Singlife Integrated Shield Plan Review 2026

Is Singlife Shield the Right ISP for You?

Singapore’s integrated shield plans (ISPs) determine which hospital ward you can stay in and how much you pay out of pocket. Singlife Shield is one of the seven MOH-approved ISPs — but how does it stack up against AIA, Great Eastern, and Prudential?

In this review, we break down every Singlife Shield plan tier, 2026 premiums, the Shield Care Rider, and the latest MOH changes so you can decide if Singlife ISP is the right fit.

1. What Is Singlife Integrated Shield Plan?

Singlife (formerly known as Aviva) offers the Singlife Shield range of integrated shield plans. Like all ISPs in Singapore, Singlife Shield sits on top of MediShield Life — your basic national health insurance — and extends coverage to higher ward classes and private hospitals.

Singlife merged with Aviva Singapore in 2022, inheriting a strong book of health insurance policyholders. Today, Singlife Shield is backed by Singlife, one of Singapore’s larger life insurers.

Key Features at a Glance

- MOH-approved ISP with MediShield Life integration

- Premiums payable fully by Medisave (for base plan)

- Covers pre- and post-hospitalisation, day surgery, and cancer drug services

- Optional Shield Care Rider for further cost reduction

- Panel and non-panel hospitals accepted (with cost differences)

You can compare Singlife Shield against all seven ISPs in our integrated shield plan comparison guide.

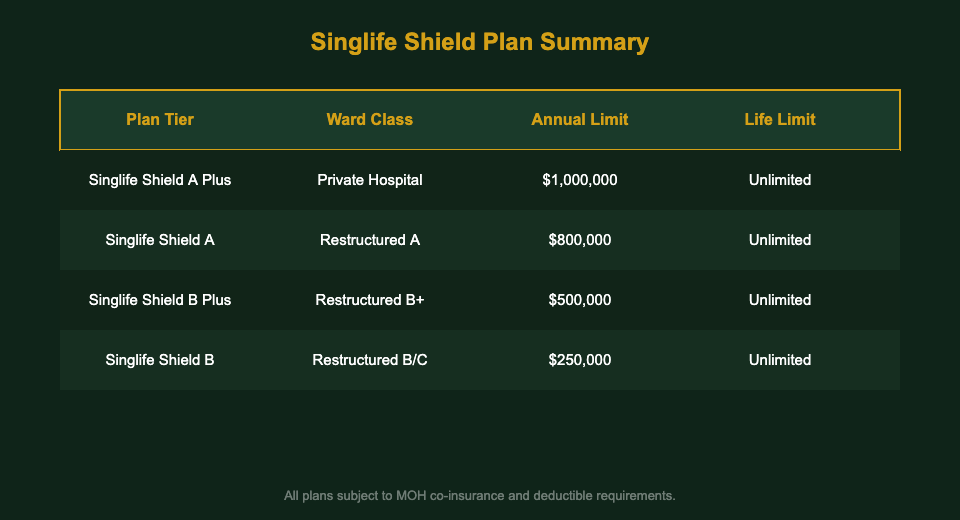

2. Singlife Shield Plan Tiers

Singlife offers four plan tiers, each covering a different hospital ward class:

- Singlife Shield A Plus — Private hospital, up to $1,000,000 per year

- Singlife Shield A — Restructured hospital Class A ward

- Singlife Shield B Plus — Restructured hospital Class B+ ward

- Singlife Shield B — Restructured hospital Class B/C ward

Most Singaporeans opt for Shield A Plus (private) or Shield A (restructured Class A) for a balance of coverage and premium cost.

4. Shield Care Rider & 2026 MOH Changes

Shield Care Rider

Singlife’s Shield Care Rider reduces or eliminates the standard co-insurance (10%) and deductible on your ISP claim. Key features:

- Co-payment as low as 5% (MOH minimum requirement for riders)

- Covers both panel and non-panel surgeons at different co-pay rates

- Must be purchased with cash (Medisave cannot pay for riders)

- Panel surgeons attract lower co-pay; non-panel attracts higher co-pay

MOH 2026 Changes

From 2024 onwards, MOH requires all ISP riders to include a minimum 5% co-payment with no cap waiver. This applies to Singlife’s Shield Care Rider too. What this means:

- Old “full rider” policies that grandfathered pre-2021 are still protected

- New riders from 2021 onwards must include the 5% co-pay

- Using a panel specialist reduces your co-pay significantly

For a full breakdown of the 2026 ISP rider changes, see our ISP rider changes 2026 guide.

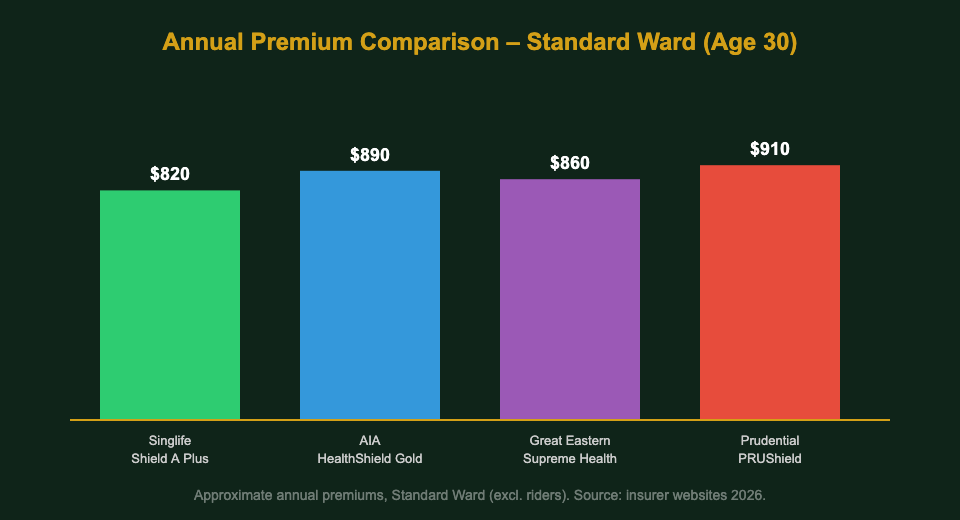

5. Singlife vs AIA vs Great Eastern vs Prudential ISP Comparison

How does Singlife Shield A Plus compare to the three other major ISPs at the private hospital tier?

| Feature | Singlife Shield A+ | AIA HealthShield Gold Max | GE Supreme Health P Plus | Prudential PRUShield Premier |

|---|---|---|---|---|

| Ward Class | Private | Private | Private | Private |

| Annual Limit | $1M | $1.5M | $1.5M | $1.5M |

| Life Limit | Unlimited | Unlimited | Unlimited | Unlimited |

| Age 30 Premium | ~$820/yr | ~$890/yr | ~$860/yr | ~$910/yr |

| Rider Available | Shield Care Rider | Plus Rider | Senior Care Rider | PruExtra Premier |

| Panel Required | No (cost diff) | No (cost diff) | No (cost diff) | No (cost diff) |

| Cancer Drug Cover | Yes | Yes | Yes | Yes |

Key takeaway: Singlife Shield A Plus has a slightly lower annual limit ($1M vs $1.5M for some competitors) but tends to be priced competitively at younger ages. The annual limit difference rarely matters in practice — most hospitalisations cost well under $500,000.

For a full comparison of all seven ISPs, read our Singapore ISP comparison 2026.

6. Who Should Buy Singlife Integrated Shield Plan?

Singlife Shield is a good fit if you:

- Want a MOH-approved ISP from an established Singapore insurer

- Are comfortable with the $1M annual limit (vs $1.5M competitors)

- Prioritise competitive premiums at younger ages

- Plan to use restructured hospitals (Class A or B+) rather than private hospitals

- Already have an existing Singlife or Aviva policy and want consolidation

You might prefer another ISP if:

- You want a higher annual limit ($1.5M+) — consider AIA, GE, or Prudential

- You require a specific panel hospital network

- Your employer offers group ISP with a specific insurer

Building your wealth alongside your health coverage? Check out our guides on Endowus and Syfe for long-term investing in Singapore.

7. How to Apply for Singlife Shield

- Visit Singlife’s website or use the Singlife app to get a premium quote for your age and desired plan tier.

- Declare health history — ISP applications require health declaration. Pre-existing conditions may result in exclusions.

- Select your plan tier — Shield A Plus (private), Shield A (Class A), Shield B Plus, or Shield B.

- Choose rider (optional) — Add the Shield Care Rider if you want to reduce co-payment. Cash required.

- Pay via Medisave — Authorise Medisave deduction for the base plan premium during application.

Note: You can only hold one ISP at a time. If switching from another insurer, ensure continuity of cover — the new policy must start before the old one lapses.

Use our retirement calculator to check how healthcare costs factor into your long-term financial plan.

8. Singlife Integrated Shield Plan FAQ

Is Singlife a reliable insurer for ISP?

Can I pay for Singlife Shield with Medisave?

What is the Singlife Shield annual limit?

Can I switch from another ISP to Singlife Shield?

Does Singlife Shield cover cancer drugs?

What is the Singlife Shield Care Rider co-payment?

Get Free Insurance Advice

Speak with a licensed insurance advisor. No obligation, no cost.

By submitting this form, you agree to our Privacy Policy.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.