Singlife Multipay Critical Illness II Review: Is It the Best Multi-Pay CI Plan in Singapore? (2026)

Singlife Multipay Critical Illness II is a multi-pay critical illness plan that covers 135 conditions across early, intermediate, and severe stages — with total payouts of up to 900% of your sum assured. Launched in late 2025 as an upgrade to the original Singlife Multipay CI (formerly Aviva MyMultiPay), it adds a market-leading 150% recurrent CI payout and an optional Advance Care Option for bigger first-claim payouts.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted. Speak to a licensed financial adviser before purchasing any insurance product.

- Singlife MPCI II covers 135 CI conditions and pays up to 900% of your sum assured — one of the highest in Singapore.

- You get 150% payout per recurrent CI claim (up to 2 claims), versus the 100% most competitors offer. But premium waiver only kicks in after the first severe-stage CI diagnosis.

- Best for: anyone who wants broad multi-pay CI coverage at a mid-range premium. Not ideal if you need mental illness coverage or a very high sum assured above $250K.

Table of Contents

What Is a Multi-Pay Critical Illness Plan?

A traditional critical illness plan pays out once. You make a claim, get a lump sum, and the policy ends. That worked when survival rates were lower. Today, more Singaporeans survive their first CI diagnosis — and some face a second or third.

A multi-pay CI plan lets you claim multiple times for different conditions, and in some cases, for the same condition recurring. For example, you could claim for early-stage cancer, recover, then claim again years later if you develop heart disease or if the cancer returns.

This matters because the critical illness insurance landscape in Singapore has shifted. According to the Singapore Cancer Registry, over 57% of breast cancer cases are now detected at Stage 1 — up from 33% a decade ago. Early detection means more survivors, which means more people who might face a second health crisis down the road.

Multi-pay plans cost more than single-pay plans. However, they give you a financial safety net that doesn’t vanish after one claim. For someone in their 30s buying CI coverage that lasts until age 75 or beyond, the probability of needing more than one claim isn’t trivial.

Singlife Multipay Critical Illness II: Key Features at a Glance

Singlife Multipay Critical Illness II (MPCI II) was launched in December 2025 as a successor to the original Singlife Multipay CI. The original plan was already well-regarded — it was previously the Aviva MyMultiPay Critical Illness IV before Singlife acquired Aviva Singapore.

Here’s what you’re getting with MPCI II:

| Feature | Details |

|---|---|

| Plan type | Multi-pay critical illness (whole life / term) |

| Conditions covered | 135 (early + intermediate + severe stages) |

| Max payout | 900% of sum assured (CI + Recurrent CI benefits) |

| Recurrent CI payout | 150% per claim, up to 2 claims (300% total) |

| Coverage term | 10 years to age 99 (customisable in 1-year intervals) |

| Premium waiver | Upon first severe-stage CI diagnosis |

| Death benefit | S$5,000 lump sum |

| Currency options | SGD, USD, AUD, GBP, EUR, HKD |

| Annual premium (est.) | ~$1,465/yr (male, age 30, $100K SA, to age 75) |

Source: Singlife Multipay Critical Illness II product brochure, December 2025. Premium estimate from Dollar Bureau comparison data.

The big upgrade from the original MPCI: the Recurrent CI Benefit now pays 150% per claim instead of 100%. That’s a meaningful improvement for worst-case scenarios where cancer returns or you suffer multiple heart attacks.

Singlife also added a new “Special Benefit” covering 34 conditions (up from 27), including things like severe presbycusis and age-related macular degeneration. Each condition pays 20% of your sum assured, capped at $25,000 per life per condition.

How the Payout Structure Works

The payout structure has three layers. Understanding them is important because the waiting periods and caps vary by layer.

Layer 1: CI Benefit (up to 600% of sum assured)

This covers early, intermediate, and severe-stage critical illnesses. You can claim multiple times for conditions in different CI groups. For example, a cancer claim and then a heart disease claim are in different groups, so both are claimable.

Early and intermediate stage claims pay up to 100% each. Severe stage claims pay up to 300% (minus any early/intermediate claims in the same CI group). The total CI Benefit caps at 600%.

There’s a 1-year waiting period between claims at the early/intermediate and severe stages. However, there is no waiting period between an early/intermediate claim and a first severe claim in the same CI group — this is important because it means your premium waiver activates faster.

Layer 2: Recurrent CI Benefit (up to 300% of sum assured)

This is where MPCI II shines. If you’ve already claimed under the CI Benefit and then get diagnosed with one of the 6 specified severe conditions again — or a different one from the list — you get 150% per claim. Up to 2 recurrent claims are allowed, totalling 300%.

The 6 recurrent conditions covered are:

- Major cancers (rediagnosed)

- Heart attack of specified severity (recurring)

- Stroke with permanent neurological deficits (recurring)

- Open-chest heart valve surgery (repeated)

- Major organ / bone marrow transplantation (repeated)

- Coronary artery bypass surgery (repeated)

There’s a 2-year waiting period between recurrent CI claims. This is standard across the industry.

Layer 3: Additional Benefits (uncapped from main benefit)

On top of the main CI and Recurrent CI benefits, you also get:

- Benign and Borderline Malignant Tumour Benefit — 20% of sum assured, max $25,000 per life

- ICU Stay Benefit — 20% of sum assured if you spend 4+ days in ICU, max $25,000 per life

- Special Benefit — 20% of sum assured per condition across 34 conditions, max $25,000 per life per condition, up to 6 claims

Advance Care Option: Trade Recurrence for a Bigger First Payout

Here’s an interesting twist. If your first severe-stage CI diagnosis is one of the 6 specified conditions (listed above), you can choose to exercise the Advance Care Option. This gives you an additional 75% of sum assured on top of your CI Benefit payout.

The catch? Exercising this option permanently cancels your Recurrent CI Benefit. So you’re essentially trading the possibility of future recurrent claims (up to 300%) for an immediate extra 75% payout.

This makes sense if you’re diagnosed with something severe and need a larger lump sum immediately for treatment. It doesn’t make sense if your condition has a high recurrence probability — like certain cancers where relapse within 5 years is common.

How Singlife MPCI II Compares to Other Multi-Pay CI Plans

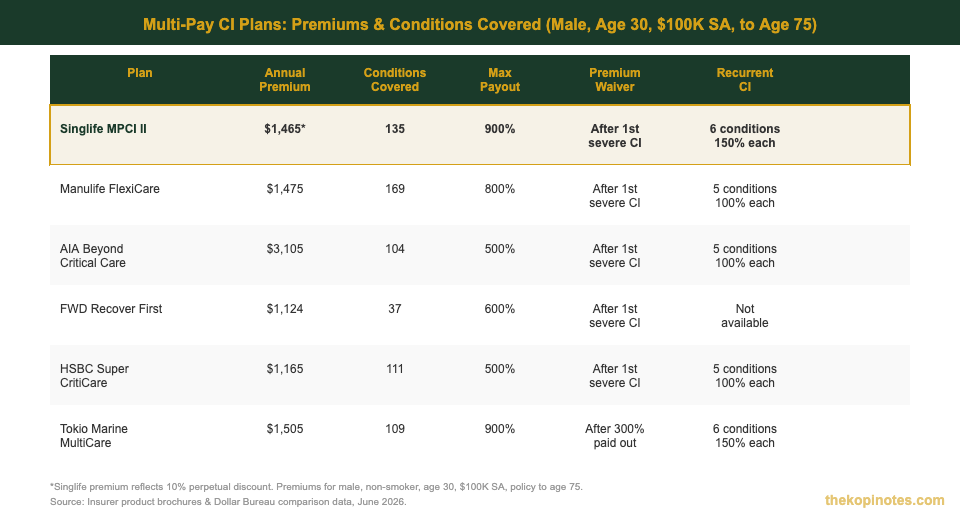

Let’s compare the key multi-pay CI plans available in Singapore as at June 2026. Premium estimates are for a male, non-smoker, age 30, with $100,000 sum assured and coverage to age 75.

| Plan | Annual Premium | Conditions | Max Payout | Recurrent CI | Premium Waiver |

|---|---|---|---|---|---|

| Singlife MPCI II | ~$1,465* | 135 | 900% | 150% × 2 | After 1st severe CI |

| Manulife FlexiCare Deluxe | ~$1,475 | 169 | 800% | 100% × 5 | After 1st severe CI |

| AIA Beyond Critical Care | ~$3,105 | 104 | 500% | 100% × 5 | After 1st severe CI |

| FWD Recover First | ~$1,124 | 37 | 600% | N/A | After 1st severe CI |

| HSBC Super CritiCare | ~$1,165 | 111 | 500% | 100% × 5 | After 1st severe CI |

| Tokio Marine MultiCare | ~$1,505 | 109 | 900% | 150% × 2 | After 300% paid out |

*Singlife premium includes 10% perpetual discount. All premiums are estimates for male, non-smoker, age 30, $100K sum assured, coverage to age 75. Source: Insurer product brochures and comparison sites, June 2026.

Key Takeaways from the Comparison

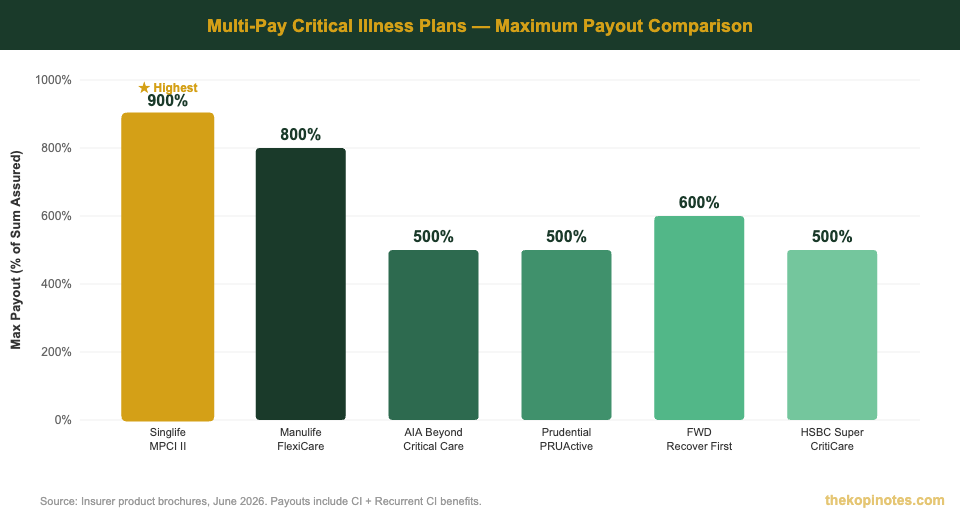

Highest total payout: Singlife MPCI II and Tokio Marine MultiCare are tied at 900%. However, Singlife edges ahead slightly because its premium waiver kicks in after the first severe CI diagnosis, while Tokio Marine requires 300% to be paid out first.

Most conditions covered: Manulife FlexiCare Deluxe covers 169 conditions — 34 more than Singlife’s 135. If breadth of coverage is your top priority, Manulife wins on paper.

Best value: FWD Recover First is the cheapest at ~$1,124/year, but only covers 37 conditions and doesn’t offer recurrent CI coverage. You’re paying less but getting significantly less protection.

Most expensive: AIA Beyond Critical Care costs roughly double the others at ~$3,105/year. It does include mental health conditions — one of very few plans that do — but the premium gap is hard to justify for most buyers.

Who Is Singlife Multipay CI II Best For?

No insurance plan is universally “the best.” Here’s who this plan suits — and who should look elsewhere.

This plan suits you if:

- You want comprehensive multi-pay coverage at a mid-range price. At ~$1,465/year (with the 10% discount), MPCI II offers excellent value for 135 conditions and 900% max payout. It sits in the middle of the pack on price but near the top on benefits.

- You’re concerned about cancer or heart disease recurrence. The 150% recurrent payout (vs the industry-standard 100%) gives you a meaningfully larger safety net if the worst-case scenario happens twice.

- You want flexible coverage duration. You can set coverage from 10 years to age 99 in one-year intervals. Most competitors only offer fixed terms (to age 70, 75, or 85). This flexibility is genuinely useful for fine-tuning your life insurance portfolio.

- You want currency flexibility. If you earn in USD or hold assets in other currencies, being able to denominate your CI coverage in that currency reduces foreign exchange risk.

This plan may NOT suit you if:

- You need coverage for mental health conditions. MPCI II does not cover mental illnesses. If this is important to you, AIA Beyond Critical Care is currently the only major multi-pay plan that includes mental health conditions.

- You need a high sum assured (above $250K). Singlife caps the maximum sum assured at $250,000. Competitors like AIA offer up to $3 million. If you’re a high earner who needs significant CI coverage, this plan alone won’t be enough.

- You prioritise breadth of conditions above all else. Manulife’s FlexiCare Deluxe covers 169 conditions. Singlife covers 135. The gap mainly consists of rarer conditions, but if comprehensive coverage is your non-negotiable, Manulife has the edge.

- You’re looking for the cheapest possible multi-pay CI plan. FWD Recover First and HSBC Super CritiCare are cheaper, though with fewer conditions and lower payouts.

For most Singaporeans in their late 20s to early 40s who want well-rounded multi-pay CI coverage without overpaying, Singlife MPCI II is a strong contender. It’s not the absolute cheapest or the most comprehensive, but it strikes an excellent balance between coverage depth and price.

If you’re still figuring out whether you need critical illness coverage at all, read our guide on critical illness insurance in Singapore first.

Limitations and Things to Watch

Every insurance plan has fine print. Here are the key limitations of Singlife MPCI II that you should be aware of before signing up.

1. No cash value

MPCI II is a pure protection plan with no savings or investment component. If you cancel the policy, you get nothing back. This is standard for multi-pay CI plans, but worth noting if you’re comparing against whole life plans that build cash value.

2. 90-day waiting period for certain conditions

Claims for heart attack, major cancer, and coronary artery disease are not payable if diagnosed within 90 days of the policy start date. This is a standard industry clause, but make sure you’re aware of it.

3. 7-day survival period

You must survive at least 7 days after diagnosis or surgery to be eligible for any CI benefit. Again, this is standard across most CI plans in Singapore.

4. Advance Care Option trade-off

As discussed above, exercising the Advance Care Option gives you an extra 75% payout upfront but permanently cancels your Recurrent CI Benefit. This is a significant decision that should be made carefully — ideally with your financial adviser — at the time of your first severe diagnosis.

5. Small death benefit

The death benefit is only $5,000. This is not meant to replace life insurance. You’ll still need a proper term life insurance plan for death coverage. If you’re building your insurance portfolio from scratch, the Singapore insurance gap report can help you figure out what’s missing.

6. Premiums are not guaranteed

Like all CI premiums, Singlife can adjust rates. This is industry-standard, but don’t assume the premium you pay today will be the premium you pay in 20 years.

How to Buy Singlife Multipay Critical Illness II

You can purchase MPCI II through:

- Singlife Financial Advisers — Singlife’s in-house advisory arm

- Independent financial advisers (IFAs) — many IFAs carry Singlife products

- FSMOne — the DIY insurance platform by iFAST. If you prefer to compare and buy without an adviser, this is an option. Check our FSMOne referral code for sign-up benefits

There’s currently a 10% perpetual premium discount on MPCI II with no minimum sum assured, plus an additional 20% first-year premium discount (applied on top of the perpetual discount). This promotion’s end date isn’t specified, so it’s worth confirming availability when you apply.

Before purchasing any CI plan, make sure your basic insurance stack is in place: disability income insurance, hospitalisation (Integrated Shield Plan), and adequate life coverage. CI insurance is important, but it shouldn’t come at the expense of these essentials.

Frequently Asked Questions

What is the maximum payout for Singlife Multipay Critical Illness II?

The maximum total payout is 900% of your sum assured. This includes up to 600% from the CI Benefit (across early, intermediate, and severe stages) and up to 300% from the Recurrent CI Benefit (150% per claim, up to 2 claims). Additional payouts for benign tumours, ICU stays, and special conditions are on top of this.

How much does Singlife Multipay Critical Illness II cost?

Premiums depend on your age, gender, smoking status, sum assured, and coverage term. As a rough guide, a 30-year-old male non-smoker with $100,000 sum assured and coverage to age 75 pays around $1,465 per year (with the 10% perpetual discount). A 35-year-old female non-smoker with the same parameters would pay less due to lower CI risk at that age.

What is the difference between Singlife Multipay CI and Singlife Multipay CI II?

MPCI II is the upgraded version launched in December 2025. Key improvements include: the Recurrent CI Benefit now pays 150% per claim (up from 100%), the number of conditions covered increased from 132 to 135, the Special Benefit expanded from 27 to 34 conditions, and the premium waiver now activates after the first severe CI diagnosis instead of requiring 300% in payouts.

Does Singlife Multipay Critical Illness II cover mental illness?

No. MPCI II does not cover mental health conditions. If you need mental illness coverage in your CI plan, AIA Beyond Critical Care is currently one of the few multi-pay CI plans in Singapore that includes it. However, AIA’s plan is significantly more expensive.

What is the Advance Care Option in Singlife MPCI II?

The Advance Care Option lets you receive an extra 75% of your sum assured when you’re diagnosed with your first severe-stage CI (must be one of 6 specified conditions). However, exercising this option permanently cancels your Recurrent CI Benefit. It’s a trade-off between getting more money upfront versus keeping the option for future recurrent claims.

Is Singlife Multipay Critical Illness II worth buying?

MPCI II is a strong multi-pay CI plan for most Singaporeans. It offers one of the highest total payouts (900%), covers 135 conditions, and has a competitive premium. It’s particularly good if you want recurrent CI coverage at 150% per claim. However, it may not suit you if you need mental illness coverage, a sum assured above $250K, or the absolute cheapest premium available.

How long is the waiting period between claims?

There’s a 1-year waiting period between early/intermediate and severe-stage CI claims. For recurrent CI claims, the waiting period is 2 years. However, there is no waiting period between an early/intermediate claim and a first severe claim in the same CI group — which means your premium waiver can activate more quickly.

Planning your insurance coverage? Use our retirement planning calculator to figure out how much coverage you actually need. And for a broader view of your financial plan, check out the Singapore insurance gap guide.

Get Free Insurance Advice

Speak with a licensed insurance advisor. No obligation, no cost.

By submitting this form, you agree to our Privacy Policy.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.