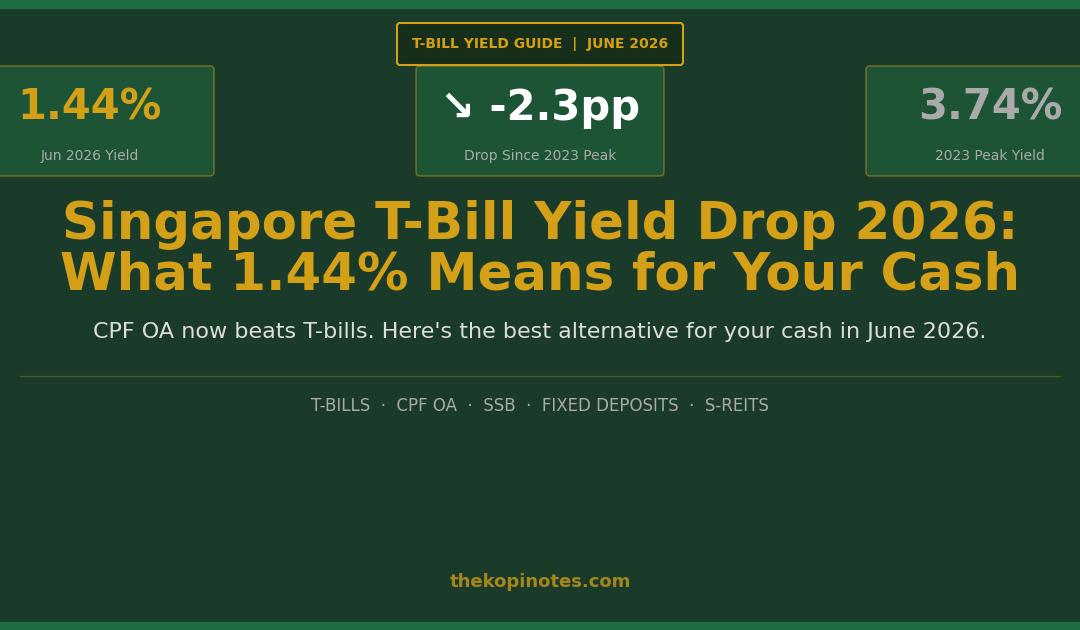

Singapore T-Bill Yield Drop 2026: What 1.44% Means for Your Cash

June 2026 | 6-month yields at ~1.40–1.45% — down from 3.7% in 2023. Here’s what to do now.

Singapore’s 6-month Treasury Bill (T-bill) yield has fallen sharply from a peak of ~3.74% in early 2023 to just 1.40–1.45% in mid-2026 — a drop of more than 2.3 percentage points. The June 2026 auctions closed near 1.44%, and the upcoming 4 June auction (BS26111H) is expected to clear around 1.40–1.45%. For Singapore investors who relied on T-bills for near-risk-free income, this matters: a S$100,000 T-bill position now earns roughly S$1,450 per six months instead of S$1,870. This guide explains the reasons behind the yield drop, what alternatives pay more, and how to rebalance your cash strategy in 2026.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

Table of Contents

Contents — Click to expand

- Singapore T-Bill Yield History 2022–2026

- Why Did Singapore T-Bill Yields Drop So Much?

- June 2026 T-Bill Auction: What to Expect

- Impact on Singapore Cash Investors

- Best Alternatives to T-Bills in 2026

- T-Bill vs CPF OA vs SSB vs Fixed Deposit Comparison

- S-REITs and Dividend Stocks: Higher Yield, Different Risk

- 2026 Cash Strategy Action Plan

- Frequently Asked Questions

Singapore T-Bill Yield History 2022–2026

Singapore T-bill yields had a remarkable run from 2022 to early 2023 as the US Federal Reserve hiked rates aggressively. The 6-month T-bill yield peaked at approximately 3.74% in early 2023, making it one of the most attractive near-risk-free returns available to Singapore retail investors. By mid-2024, yields had eased to around 3.3–3.5%. In 2025, as the Fed began cutting rates and global recession fears cooled, Singapore T-bill yields fell further — reaching the 2% range by Q3 2025 and then dropping below 1.5% by early 2026.

The trajectory in 2026 has been particularly steep. The January 27, 2026 one-year T-bill (BY26100S) closed at 1.44%. The March/April 2026 six-month auctions briefly touched 1.40% before a minor rebound to 1.47% in April 2026. The May 21 auction closed at 1.45%, and the secondary market yield on May 26 was 1.41%.

| Period | 6-Month T-Bill Cut-Off Yield | Direction |

|---|---|---|

| Q1 2023 (Peak) | ~3.74% | 📈 Peak |

| Q1 2024 | ~3.50% | ↘ Easing |

| Q3 2025 | ~2.00–2.20% | ↘ Declining |

| Jan 2026 | ~1.44% | ↘ Sharp drop |

| Apr 2026 (Brief high) | ~1.47% | ↗ Minor rebound |

| May 7, 2026 | 1.40% | ↘ Near-low |

| May 21, 2026 | 1.45% | ↗ Mild recovery |

| Jun 4, 2026 (forecast) | ~1.40–1.45% | ➡ Sideways |

Source: MAS Auctions and Issuance Calendar, Growbeansprout.com, June 2026

Why Did Singapore T-Bill Yields Drop So Much?

Singapore T-bill yields track short-term US interest rates closely because Singapore’s monetary policy operates within MAS’s Singapore Dollar Nominal Effective Exchange Rate (S$NEER) framework — and global capital flows keep SGD short rates anchored near USD short rates. The primary driver of the 2026 yield decline is the US Federal Reserve’s rate-cutting cycle that began in late 2024. By mid-2026, the Fed funds rate has been cut from its 5.25–5.50% peak, pulling short-term rates globally lower.

Three secondary factors accelerated the Singapore T-bill yield drop:

1. Strong demand at auctions. T-bill applications in May 2026 reached S$18.0 billion against an issuance size of S$8.5 billion — an oversubscription ratio of more than 2×. High demand with fixed supply naturally pushes cut-off yields down.

2. Safe-haven flows. Global geopolitical uncertainty and equity market volatility through 2025–2026 pushed conservative Singapore investors and institutions into SGS (Singapore Government Securities), compressing yields further.

3. MAS issuance management. MAS increased 6-month T-bill issuance to S$8.5 billion per auction — the highest on record — which has helped meet demand without allowing yields to fall even more.

The 10-year Singapore government bond yield was 2.05% as at May 28, 2026, while the US 10-year was 4.50%. The unusually wide gap reflects Singapore’s safe-haven status and local demand dynamics.

June 2026 T-Bill Auction: What to Expect

The upcoming 6-month T-bill auction (BS26111H) is scheduled for 4 June 2026 with an issuance size of S$8.5 billion — same as the previous auction. Applications using cash close at 9pm on 3 June. CPF-OA applications via DBS and OCBC also close at 9pm on 3 June; UOB CPF-OA closes earlier at 9pm on 2 June.

Based on market indicators as at late May 2026, the secondary market yield was 1.41% — slightly below the May 21 cut-off of 1.45%. If demand stays elevated (applications ≥ S$18B), the June 4 cut-off yield could settle in the 1.40–1.44% range. A meaningful rebound above 1.50% would require either a spike in US short rates or a significant pullback in domestic T-bill demand — neither is likely near-term.

For Singapore investors applying non-competitively (the most common retail approach), you accept the auction cut-off yield. At current levels, the effective return on a 6-month S$100,000 T-bill is approximately S$700–S$725 for six months — down from S$1,870 at the 2023 peak.

Impact on Singapore Cash Investors

The T-bill yield drop from 3.74% to ~1.44% represents a 57% cut in income for investors who rotate cash through T-bills. A Singapore investor with S$200,000 in T-bills who rolled them every six months at 3.7% earned approximately S$7,400/year. At 1.44%, that same position earns just S$2,880/year — a S$4,520 annual income shortfall.

This matters most for three groups. Retirees using T-bills for income have seen a meaningful income source compress to near-CPF OA levels — diversifying into higher-yielding instruments is now more urgent. Emergency fund investors find T-bills still viable for the liquidity pot given their government backing, but the yield edge over savings accounts has narrowed substantially. CPF-OA investors face the starkest math reversal: CPF OA’s guaranteed 2.50% p.a. now significantly outpaces the 6-month T-bill yield of ~1.44%, meaning the old strategy of using CPFIS-OA to buy T-bills now actually costs you 1 percentage point per year versus staying in CPF OA.

Best Alternatives to T-Bills in 2026

With T-bill yields at multi-year lows, Singapore investors are actively looking for alternatives. Here are the key options, ranked by yield — with the caveat that higher yield means either more risk, less liquidity, or a longer lock-up period.

| Instrument | Indicative Yield (Jun 2026) | Liquidity | Risk |

|---|---|---|---|

| S-REITs (top 10 avg) | 5.5–9.5% | High (SGX-listed) | Market risk, DPU variable |

| CPF Special Account / RA | 4.00% | Low (locked in CPF) | Government-guaranteed |

| Endowus / Syfe Income+ (SRS) | 3.0–4.5% | Medium | Low-medium (bond/hybrid) |

| Singapore Savings Bonds (SSB) | 1.46% (1-yr) / 2.11% (10-yr avg) | High (redeem any month) | Government-guaranteed |

| CPF Ordinary Account | 2.50% | Low (CPF withdrawal rules) | Government-guaranteed |

| Fixed Deposits (6-month best) | ~1.50% | Low (locked for tenor) | SDIC-insured up to S$100k |

| 6-month T-bill (current) | ~1.40–1.45% | Medium (hold to maturity) | Government-guaranteed |

Source: MAS, CPF Board, DBS, June 2026. Yields are indicative and subject to change.

The key insight: T-bills have gone from the clear winner in 2023 to one of the least attractive safe options in 2026. Their only remaining advantages are government guarantee, CPF-OA/SRS access, and certainty of cut-off yield.

T-Bill vs CPF OA vs SSB vs Fixed Deposit: Detailed Comparison

For Singapore investors deciding where to park cash or CPF funds right now, here is a side-by-side breakdown of the four most common safe-haven options as at June 2026.

| Feature | 6M T-Bill | CPF OA | SSB | Fixed Deposit |

|---|---|---|---|---|

| Current yield | ~1.44% | 2.50% | 1.46% (1-yr) / 2.11% (10-yr) | ~1.50% (best 6M) |

| Minimum investment | S$1,000 | N/A | S$500 | S$5,000–S$20,000 |

| Maximum per person | Unlimited | Unlimited | S$200,000 | Unlimited (SDIC covers S$100k) |

| Liquidity | Hold 6M or sell secondary market | Limited by CPF rules | Redeem any month, no penalty | Locked; early = 0% interest |

| CPF OA eligible? | Yes (CPFIS-OA) | N/A | Yes | Some banks |

| SRS eligible? | Yes | No | Yes | Yes |

| Verdict Jun 2026 | ❌ Below CPF OA rate | ✅ Best guaranteed return | ✅ SSB 10-yr avg beats T-bill | ⚠️ Marginally better, less flexible |

Source: MAS, CPF Board, bank websites, June 2026. All yields approximate.

For CPF OA investors: keeping money in CPF OA at 2.50% now clearly beats rolling into T-bills at 1.44%. The only reason to still use T-bills via CPFIS-OA is if you want secondary market access — a slim advantage at current yields. For the full T-bill mechanics guide, see Singapore T-bills 2026 guide. For the head-to-head, see our T-bill vs CPF OA 2026 comparison.

S-REITs and Dividend Stocks: Higher Yield, Different Risk

For investors willing to accept market price volatility in exchange for a much higher income yield, Singapore-listed REITs (S-REITs) remain one of the most compelling options. As at June 2026, the top S-REITs by yield include Sasseur REIT at approximately 9.5%, Elite UK REIT at ~8.8%, AIMS APAC REIT at ~6.9%, and even blue-chip names like Mapletree Logistics Trust (~6.1%) and Frasers Centrepoint Trust (~6.0%) — all significantly above the 1.44% T-bill rate.

The critical difference: S-REIT distributions are variable (not guaranteed), and unit prices fluctuate. When T-bill yields were 3.7% in 2023, the spread between T-bill yields and S-REIT yields had compressed to historically thin levels. At 1.44%, the risk premium gap is now 4–5 percentage points for most REITs — much more attractive for income investors willing to hold through volatility.

Two practical ways to access diversified S-REIT income: the Lion-Phillip S-REIT ETF (CLR) offers ~5.5% trailing yield with 0.60% TER across ~30 S-REITs (see Singapore REIT ETF guide), and robo-advisor income portfolios via Endowus (referral 2V343) or Syfe (referral SRPRFFFCD) targeting 3–5% distributions with SRS/CPF eligibility. For a full breakdown of the best S-REITs in Singapore 2026, including DPU sustainability analysis, see the dedicated guide.

2026 Cash Strategy Action Plan for Singapore Investors

Given T-bill yields near 1.44% and the wide range of alternatives available, here is a practical reallocation framework by investor profile:

| Investor Profile | Recommended Cash Strategy |

|---|---|

| Emergency fund (3–6 months expenses) | High-yield savings account or SSB — keep liquid. T-bills still OK but no yield edge over some savings accounts. |

| CPF OA investor | Stop using CPFIS-OA for T-bills. Leave in CPF OA at 2.50% — now outperforms T-bills by ~1 percentage point. |

| SRS investor | Consider shifting SRS T-bills to Endowus or Syfe Income+ portfolios (3–5% target yield) or SSB for better returns. |

| Income investor (retiree/near-retirement) | Rebalance toward blue-chip S-REITs (5–7% yield), REIT ETFs (CLR), and CPF LIFE top-ups. T-bills for liquidity buffer only. |

| Growth investor (long horizon) | Reduce T-bill allocation to liquidity minimum. Put long-term capital into CSPX/VWRA (global equities) or S-REITs. |

Source: The Kopi Notes analysis, June 2026. Not financial advice.

Use the Singapore retirement calculator to model how different yield assumptions on your cash affect your retirement timeline. For T-bill and SSB access via CDP, FSMOne (referral P0544985) is the lowest-cost brokerage option.

Frequently Asked Questions

Why has the Singapore T-bill yield dropped so much in 2026?

The main driver is the US Federal Reserve’s rate-cutting cycle that began in late 2024. Singapore T-bill yields track US short-term rates closely through the SGD NEER framework. In addition, extremely strong demand — S$18 billion applications against S$8.5 billion issued in May 2026 — pushed cut-off yields down further. The 6-month yield fell from ~3.74% in early 2023 to ~1.40–1.45% by mid-2026.

Should I still invest in T-bills in June 2026?

T-bills still make sense as part of a liquidity buffer — they are government-guaranteed and available via cash, CPF-OA, and SRS. However, at ~1.44%, T-bills no longer offer a yield advantage over CPF OA (2.50%) or Singapore Savings Bonds (2.11% for 10-year average). For income beyond the emergency fund, alternatives like S-REITs, robo-advisor income portfolios, or SSBs now offer better risk-adjusted returns.

What yield should I expect from the 4 June 2026 T-bill auction?

Based on market indicators as at late May 2026 — secondary market yield of 1.41%, continued high demand (~S$18B applications), and unchanged issuance of S$8.5B — the June 4 auction (BS26111H) is expected to clear around 1.40–1.44%. A significant rebound above 1.50% would require a notable rise in US short rates or a sharp drop in domestic demand, neither of which is expected near-term.

Is CPF OA better than T-bills now?

Yes — CPF OA pays a guaranteed 2.50% p.a., significantly more than the current T-bill yield of ~1.44%. Previously, when T-bill yields exceeded 2.50%, investors using CPFIS-OA to buy T-bills could earn more than leaving money in CPF OA. That math has reversed. As at June 2026, keeping money in CPF OA clearly beats T-bills by approximately 1 full percentage point per year.

How do I apply for the Singapore T-bill using cash?

Apply through DBS, OCBC, or UOB internet banking. Applications for the June 4 auction close at 9pm on June 3 (DBS/OCBC) or 9pm on June 2 (UOB). Select “non-competitive bid” to accept the auction cut-off yield. T-bills are issued at a discount and you receive face value at maturity (6 months). Minimum investment is S$1,000.

Can I use SRS funds to buy T-bills?

Yes. Singapore T-bills are eligible for SRS investment, allowing you to defer tax on interest income until retirement. However, with yields at ~1.44%, consider whether SRS funds might generate higher returns in an income-oriented portfolio — for example, Endowus Income+ or Syfe Income+ portfolios target 3–5% distributions, significantly above current T-bill yields.

Will Singapore T-bill yields recover back above 3% again?

A recovery back to 3%+ would require the Fed to reverse course and begin hiking rates — currently not in base-case forecasts for 2026 or 2027. Most market expectations see SGD short rates staying in the 1.3–1.7% range through end-2026. However, if US inflation re-accelerates or geopolitical shocks destabilise global bond markets, yields could spike higher relatively quickly.

What is the difference between Singapore T-bills and Singapore Savings Bonds?

Both are government-guaranteed SGS instruments. T-bills: 6-month or 1-year maturity, must hold to maturity or sell on secondary market, S$1,000 minimum, available via CPF-OA/SRS/cash. SSBs: up to 10-year maturity with step-up interest (higher in later years), redeemable any month without penalty, S$500 minimum, maximum S$200,000 per person. As at June 2026, SSBs offer a better 10-year average return (2.11%) than T-bills (1.44%), making SSBs more attractive for longer horizons.

What are the best investments for passive income in Singapore in 2026?

With T-bill yields at 1.44%, investors seeking meaningful passive income should look beyond T-bills. Top options: S-REITs (5–9%+ yield, market risk), CPF Special/RA top-ups (4% guaranteed), SSBs (2.11% 10-yr avg, flexible), Endowus/Syfe income portfolios (3–5% target, SRS-eligible), and blue-chip dividend stocks. See the passive income Singapore 2026 guide for a full breakdown.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.