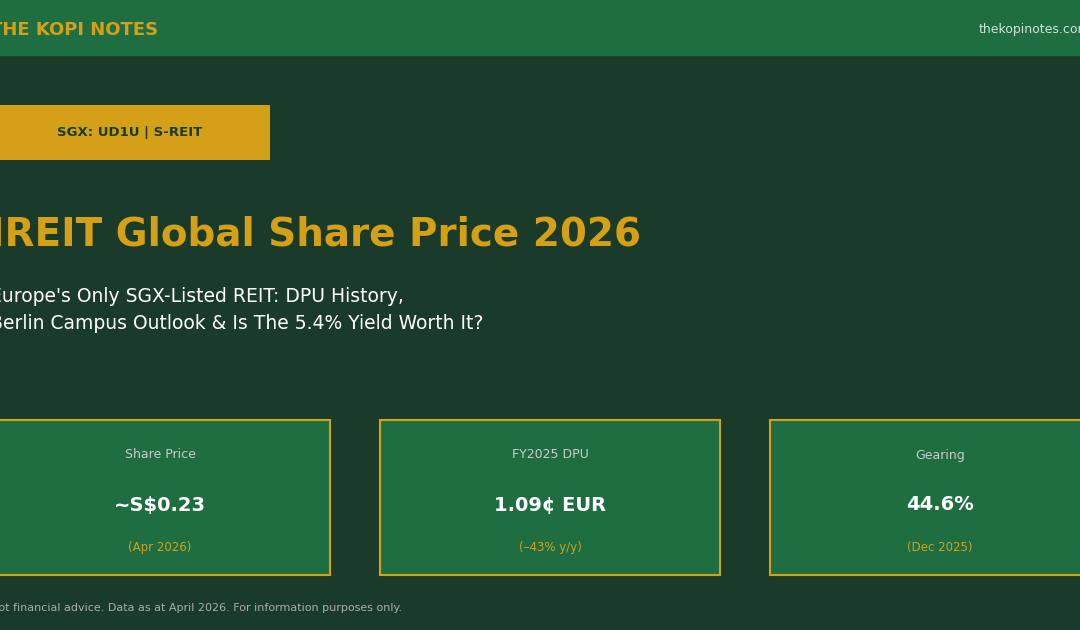

IREIT Global Share Price 2026 (SGX: UD1U): DPU History, 5.4% Yield & Berlin Campus Deep-Dive

Europe’s only SGX-listed REIT is navigating its toughest period yet — but is the beaten-down share price a value opportunity for Singapore income investors? We break down the numbers.

Not financial advice. This article is for informational purposes only. All data referenced is as at April 2026 unless otherwise stated. Always do your own research before making investment decisions.

IREIT Global (SGX: UD1U) is Singapore’s gateway to European commercial real estate — the only S-REIT with a portfolio entirely in Western Europe. With assets spanning Germany, Spain and France, it offers Singapore investors diversification beyond Asia-Pacific. But FY2025 was a brutal year: DPU plunged 43% year-on-year as the vacancy at its flagship Berlin Campus — caused by Deutsche Telekom’s exit — hit income hard.

With shares trading near multi-year lows around S$0.23 and a trailing yield of ~5.4%, the key question for investors is whether the Berlin Campus recovery makes IREIT worth buying at these levels — or whether elevated gearing at 44.6% and ongoing uncertainty make it a value trap.

Table of Contents

Contents — Click to expand

- IREIT Global: Who Is It & What Does It Own?

- Share Price History & Current Trading Level

- DPU History: From Peak to Trough

- Portfolio Deep-Dive: Germany, Spain & France

- The Berlin Campus Problem (And Recovery Plan)

- Gearing, Debt & Financial Position

- Yield Comparison vs S-REIT Peers

- 2026 Outlook: Catalysts & Risks

- Is IREIT Worth Buying at S$0.23?

- FAQ

1. IREIT Global: Who Is It & What Does It Own?

IREIT Global was listed on SGX in August 2014, making it the first Singapore-listed REIT with a portfolio entirely outside Asia. It is sponsored by joint sponsors City Developments Limited (CDL) and Tikehau Capital, and managed by IREIT Global Group Pte. Ltd.

As at December 2025, IREIT’s portfolio comprises:

- 5 freehold office properties in Germany — including the troubled Berlin Campus (Tiergarten/Schöneberg area) and Darmstadt Campus

- 4 freehold office properties in Spain — all located in Madrid

- 44 retail properties in France — a Decathlon-anchored pan-France portfolio fully leased on long WALT leases

Total portfolio value: approximately €798.1 million as at 31 December 2025. Total lettable area: approximately 425,000 sqm. The REIT distributes income in Singapore dollars (from EUR earnings), creating some currency translation effect on SGD DPU figures.

2. Share Price History & Current Trading Level

IREIT Global shares (SGX: UD1U) are trading at approximately S$0.23 per unit as at April 2026 — down significantly from their listing-era highs above S$0.75 in 2018–2019. The decline reflects: the Berlin Campus vacancy shock (Deutsche Telekom exit effective January 2025), rising European interest rates inflating debt costs, and EUR/SGD currency headwinds.

| Period | Approximate Price Range | Context |

|---|---|---|

| IPO (Aug 2014) | S$0.46 | Listing price |

| 2018 Peak | ~S$0.78 | Pre-COVID high |

| 2022–2023 | S$0.40–S$0.50 | Rate hike pressure |

| Early 2025 | ~S$0.32 | Berlin vacancy announced |

| April 2026 | ~S$0.23 | Current (multi-year low) |

The analyst consensus target (from DBS as the joint sponsor research desk) was S$0.32, implying ~39% upside from the current S$0.23 — but that target is predicated on Berlin Campus recovery progressing as planned.

For SGX investors, IREIT trades under ticker UD1U. The EUR-denominated counter trades as 8U7U for those who wish to receive distributions in EUR directly.

3. DPU History: From Peak to Trough

IREIT Global distributes income semi-annually. Distributions are declared in EUR cents per unit but paid to SGD unitholders in Singapore dollars after currency conversion. Below is the annual DPU track record from FY2019 through FY2025:

| Financial Year | DPU (EUR cents) | Change y/y |

|---|---|---|

| FY2019 | 3.66¢ | — |

| FY2020 | 3.88¢ | +6.0% |

| FY2021 | 2.68¢ | –31.0% |

| FY2022 | 2.31¢ | –13.8% |

| FY2023 | 1.87¢ | –19.1% |

| FY2024 | 1.90¢ | +1.6% |

| FY2025 | 1.09¢ | –42.6% |

The DPU peak was FY2020 at 3.88 EUR cents. Since then, IREIT has been on a multi-year declining trend — driven by a combination of lease roll-offs in Germany, rising finance costs as cheap hedged debt repriced higher, and the catastrophic impact of Deutsche Telekom’s decision to exit its entire 100,000 sqm Berlin Campus lease effective 1 January 2025.

The FY2025 2H DPU was particularly alarming at just 0.38 EUR cents — down 59.6% year-on-year — as the full-half impact of Berlin’s vacancy was felt. The management team has indicated it will only consider DPU top-ups (from capital) once the Berlin leasing situation stabilises.

4. Portfolio Deep-Dive: Germany, Spain & France

IREIT’s income comes from three distinct European sub-markets, each with its own dynamics. Here’s how they stack up as at December 2025:

Germany (~47% of portfolio value)

Germany is IREIT’s largest market by value but also its biggest headache. The Berlin Campus (~100,000 sqm of office space in the Telekom-City submarket) became 100% vacant when Deutsche Telekom — IREIT’s largest tenant — exited at the end of 2024. The Darmstadt Campus fared better, with a new 10-year federal government tenant lease signed that raised committed occupancy from 41.3% to approximately 60% by early 2026. Excluding Berlin, the German portfolio occupancy is around 60–65%; including Berlin, it drags the overall German occupancy sharply lower. Germany’s office market faces structural headwinds from work-from-home adoption and subdued demand in the Telekom-City submarket specifically.

Spain (~15% of portfolio value)

IREIT owns four freehold office properties in Madrid — IL Luminoso, IL Palatino, IL Mercurio, and the Parc Cugat asset. Madrid’s office market has shown more resilience than Germany, with active leasing markets and positive rental reversion in some sub-markets. IREIT has been securing lease extensions and new leases in Spain through 2025–2026, maintaining reasonably healthy occupancy. Spain contributes a more stable income stream compared to the German assets.

France (~38% of portfolio value)

France is IREIT’s most defensive asset. The portfolio consists of 44 Decathlon-anchored retail properties spread across France, all on long-dated triple net leases. This portfolio is 100% leased and provides highly predictable, inflation-linked income. The French portfolio is perhaps the underappreciated gem within IREIT’s structure — it anchors income stability while Germany recovers.

Overall portfolio occupancy (including Berlin): 72.7%. Excluding Berlin: approximately 89.4%. Independent valuation: ~€798.1 million.

5. The Berlin Campus Problem (And Recovery Plan)

The Berlin Campus is IREIT’s most important single asset and its biggest near-term challenge. When Deutsche Telekom — which had occupied nearly all of Berlin Campus — vacated its 100,000 sqm lease effective 1 January 2025, IREIT lost its most significant income stream overnight. Understanding what management is doing to solve this problem is key to any investment thesis on IREIT.

What is the Berlin Campus? Located in the Schöneberg district of Berlin, the Berlin Campus is a large-scale mixed-use campus development. IREIT has embarked on a major repositioning programme (internally called “Project REIT”) to transform the campus into a multi-tenanted, mixed-use destination combining office, hospitality, and potentially retail uses.

Phase 1: Hospitality

IREIT has already secured two hospitality tenants for portions of the Berlin Campus:

- Premier Inn — a large extended-stay hotel operator, construction progress at ~23% as at Q1 2026

- Stayery — a serviced apartment brand, construction at ~21%

Both hospitality spaces are expected to be handed over to tenants by October 2027. Phase 1 refurbishment is on budget, though the delivery timeline shifted slightly from mid-2027 to Q2–Q3 2027.

Phase 2: Office Re-leasing

This is the critical unknown. As at the April 2026 AGM, IREIT management indicated that signing of an anchor office lease is now targeted for early Q3 2026. The pipeline includes both large and small potential occupiers. However, IREIT has been cautious — it will only commence Phase 2 fit-out capex once an anchor lease is signed, to avoid over-investing ahead of confirmed demand.

The Telekom-City submarket faces elevated vacancy after Deutsche Telekom vacated large spaces across multiple landlords. IREIT has responded with more flexible lease terms, broker incentives, and reduced effective rents to attract tenants.

Bottom line on Berlin: Until an anchor office tenant is signed and Phase 2 construction commences, Berlin Campus will continue to weigh heavily on DPU. Management estimates the Berlin recovery timeline at 2027–2028 for meaningful income contribution from office space. The hospitality income (Premier Inn, Stayery) provides some interim relief from late 2027 onwards.

6. Gearing, Debt & Financial Position

This is one of the more pressing concerns for IREIT investors. The aggregate leverage ratio as at 31 December 2025 was 44.6% — uncomfortably close to the MAS regulatory limit of 50% for S-REITs. This was driven by two factors: the issuance of S$85 million in green notes in May 2025, and a decline in portfolio valuation (as Berlin Campus zero-income assets were marked down).

| Metric | Value (Dec 2025) |

|---|---|

| Aggregate Leverage | 44.6% |

| Cost of Debt | 2.8% p.a. |

| Estimated Debt Headroom (to 50% limit) | ~€100 million |

| CDL Emergency Facility (Dec 2025) | €12.5 million (2-yr term) |

| Early Loan Repayment (Mar 2026) | €10 million |

| Estimated Leverage (post Mar 2026 repayment) | ~43.5% |

Management has proactively reduced leverage slightly via a €10 million early loan repayment in March 2026, bringing estimated gearing to ~43.5%. The cost of debt jumped from 1.9% (end-2024) to 2.8% (end-2025) — a significant increase given IREIT’s European loan book repricing as hedges roll off. This higher finance cost is one of the secondary drags on FY2025 DPU beyond just Berlin’s vacancy.

The joint sponsor CDL stepped in with a €12.5 million 2-year term loan in December 2025, signalling sponsor support and buying IREIT some liquidity breathing room during the repositioning period. For investors, the gearing situation needs monitoring — any further decline in portfolio values could tighten headroom toward MAS limits.

Want to model IREIT’s gearing vs yield trade-off? Try our S-REIT Gearing Ratio & ICR Calculator or check how IREIT’s yield stacks up with the S-REIT Yield vs SGS Bond Spread Calculator.

7. Yield Comparison vs S-REIT Peers

Based on trailing FY2025 DPU and current share prices as at April 2026, here’s how IREIT Global stacks up against other S-REITs. Note that IREIT’s 5.4% yield reflects a significantly impaired DPU — peers at similar yields are generally in a healthier income position.

IREIT’s ~5.4% trailing yield sits in the middle of the S-REIT peer group — but context matters enormously. ESR-LOGOS (9.4%) and Mapletree Industrial (6.9%) are generating those yields from relatively stable, leased portfolios. IREIT’s 5.4% is based on a DPU that is widely expected to recover as Berlin Campus income resumes. If Berlin stabilises and DPU recovers to, say, 1.5–1.8 EUR cents, the forward yield at today’s share price would be materially higher.

For comparison, our Best S-REITs Singapore 2026 guide covers the full S-REIT sector yield comparison table. IREIT is distinctly positioned as a high-risk, high-potential-reward recovery play rather than a stable income compounder.

To build a diversified dividend portfolio that includes S-REITs, use our Dividend Portfolio Yield Calculator and REITs Dividend Yield Calculator.

8. 2026 Outlook: Catalysts & Risks

Potential Upside Catalysts

- Berlin anchor tenant signed (Q3 2026 target): This is the single biggest catalyst. Signing a major office tenant would confirm the Berlin recovery thesis and give the market visibility on future income. It could meaningfully re-rate the unit price.

- Darmstadt occupancy rising to ~60%+: A new 10-year federal tenant lease has improved Darmstadt’s committed occupancy from 41.3% toward 60%. This reduces German portfolio risk beyond just Berlin.

- EUR/SGD tailwind: If the Euro strengthens vs Singapore Dollar, SGD-denominated DPU will benefit. Singapore investors should monitor EUR/SGD rates when assessing IREIT’s distribution in local currency terms.

- European rate cuts: The ECB’s rate-cutting cycle, if it continues through 2026, could reduce IREIT’s refinancing costs as European loans are repriced at lower rates — directly benefiting net income and DPU.

- France portfolio stability: The 100%-leased Decathlon-anchored French portfolio continues to provide defensive, inflation-indexed income. Any positive lease renewal or expansion in France is upside.

Key Risks

- Berlin delays: If the anchor office tenant signing slips beyond Q3 2026, or if Phase 2 construction is delayed further, DPU recovery will be pushed out. This remains the biggest downside scenario.

- Gearing breach risk: At 44.6% leverage (post-March repayment ~43.5%), IREIT has limited buffer below the 50% MAS regulatory cap. Any further portfolio devaluation could force dilutive equity fundraising.

- Higher-for-longer European rates: IREIT’s cost of debt has already jumped from 1.9% to 2.8%. If European rates stay elevated and hedges continue rolling off at higher rates, finance costs will remain a drag.

- German office market structural weakness: Work-from-home adoption in Germany, combined with the Telekom-City submarket’s elevated vacancy, may slow the pace of re-leasing at Berlin Campus even once refurbishment is complete.

- EUR depreciation risk: IREIT earns in EUR but many investors hold in SGD. A weakening Euro reduces the effective yield received in Singapore dollars.

9. Is IREIT Worth Buying at S$0.23?

IREIT Global at S$0.23 is a high-conviction recovery play — not a passive income hold. Here’s our honest assessment:

Bull case: At S$0.23, the market is pricing in significant pessimism. If Berlin Campus secures an anchor tenant by Q3 2026 as targeted, and if Phase 2 commences construction in 2027, DPU could recover toward 1.8–2.0 EUR cents by FY2027–2028. At that DPU level and current prices, the forward yield would be in the 9–10% range — with potential capital gain back toward NAV (approximately S$0.32–0.35 based on analyst estimates). Total return could be substantial for patient investors.

Bear case: If Berlin tenant signing slips to 2027 or beyond, or if the REIT is forced into a rights issue to manage gearing, unitholders could face significant dilution. The DPU trough may not be over. At 44.6% gearing, there is limited financial flexibility.

Verdict: IREIT is suitable for risk-tolerant investors who believe in the Berlin Campus recovery story and have a 2–3 year investment horizon. It is not suitable for conservative income investors seeking stable quarterly dividends. Position sizing should reflect the elevated uncertainty — many experienced S-REIT investors treat IREIT as a speculative position rather than a core holding. If Berlin tenant news emerges before mid-2026, that is the key catalyst to watch.

10. Frequently Asked Questions

What is IREIT Global's ticker on SGX?

What caused IREIT Global's DPU to fall 43% in FY2025?

Is IREIT Global's dividend sustainable at S$0.23 share price?

When will IREIT Global's DPU recover?

What is IREIT Global's gearing ratio and is it dangerous?

How does IREIT Global compare to other S-REITs for Singapore CPF investors?

Where can I buy IREIT Global shares in Singapore?

Explore More on The Kopi Notes

Researching S-REITs and dividend investing? These resources can help:

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.