CapitaLand Ascott Trust Share Price 2026 (SGX: HMN): DPU, ~6.8% Yield & Investor Guide

Asia-Pacific’s largest hospitality trust — 103 properties, 16 countries, and a stable 6.10¢ FY2025 DPU. Here’s everything you need to know.

CapitaLand Ascott Trust (SGX: HMN) is Asia-Pacific’s largest listed hospitality trust, owning 103 properties with over 18,000 units across 45 cities in 16 countries. For FY2025, it paid a Distribution Per Unit (DPU) of 6.10¢, unchanged year-on-year. At the current share price of ~S$0.895, that translates to a trailing yield of approximately 6.8%. Analysts hold a consensus BUY with a target price of S$1.05–S$1.08, implying 17–21% upside.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

- FY2025 DPU is 6.10¢ (~6.8% yield at S$0.895) — stable and underpinned by divestment gains

- Portfolio of 103 properties across 16 countries offers geographic diversification most Singapore REITs can’t match

- Analyst consensus is BUY with TP S$1.05–S$1.08 — but short-term AEI drag on 1Q2026 earnings is real

Table of Contents

Contents — Click to expand

- What Is CapitaLand Ascott Trust?

- Share Price History 2019–2026

- DPU & Distribution History

- Portfolio Overview: 103 Properties, 16 Countries

- 1Q2026 Business Update: What You Need to Know

- Is the 6.8% Yield Sustainable?

- Peer Comparison: CLAS vs Other S-REITs

- Analyst Targets & Verdict

- How to Buy CLAS (CPF, SRS & Cash)

- Frequently Asked Questions

What Is CapitaLand Ascott Trust?

CapitaLand Ascott Trust (CLAS) is a stapled group comprising CapitaLand Ascott Real Estate Investment Trust and CapitaLand Ascott Business Trust. It was formerly known as Ascott Residence Trust (ART) before rebranding. CLAS has been listed on the Singapore Exchange (SGX) since 2006.

Its mandate is to invest in income-producing real estate used as serviced residences, rental housing, student accommodation, and other hospitality assets globally. Properties operate under well-known brands including Ascott, Somerset, Quest, and Citadines.

With an asset value of S$8.9 billion as at 31 March 2026 across 103 properties in 45 cities and 16 countries, CLAS is the largest hospitality trust in Asia-Pacific. That’s an important distinction — most Singapore REITs focus on a single asset class or country. CLAS gives you built-in geographic diversification.

The trust earns income from a mix of management contracts, master leases, and direct hotel ownership — a blend that balances stable rental income with upside exposure to the hospitality cycle.

CLAS Share Price History 2019–2026

CLAS has seen significant price swings over the past six years, largely driven by COVID-19 in 2020–2021 and the subsequent hospitality recovery. Here’s the approximate year-end share price range:

| Year | Approx. Price Range (S$) | Key Theme |

|---|---|---|

| 2019 | 1.14 – 1.32 | Pre-COVID peak; merger with Ascendas Hospitality |

| 2020 | 0.72 – 1.08 | COVID collapse; travel bans hit occupancy |

| 2021 | 0.89 – 1.10 | Gradual recovery; vaccinations boost travel |

| 2022 | 0.92 – 1.14 | Travel boom; RevPAU surges past pre-COVID levels |

| 2023 | 0.88 – 1.15 | DPU recovery to 6.57¢; rate headwinds emerge |

| 2024 | 0.83 – 1.02 | DPU flat; higher-for-longer rates pressure |

| 2025 | 0.85 – 0.99 | DPU stable at 6.10¢; AEI investments begin |

| 2026 YTD | ~0.895 (Jun) | AEI drag; Japan portfolio expansion |

Source: SGX, investing.com, analyst estimates. Prices are approximate annual ranges.

The current price of ~S$0.895 sits near the lower end of recent years — at a discount to the 2022–2023 travel recovery peak. The 52-week range is S$0.85–S$0.99.

CLAS DPU & Distribution History FY2020–FY2025

Distribution Per Unit (DPU) — the cash paid to each unit you own — tells you how income has grown over time. CLAS pays semi-annually, in February and August each year.

| Fiscal Year | Annual DPU (¢) | YoY Change | Trailing Yield (at year-end price) |

|---|---|---|---|

| FY2020 | 1.05 | – | ~1.3% |

| FY2021 | 4.58 | +336% | ~4.2% |

| FY2022 | 5.14 | +12.2% | ~5.3% |

| FY2023 | 6.57 | +27.8% | ~6.5% |

| FY2024 | 6.10 | –7.2% | ~6.7% |

| FY2025 | 6.10 | 0% | ~6.8% |

Source: CapitaLand Ascott Trust investor relations, Growbeansprout.com. Data as at June 2026.

The big takeaway: DPU crashed in 2020 when COVID shuttered global travel, then recovered sharply as borders reopened. FY2023 was the peak at 6.57¢ — partly boosted by divestment gains. FY2024 and FY2025 are both at 6.10¢, which management committed to as a floor.

Management retained S$23.2 million in non-periodic items to fund AEIs, which is why total income available for distribution rose 11% but DPU held flat. That’s prudent capital management — not weakness.

Portfolio Overview: 103 Properties, 16 Countries

CLAS’ portfolio is its strongest differentiator. No other S-REIT offers this level of geographic spread — across Asia Pacific, Europe, and the United States.

| Region | Key Markets | 1Q2026 RevPAU Trend |

|---|---|---|

| Singapore | Singapore | +2% YoY |

| Australia | Sydney, Melbourne, Perth | +7% YoY (AUD 188) |

| Japan | Tokyo, Osaka, Hiratsuka | +3% YoY same-store |

| Europe | London, Paris, Hamburg | AEI drag (renovations) |

| USA | New York | AEI drag (renovations) |

| Rest of Asia | Vietnam, Philippines, China | Steady recovery |

Source: CapitaLand Ascott Trust 1Q2026 Business Update, April 2026.

In 2026, CLAS added three Japan rental housing properties near Greater Tokyo for approximately ¥4.6 billion (~S$42 million). Japan is now a core growth pillar — rental housing there provides stable, yen-denominated income with long leases, a useful counterbalance to the more volatile hotel income in other markets.

1Q2026 Business Update: What You Need to Know

CLAS released its 1Q2026 business update in April 2026. Portfolio RevPAU dipped to S$137, with overall occupancy at 77%. The drag is clear: ongoing AEI works in London, Hamburg, New York, and Paris temporarily restricted rooms. Strip those out and same-store RevPAU rose 1% year-on-year — the underlying portfolio is growing.

- Portfolio RevPAU: S$137 | Overall occupancy: 77%

- Same-store RevPAU (ex-AEI): +1% YoY

- Australia RevPAU: AUD 188 (+7% YoY)

- Japan same-store RevPAU: +3% YoY

- Singapore RevPAU: +2% YoY

The Cavendish London AEI is the most significant current project, expected to complete in 2027. Once done, London — one of the world’s top hotel markets — should contribute significantly higher RevPAU. The renovation headwind is temporary and deliberate.

Is the 6.8% Yield Sustainable?

What supports it: Gearing of 38.9% is well within MAS’ 50% limit, giving CLAS ~S$1.9 billion of debt headroom. Income available for distribution rose 11% in FY2025 to S$256.7 million — management retained some for AEIs. Total distribution of S$233.5 million was up 1% YoY. The underlying business is growing.

What could pressure it: Currency headwinds across 16 countries are the biggest risk. The AEI drag in 1Q2026 is a near-term earnings headwind (resolves by 2027). Occupancy at 77% is still ~5ppt below pre-COVID normalised levels.

| DPU Scenario | Annual DPU (¢) | Yield at S$0.895 | Assumption |

|---|---|---|---|

| Bear | 5.50 | 6.1% | Currency drag; AEI extends; occupancy flat |

| Base | 6.00 | 6.7% | Stable distributions; AEI completes 2027 |

| Bull | 6.60 | 7.4% | Occupancy normalises; AEI uplifts RevPAU |

Source: TKN estimates based on FY2025 reported figures. Not financial advice.

The base case ~6.0–6.1¢ DPU is highly defensible. The bear case requires multiple simultaneous negatives. The bull case is plausible by 2027–2028 once AEIs complete. For more on REIT income strategies, see our passive income Singapore guide.

Peer Comparison: CLAS vs Other S-REITs

| REIT | Ticker | Sector | Yield (Est.) | Gearing |

|---|---|---|---|---|

| CapitaLand Ascott Trust | HMN | Hospitality | ~6.8% | 38.9% |

| ParkwayLife REIT | C2PU | Healthcare | ~4.6% | 33.4% |

| Suntec REIT | T82U | Office/Retail | ~5.7% | 43% |

| OUE REIT | TS0U | Diversified | ~7.2% | 35.5% |

| Starhill Global REIT | P40U | Retail/Office | ~6.8% | 35.5% |

| CICT | C38U | Commercial | ~5.5% | 39.6% |

| Keppel DC REIT | AJBU | Data Centre | ~4.5% | 36% |

Source: TKN compilation from SGX, company reports, analyst estimates. Data as at June 2026. Not a recommendation.

CLAS offers a competitive 6.8% yield with gearing at 38.9% — comfortably mid-range. The standout differentiator is portfolio breadth: 103 properties across 16 countries vs the typical S-REIT’s single-country focus. For a wider view, see our best S-REITs Singapore 2026 comparison.

Analyst Targets & Verdict: Buy, Hold or Sell?

Eight analysts cover CLAS, with six holding BUY. The consensus target price is S$1.05–S$1.08 vs the current ~S$0.895 — representing 17–21% potential upside, not including the 6.8% yield.

| Scenario | Rating | Target Price (S$) | Key Thesis |

|---|---|---|---|

| Consensus | BUY | 1.05–1.08 | Top pick in hospitality; geographic diversification |

| Bull Case | Strong BUY | 1.42 | Full occupancy recovery + AEI uplifts by 2027 |

| Bear Case | HOLD/SELL | 0.88 | AEI overruns; currency drag; occupancy miss |

Source: Investing.com consensus, POEMS research April 2026. Not financial advice.

CLAS suits investors wanting: (1) higher yield than blue-chip commercial REITs, (2) global portfolio exposure in a single SGX unit, (3) confidence in the travel recovery thesis through 2027. Less suitable for very risk-averse investors who prefer the stability of industrial or healthcare REITs. For CPF strategies, our CPF investment strategy guide covers OA investing alongside REITs.

How to Buy CLAS (CPF, SRS & Cash Account)

CLAS is listed on SGX under ticker HMN. You can buy it through any SGX-connected brokerage.

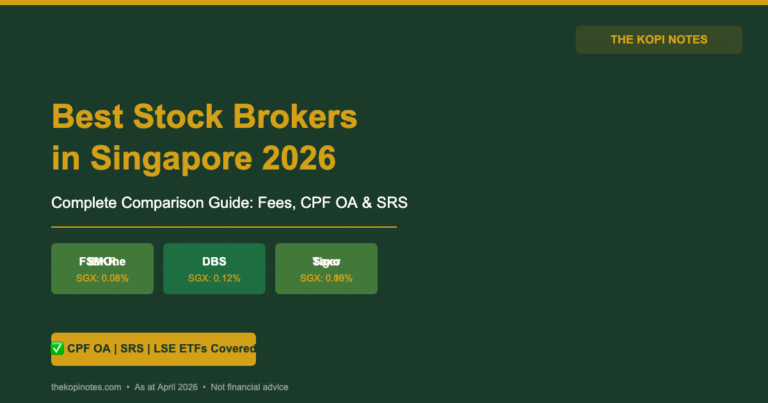

| Broker | CPF (CPFIS-OA)? | SRS? | Min. Commission |

|---|---|---|---|

| FSMOne | Yes | Yes | 0.08% (min S$8.80) |

| DBS Vickers | Yes | Yes | 0.12% (min S$25) |

| IBKR | No | No | ~S$1.70 flat |

| Syfe Trade | No | No | S$0 (first 3 free/mo) |

Source: Broker websites, TKN compilation. Data as at June 2026.

Note that CLAS is a stapled security — always verify CPFIS eligibility on the CPF Board’s approved investment list before purchasing with CPF funds.

New to FSMOne? Use our FSMOne referral code P0544985. Prefer a robo-advisor? Syfe (code SRPRFFFCD) and Endowus (code 2V343) both offer REIT portfolios. Use our free Singapore retirement calculator to plan your income targets.

Frequently Asked Questions

What is CapitaLand Ascott Trust's SGX ticker?

What is CLAS' current DPU and dividend yield?

How many properties does CapitaLand Ascott Trust own?

Is CapitaLand Ascott Trust eligible for CPF investment?

What is the gearing ratio of CapitaLand Ascott Trust?

What are analysts saying about CLAS in 2026?

Why did CLAS DPU fall from FY2023's 6.57¢ to 6.10¢?

What are the key risks of investing in CLAS?

How does CLAS compare to other Singapore hospitality REITs?

What is RevPAU and why does it matter for CLAS?

Disclaimer: This article is for educational and informational purposes only. It does not constitute financial advice. Always do your own research before investing. Past distributions are not a guarantee of future distributions. The Kopi Notes may earn referral fees from broker links on this page.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.