Singapore Retirement Calculator 2026: How Much Do You Really Need to Retire?

How much money do you need to retire comfortably in Singapore? The answer depends on your lifestyle, CPF savings, investment income, and when you plan to stop working. This guide walks you through the numbers — with a practical retirement calculator framework, CPF Retirement Sum updates for 2026, and dividend investing strategies to bridge the gap.

The Singapore Retirement Number Formula

The simplest framework for calculating your retirement number is the 25x Annual Expenses Rule (based on the 4% safe withdrawal rate). Here is how it works:

Retirement Number = Annual Expenses × 25

For example: if you need S$4,000/month to live comfortably in Singapore (S$48,000/year), your retirement target is S$1,200,000 in investable assets. At a 4% withdrawal rate, this portfolio sustains 30+ years of withdrawals — backed by decades of historical stock market data.

However, Singapore retirees have a significant advantage: CPF LIFE payouts reduce the portfolio size you need. Your CPF LIFE monthly payout at 65 counts toward your monthly income, so only the gap between CPF LIFE income and your desired monthly spend needs to be funded by your investment portfolio.

Retirement Calculator: How Much Do You Need?

Use the table below to find your retirement target based on monthly spending and CPF LIFE payout. The “Portfolio Needed” column assumes a 4% safe withdrawal rate covering the gap between your CPF payout and your target monthly spend.

| Monthly Spend Target | CPF LIFE Payout (est.) | Monthly Gap | Portfolio Needed (25x) |

|---|---|---|---|

| S$2,500 | ~S$1,600 (BRS) | S$900 | S$270,000 |

| S$3,500 | ~S$2,300 (FRS) | S$1,200 | S$360,000 |

| S$5,000 | ~S$2,300 (FRS) | S$2,700 | S$810,000 |

| S$7,000 | ~S$3,200 (ERS) | S$3,800 | S$1,140,000 |

| S$10,000 | ~S$3,200 (ERS) | S$6,800 | S$2,040,000 |

CPF LIFE payouts are estimates for members who join at 65 with FRS/BRS/ERS set aside. Actual payouts depend on CPF balance at 55, plan type, and deferment age. Refer to cpf.gov.sg for personalised estimates.

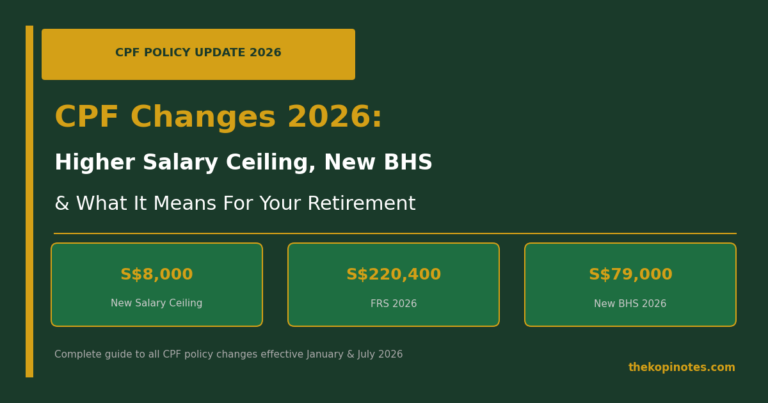

CPF Retirement Sums 2026

The CPF Board sets three retirement sum tiers, adjusted annually. For members turning 55 in 2026:

| Retirement Sum | Amount (2026) | What It Means |

|---|---|---|

| Basic Retirement Sum (BRS) | ~S$106,500 | Minimum payout; requires property pledge |

| Full Retirement Sum (FRS) | ~S$213,000 | Standard payout; 2× BRS |

| Enhanced Retirement Sum (ERS) | ~S$426,000 | Maximum payout; 4× BRS |

Exact figures for 2026 are published by CPF Board and typically announced in the government budget. The numbers above are estimates based on the annual ~3.5% escalation rate. Verify at cpf.gov.sg.

CPF LIFE Monthly Payouts

CPF LIFE (Lifelong Income For the Elderly) provides monthly payouts from age 65 until death. The amount depends on your Retirement Account (RA) balance at 55 and your chosen plan (Standard, Escalating, or Basic).

Under the Standard Plan (most common), estimated monthly payouts for members starting at 65:

- BRS set aside: approximately S$750–900/month

- FRS set aside: approximately S$1,500–1,800/month

- ERS set aside: approximately S$2,900–3,500/month

These payouts are guaranteed for life — making CPF LIFE effectively an annuity paid by the Singapore Government. For retirement planning, always treat CPF LIFE as your income floor, and plan your investment portfolio to top up the gap.

How Dividends and REITs Fill the Retirement Gap

The most popular strategy among Singapore retirees is building a dividend portfolio of S-REITs to generate passive monthly or quarterly income that covers the gap between CPF LIFE payouts and target monthly expenses.

Example: If your CPF LIFE pays S$1,800/month and you want S$4,500/month total, you need an additional S$2,700/month (S$32,400/year) from your portfolio. At a 6% annual distribution yield from a REIT portfolio, you would need approximately S$540,000 in REITs.

This is far less than the S$1,350,000 (= S$4,500 × 12 × 25) you would need without any CPF LIFE income — illustrating the power of CPF LIFE as a retirement foundation.

For REIT selection, see our Best S-REITs in Singapore 2026 guide for current yield rankings and quality analysis.

Retirement Planning by Age: A Singapore Roadmap

| Age | Key Priority | Action |

|---|---|---|

| 20s | Compound growth | Invest CPF-OA in ETFs; start REIT positions; max out SRS |

| 30s | Accumulation phase | Build dividend REIT portfolio; keep CPF-SA at 4%; use Endowus |

| 40s | Wealth protection | Balance growth and income REITs; top up CPF-RA voluntarily |

| 50s | Pre-retirement | Shift to income-heavy REITs; plan CPF LIFE deferment to 70 |

| 60s+ | Income flow | Live on CPF LIFE + REIT dividends; draw down portfolio gradually |

Start Building Your Retirement Portfolio Today

Open an account on these platforms to start investing your CPF or cash savings in S-REITs and income funds:

FAQ: Retirement Planning in Singapore

At what age can I retire in Singapore?

At what age can I retire in Singapore?

”Should

”What

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.