AIA HealthShield Gold Max: Complete 2026 Review (Plan A, B, Premiums & New Rider Rules)

Singapore’s most comprehensive AIA integrated shield plan guide — coverage tiers, premium tables, the April 2026 MOH rider changes, and who should pick which plan.

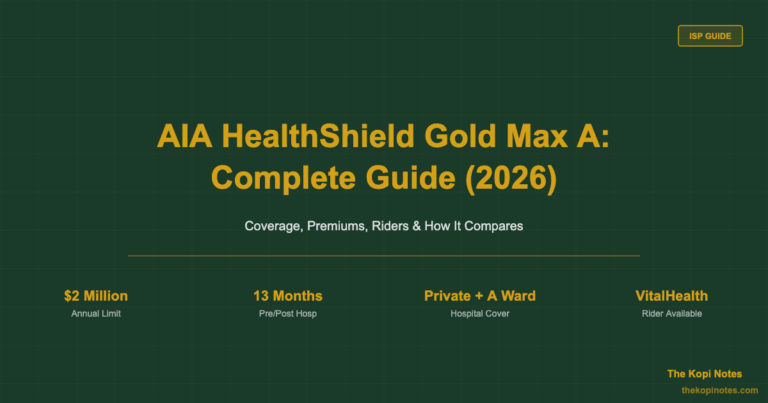

AIA HealthShield Gold Max is an Integrated Shield Plan (ISP) that extends your MediShield Life coverage to include private hospitals and A-class wards. Available in four tiers — Plan A, Plan B, Plan B Lite, and Standard — it covers hospitalisation bills on an “as charged” basis, with annual claim limits ranging from $200,000 to $2,000,000. A key differentiator is built-in critical illness coverage of up to $100,000 per year and, for Plan A holders, the market-longest 13-month pre- and post-hospitalisation benefit.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

Table of Contents

Contents — Click to expand

- What Is AIA HealthShield Gold Max?

- The Four Plan Tiers Explained

- Premium Table by Age (2026)

- Plan A vs Plan B: Key Differences

- Critical Illness Coverage — A Hidden Gem

- AIA Max VitalHealth Riders & April 2026 Changes

- Paying Premiums with MediSave

- Who Should Buy AIA HealthShield Gold Max?

- Frequently Asked Questions

What Is AIA HealthShield Gold Max?

AIA HealthShield Gold Max is a MediSave-approved Integrated Shield Plan (ISP) offered by AIA Singapore. Like all ISPs in Singapore, it consists of two layers: the base MediShield Life coverage administered by the CPF Board, topped up with additional private insurance coverage from AIA. Together, they provide a more comprehensive hospitalisation safety net than MediShield Life alone.

The plan is available to Singapore Citizens, Singapore Permanent Residents, and foreigners holding valid work passes — making it one of the few ISPs with pass holder eligibility. Premiums can be fully or partially paid from your MediSave account, subject to the prevailing CPF Board withdrawal limits.

AIA HealthShield Gold Max is the flagship health product from AIA Singapore, and is positioned as a premium ISP with strong critical illness and outpatient benefits built in — factors that make it pricier than some competitors but richer in breadth of coverage.

The Four Plan Tiers Explained

AIA HealthShield Gold Max comes in four tiers, each targeting a different ward class and hospital type. Understanding which tier suits you depends on whether you prioritise private hospital access, value for money, or simply supplementing your MediShield Life coverage above what public hospitals offer.

| Plan | Ward Coverage | Annual Claim Limit | Pre/Post Hosp. | Annual Premium (Age 31–35, Male) |

|---|---|---|---|---|

| Plan A | Private Hospital | $2,000,000 | Up to 13 months | $360/yr |

| Plan B | Class A Ward (public/restructured) | $1,000,000 | Up to 180 days | $168/yr |

| Plan B Lite | Class B Wards & below | $300,000 | Up to 100 days | $102/yr |

| Standard Plan | Class B1 & below | $200,000 | None | $86/yr |

Source: AIA Singapore, Dollar Bureau (April 2026). Male Singapore citizen aged 31–35. Premiums subject to revision.

All plans share the same core structure: a $2,000 deductible applies before AIA pays out, and after the deductible, policyholders co-pay a minimum of 5% of the covered bill. This cost-sharing mechanism was introduced by MOH to encourage prudent use of healthcare — and it applies even if you hold a rider.

Premium Table by Age (2026)

AIA HealthShield Gold Max uses claims-based pricing, meaning if you make claims, your future premium increases above the standard age-band schedule. This is different from some competitors (e.g. HSBC Life Shield, Singlife Shield) that use flat premiums regardless of claims history.

The table below shows indicative base annual premiums for Plan A and Plan B for Singapore citizens. Note that premiums are not guaranteed and may be revised by AIA. The MediShield Life component is payable entirely from MediSave; the additional AIA component may require cash top-up in later age bands.

| Age Band | Plan A Total Premium | Plan A Cash Outlay (approx.) | Plan B Total Premium | Plan B Cash Outlay (approx.) |

|---|---|---|---|---|

| 1–20 | ~$210 | $0 (MediSave covers all) | ~$95 | $0 |

| 21–30 | ~$280 | $0–$50 | ~$130 | $0 |

| 31–40 | ~$360–$440 | $100–$200 | ~$168–$195 | $0–$30 |

| 41–50 | ~$560–$720 | $250–$400 | ~$240–$310 | $80–$150 |

| 51–60 | ~$1,000–$1,600 | $500–$900 | ~$420–$650 | $200–$400 |

| 61–70 | ~$2,200–$3,500 | $1,000–$2,000+ | ~$900–$1,400 | $500–$900 |

Source: AIA Singapore product summary (Sep 2024 version), CPF MediSave withdrawal limits. Figures indicative; cash outlay varies by MediSave balance and claims history. For exact premiums, refer to the AIA HealthShield Gold Max product page.

For younger policyholders aged 1 to 25, there is typically no cash outlay as MediSave covers the entire premium. The cash top-up requirement grows significantly from age 56 onwards, particularly for Plan A — a key consideration when budgeting for retirement healthcare costs. If you’re planning your retirement finances, our Singapore retirement calculator can help you model these future healthcare expenses.

Plan A vs Plan B: Key Differences

The choice between Plan A and Plan B is the most common dilemma for Singapore residents reviewing their health coverage. The headline difference is ward class — Plan A covers private hospitals while Plan B is capped at Class A wards in public or restructured hospitals — but the differences run deeper than that.

| Feature | Plan A | Plan B |

|---|---|---|

| Hospital Coverage | Private & Public A-class | Public/Restructured Class A only |

| Annual Claim Limit | $2,000,000 | $1,000,000 |

| Pre-Hospitalisation | Up to 13 months (AQHP/public) | Up to 180 days |

| Post-Hospitalisation | Up to 13 months (AQHP/public) | Up to 180 days |

| Critical Illness Cover | $100,000/year | $75,000/year |

| Deductible | $2,000 (private); $1,500–$3,500 (MOH min) | $2,000 (Class A) |

| Co-insurance | 5% after deductible | 5% after deductible |

| Annual Premium (age 31–35, Male) | $360 | $168 |

| Early Detection Screening | From age 40 (Plan A only) | Not included |

Source: AIA Singapore product summary, Dollar Bureau (April 2026).

From a pure cost-per-dollar-of-coverage standpoint, both plans are competitive within the market. For a 35-year-old male, Plan A costs $360/year for $2,000,000 in coverage — a cost-benefit ratio of approximately $5,556 of coverage per dollar of premium. Plan B offers $1,000,000 coverage for $168, a ratio of roughly $5,952. While Plan B has a slightly better ratio, Plan A’s 13-month pre/post hospitalisation benefit and the option to use Singapore’s private hospitals are significant qualitative advantages.

The 13-month pre/post hospitalisation benefit on Plan A is particularly valuable for managing serious conditions like cancer, where specialist consultations, imaging, and follow-up treatment extend well beyond 180 days. For those interested in building holistic financial protection alongside their health coverage, our guide on CPF investment strategy explains how to maximise your CPF funds for both healthcare and retirement.

Critical Illness Coverage — A Hidden Gem

One of the most underappreciated features of AIA HealthShield Gold Max is the built-in critical illness (CI) benefit. Most ISPs are purely hospitalisation plans; AIA’s plans include CI coverage on top of the hospitalisation layer at no extra premium charge.

Here is the CI coverage breakdown across plans:

| Plan | CI Benefit Per Year | CIs Covered |

|---|---|---|

| Plan A | $100,000/year | 30 late-stage CIs |

| Plan B | $75,000/year | 30 late-stage CIs |

| Plan B Lite | $50,000/year | 30 late-stage CIs |

| Standard | Not included | — |

Source: AIA Singapore HealthShield Gold Max product brochure (2026).

The 30 covered critical illnesses include major cancers, heart attacks, stroke, kidney failure, coronary artery bypass surgery, and Alzheimer’s disease, among others. This benefit pays out as a lump sum directly to the policyholder upon diagnosis, separate from the hospitalisation coverage. It can help offset income loss, home care costs, and other non-medical expenses during recovery.

Note that the CI benefit reduces your annual claim limit by the amount paid out. For example, a Plan B Lite policyholder who claims $50,000 in CI benefits will have their remaining annual limit reduced to $250,000 for that policy year. However, for Plan A and Plan B holders, the high claim limits mean this is unlikely to cause an issue in practice.

AIA Max VitalHealth Riders & the April 2026 MOH Changes

Riders are optional add-ons that cap your out-of-pocket costs above and beyond the base ISP. Before April 2026, the AIA Max VitalHealth riders could cover almost your entire deductible and co-insurance, leaving policyholders with near-zero bills even at private hospitals. This is no longer the case.

Effective 1 April 2026, MOH introduced sweeping changes to all IP riders to curb rising healthcare costs. Here is what changed:

| Feature | Old Riders (pre-Apr 2026) | New Riders (from Apr 2026) |

|---|---|---|

| Deductible Coverage | Rider covered deductible | NOT covered — you pay $1,500–$3,500 |

| Co-payment Cap | $3,000/year | $6,000/year (excl. deductible) |

| Min Co-payment | 5% | 5% (unchanged) |

| Rider Premium (approx. age 60) | ~$5,300/year | ~$3,700/year (−30%) |

| Transition Timeline | Existing policies unchanged until renewal after 1 Apr 2028 | New policies from 1 Apr 2026 must use new design |

Source: MOH press release, 26 November 2025. AIA Singapore April 2026 rider update infographics.

AIA has replaced the old AIA Max VitalHealth A and B with the new AIA Max VitalHealth Pro A and AIA Max VitalHealth Pro B, which comply with MOH’s April 2026 rules. The new riders are on average 30% cheaper — representing annual savings of roughly $600 for private hospital riders and $200 for public hospital riders. Older policyholders enjoy the greatest premium savings in absolute dollar terms.

The practical impact: if you are hospitalised at a private hospital under Plan A and incur a $56,900 bill (e.g. knee joint replacement), your out-of-pocket under the new rider is approximately $6,170 in MediSave — versus $2,840 under the old rider. However, if you switched to the new rider at age 60, you would have saved $1,600/year in premiums, meaning you recoup the extra co-payment after about three years of premium savings.

What this means for existing AIA Max VitalHealth holders: If you purchased your rider before 27 November 2025, you remain on the old design until your first renewal after 1 April 2028. You may wish to speak to your financial advisor about whether switching to the new, cheaper Pro rider makes sense for your situation, particularly if you are in good health and unlikely to require major hospitalisation in the near term.

Paying Premiums with MediSave

A significant advantage of AIA HealthShield Gold Max — like all ISPs — is the ability to pay premiums from your CPF MediSave account. This means the plan does not necessarily require cash outlay, especially for younger policyholders.

The MediSave portion covers the base MediShield Life premium in full. For the additional AIA component, MediSave can be used up to prevailing withdrawal limits (updated annually by the CPF Board). For younger insured persons aged 1–25, MediSave typically covers the entire premium with no cash outlay required.

Riders, however, must be paid entirely in cash — MediSave cannot be used for the AIA Max VitalHealth rider premium. This is an important distinction when budgeting for your health insurance costs, especially as you age into higher premium bands.

Singapore residents can also use their MediSave to pay the deductible and co-insurance under the ISP (subject to limits), which helps manage hospitalisation cash outlays. Understanding how your MediSave works alongside your ISP is an important part of your broader financial strategy in Singapore.

Who Should Buy AIA HealthShield Gold Max?

AIA HealthShield Gold Max is a strong option for a specific profile of Singapore residents. It is not the cheapest ISP on the market, but it offers a distinctive combination of features — particularly the CI coverage and long pre/post hospitalisation benefit — that certain buyers will find valuable.

AIA HealthShield Gold Max Plan A is ideal if you:

- Want access to private hospitals and private specialists without needing a referral

- Value the longest pre/post hospitalisation benefit in the market (13 months via AQHP)

- Want built-in critical illness coverage of $100,000/year alongside your hospitalisation plan

- Are aged 25–45 and can still buy at relatively low premiums with minimal cash outlay

- Have a family history of serious illness and want comprehensive protection

AIA HealthShield Gold Max Plan B is ideal if you:

- Are comfortable with public/restructured hospitals but want Class A ward access

- Want strong coverage at a materially lower premium than Plan A

- Want the $75,000/year CI benefit included in your hospitalisation plan

- Are looking to supplement MediShield Life without spending heavily on premiums

Consider alternatives if you:

- Want the cheapest possible ISP — NTUC Income Enhanced IncomeShield Advantage is materially cheaper for Plan B equivalents

- Prefer predictable, non-claims-based pricing — HSBC Life Shield and Singlife Shield use fixed premium schedules

- Only need B2/C ward coverage — other ISPs offer better value at the B Lite and Standard tiers

- Are looking for CPF-investable hospitalisation coverage — LSE ETFs and ISPs are separate instruments; ISPs are funded via MediSave, not CPF-OA

For a broader comparison of all seven ISPs in Singapore, our integrated shield plan comparison guide ranks every insurer across premiums, coverage, and post-2026 rider structures. You can also check out the MediShield Life guide to understand your base coverage before evaluating any top-up plan.

If you are in the process of reviewing your overall financial health in Singapore — insurance, savings, and investments — our Singapore retirement calculator and guide on Singapore Savings Bonds 2026 are useful starting points for the savings and investment side of the equation.

Frequently Asked Questions

What is AIA HealthShield Gold Max and how does it work?

AIA HealthShield Gold Max is a MediSave-approved Integrated Shield Plan (ISP) that layers on top of your MediShield Life base coverage. It covers hospitalisation bills mostly on an “as charged” basis — meaning AIA pays the actual bill after you cover the deductible ($2,000) and 5% co-insurance. Plans range from Standard (Class B1 and below, $200,000 limit) to Plan A (private hospitals, $2,000,000 limit). Premiums can be paid from MediSave, and the plan also includes critical illness coverage as a built-in benefit across Plans A, B, and B Lite.

What is the difference between AIA HealthShield Gold Max Plan A and Plan B?

The key difference is hospital coverage. Plan A covers private hospitals (and public hospitals), with an annual claim limit of $2,000,000 and up to 13 months of pre- and post-hospitalisation benefits. Plan B covers Class A wards in public or restructured hospitals, with a $1,000,000 limit and 180 days of pre/post cover. Plan A also includes $100,000/year in critical illness coverage versus $75,000/year for Plan B. For a 35-year-old male, Plan A costs $360/year and Plan B $168/year. The right choice depends on whether you want private hospital access and the extended hospitalisation benefit.

Can I buy AIA HealthShield Gold Max as a foreigner in Singapore?

Yes. AIA HealthShield Gold Max is one of the few integrated shield plans in Singapore that covers foreigners with valid work passes, in addition to Singapore Citizens and Permanent Residents. However, since MediShield Life only covers Singapore Citizens and PRs, work pass holders purchasing the plan will only get the AIA top-up portion — not the MediShield Life layer. Premiums for work pass holders are structured differently and must be confirmed directly with AIA or a licensed financial advisor.

What happened to AIA Max VitalHealth riders after April 2026?

From 1 April 2026, MOH introduced new rules requiring all IP riders to no longer cover the minimum IP deductible ($1,500–$3,500 depending on ward class). The co-payment cap was also raised from $3,000 to $6,000 per year. AIA responded by withdrawing the old AIA Max VitalHealth riders and launching the new AIA Max VitalHealth Pro A and Pro B, which comply with the new rules. The new riders are on average 30% cheaper in premiums. Existing policyholders who bought riders before 27 November 2025 remain on the old design until their first renewal after 1 April 2028.

Can I pay AIA HealthShield Gold Max premiums using MediSave?

Yes, all AIA HealthShield Gold Max base plan premiums can be paid from MediSave, subject to CPF Board withdrawal limits. For policyholders aged 1–25, MediSave typically covers the full premium with no cash outlay. Cash top-up becomes necessary from around age 26 onwards for Plan A, and from around age 31 for Plan B, as the AIA top-up component exceeds the MediSave withdrawal cap. Rider premiums (AIA Max VitalHealth Pro) must be paid entirely in cash — they cannot be funded from MediSave.

Is AIA HealthShield Gold Max worth buying over cheaper ISPs like NTUC Income?

It depends on your priorities. AIA’s plans are among the more expensive ISPs in Singapore, but they offer unique features: the market-longest 13-month pre/post hospitalisation benefit (Plan A), built-in critical illness coverage across all major tiers, and partnerships with AIA Quality Healthcare Partners (AQHP) for specialist referrals. Cheaper alternatives like NTUC Income Enhanced IncomeShield Advantage offer lower premiums but shorter hospitalisation benefit windows and no built-in CI. If predictable premiums matter most to you, HSBC Life Shield or Singlife Shield use non-claims-based pricing. The right ISP is the one that matches your health profile, budget, and hospital preference — getting a second opinion from a licensed financial advisor is always worthwhile.

Does AIA HealthShield Gold Max cover outpatient treatments and day surgery?

The base plans cover some outpatient treatments, particularly pre- and post-hospitalisation consultations, specialist referrals, and certain day surgeries. Plan A holders using AIA Quality Healthcare Partners (AQHP) enjoy the extended 13-month pre/post hospitalisation coverage for outpatient consultations directly related to a hospitalisation episode. GP teleconsultations via WhiteCoat are available from as low as $12 for AIA policyholders. For broader outpatient coverage beyond what the base plan provides, AIA also offers the Emergency and Outpatient Care Booster as an optional add-on for Plan A holders.

Review Your Full Financial Health Today

Health insurance is one piece of the puzzle. Pair it with strong savings and investment habits to build long-term financial resilience.

Get Free Insurance Advice

Speak with a licensed insurance advisor. No obligation, no cost.

By submitting this form, you agree to our Privacy Policy.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.