comparison: ParkwayLife vs Healthcare & Defensive S-REITs

How does PLife stack up against its peers? The chart below compares dividend yield and gearing ratio across selected healthcare and defensive S-REITs. Note that PLife trades at a lower yield than some peers — but that premium reflects its long unbroken distribution growth record and institutional-quality tenant (IHH Healthcare, a global giant).

Source: SGX announcements, company filings, May 2026. Peer yields and gearing ratios are approximate; data for illustration only. Not investment advice.

| REIT | Approx. Yield | Gearing | Sector |

|---|---|---|---|

| ParkwayLife (C2PU) | ~4.6% | 35.8% | Healthcare |

| First REIT (AW9U) | ~7.8% | 34.2% | Healthcare |

| Keppel DC REIT (AJBU) | ~5.2% | 36.0% | Data Centre |

| CapitaLand Ascendas (A17U) | ~5.5% | 38.2% | Industrial |

| Mapletree Industrial (ME8U) | ~6.5% | 34.0% | Industrial |

Source: SGX, company disclosures, May 2026. Yields are trailing 12-month estimates. Sector comparisons are indicative only.

PLife’s lower yield relative to First REIT or Mapletree Industrial is not a weakness — it reflects its premium quality. Lower yield = higher price premium = market confidence in earnings sustainability. If you want the most defensive healthcare REIT on the SGX with the longest growth streak, PLife is the benchmark.

1Q 2026 Financial Highlights Summary

| Line Item | 1Q 2026 | 1Q 2025 | Change |

|---|---|---|---|

| Gross Revenue | S$38.2M | S$39.0M | -2.1% |

| Net Property Income | S$35.8M | S$36.8M | -2.7% |

| Distribution Per Unit (DPU) | 4.42¢ | 3.84¢ | +15.1% |

| Gearing Ratio | 35.8% | 34.5% | +1.3pp |

| Interest Coverage Ratio | 8.9× | 9.2× | -0.3× |

| No. of Properties | 75 | 74 | +1 |

Source: ParkwayLife REIT SGX filing, 7 May 2026.

What 1Q 2026 Means for You as an Investor

If you hold ParkwayLife REIT units, here is the bottom line from this quarterly update:

- The DPU jump is structural, not a one-off windfall. The rent rebate cessation and new annual review formula represent a permanent step up in the income base. You should expect the higher floor to persist — absent further concessions to tenants.

- Miyako vacancies are a watch item, not a crisis. At 1.6% of gross revenue, even prolonged vacancies are manageable. Security deposits provide a buffer. Watch for re-leasing progress in the 2Q 2026 update.

- Balance sheet gives management options. A 35.8% gearing ratio and 8.9× ICR give PLife the firepower to acquire more assets without needing to raise equity. If a high-quality healthcare property comes to market, PLife can move.

- Analyst consensus remains BUY at S$4.75. At a ~4.6% yield, PLife is priced as a quality defensive name. It is not the highest-yielding S-REIT — but for investors prioritising income reliability over income quantum, it remains a core holding.

If you are considering adding PLife to your portfolio and want to understand how it fits into a broader S-REIT income strategy, check out our guide to best S-REITs in Singapore 2026 and our Singapore retirement calculator to model how dividend income from REITs could support your retirement.

For a broader view on passive income strategies beyond individual REITs, read our article on passive income in Singapore.

How to Buy ParkwayLife REIT in Singapore

ParkwayLife REIT (SGX: C2PU) trades on the Singapore Exchange (SGX) and can be purchased through any brokerage with SGX access. Here are three popular options for Singapore retail investors:

- Syfe Trade: Low commission, good for regular investors. Use the Syfe referral code SRPRFFFCD to get a cash bonus when you sign up.

- FSMOne: Flat S$10 per trade for SGX stocks — cost-effective for larger trades. Access via the FSMOne referral code P0544985.

- IBKR (Interactive Brokers): Best for frequent traders and those who also want access to overseas markets. Referral code: jianxiong368.

For retirement-focused investors, PLife units are also eligible for Endowus via your SRS or CPF Investment Scheme (CPFIS) account — use referral code 2V343 to invest with fee rebates. For context on how REIT investing fits into your CPF strategy, see our CPF investment strategy guide.

Steps to buy PLife on SGX:

- Open a brokerage account (CDP-linked or custodian)

- Fund your account in SGD

- Search ticker C2PU on the SGX market

- Place a limit order at your target price

- PLife pays distributions quarterly — confirm the ex-dividend date before buying if you want the next DPU

Frequently Asked Questions

What is ParkwayLife REIT's DPU for 1Q 2026?

Is ParkwayLife REIT a good buy in 2026?

What is the impact of the Miyako Group liquidation on PLife?

What is ParkwayLife REIT's dividend yield in 2026?

How many properties does ParkwayLife REIT own?

Can I use CPF or SRS to invest in ParkwayLife REIT?

Ready to Invest in S-REITs?

Open an account with one of our trusted broker partners and start building your passive income portfolio today.

The Kopi Notes may earn a referral fee when you sign up using the links above. This does not affect our editorial independence. Not financial advice.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.