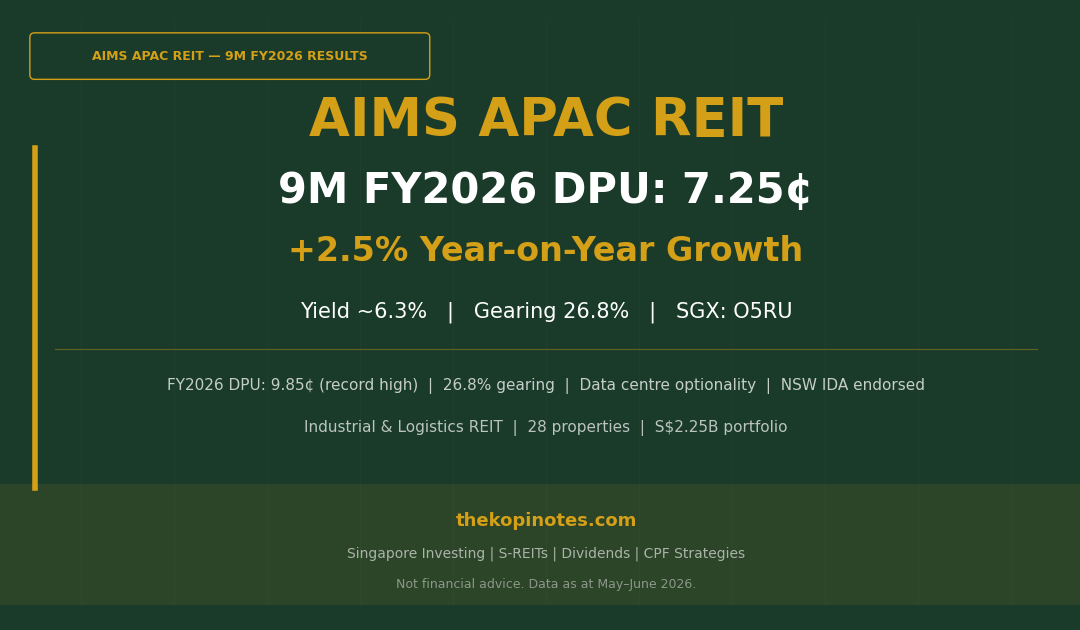

AIMS APAC REIT 9M FY2026 DPU: 7.25¢ Results, ~6.9% Yield & 2026 Investor Guide (SGX: O5RU)

SGX: O5RU | Industrial & Logistics REIT | Updated June 2026

AIMS APAC REIT (SGX: O5RU) reported 9M FY2026 DPU of 7.25 Singapore cents, up 2.5% year-on-year, driven by positive rental reversions across its 28-property Singapore and Australian industrial portfolio. Full-year FY2026 DPU reached 9.85¢ (+2.6% YoY), with aggregate leverage at just 26.8% — one of the lowest in the S-REIT sector. At a share price of S$1.57, trailing yield is approximately 6.3%, rising to ~6.9% on DRP-adjusted issue price. NSW government endorsement of two Australian assets for data centre development adds meaningful medium-term optionality.

Not financial advice. All figures are for educational reference only. Data as at May–June 2026 unless noted.

Table of Contents

Click to expand contents

- What Is AIMS APAC REIT (O5RU)?

- 9M FY2026 DPU: Key Results Breakdown

- FY2026 Full Year Financial Performance

- DPU History FY2019–FY2026

- Portfolio Overview: 28 Properties, S$2.25B

- Capital Management & Balance Sheet

- Data Centre Upside: NSW IDA Endorsement

- Peer Yield Comparison: AIMS vs Sector

- How to Buy AIMS APAC REIT (CPF / SRS / Cash)

- Verdict: Buy, Hold or Sell?

- FAQ

What Is AIMS APAC REIT (SGX: O5RU)?

AIMS APAC REIT (AA REIT) is a Singapore-listed industrial and logistics REIT managed by AIMS APAC REIT Management Limited, a subsidiary of AIMS Financial Group. The REIT owns a diversified portfolio of 28 industrial properties spread across Singapore (25 properties) and Australia (3 properties), with a combined portfolio value of S$2.25 billion as at 31 March 2026.

The portfolio spans multiple industrial sub-sectors: logistics & warehousing, hi-tech industrial, business parks, and light industrial. Major tenants include Woolworths, Optus, Illumina Singapore, KWE-Kintetsu World Express, and Schenker Singapore — representing a diversified, defensive tenant base with more than 80% of income from essential industries.

Listed on the Singapore Exchange (SGX) under ticker O5RU, AA REIT has delivered total returns of 720.42% since AIMS Financial Group’s takeover in 2009, outperforming the STI’s 403.93% over the same period.

| Key Metric | Value (as at Mar 2026) |

|---|---|

| SGX Ticker | O5RU |

| Share Price | S$1.57 |

| FY2026 DPU | 9.850 Singapore cents (+2.6% YoY) |

| Trailing Yield | ~6.3% at S$1.57 |

| DRP Yield | ~6.9% at DRP issue price S$1.42 |

| Aggregate Leverage | 26.8% |

| Portfolio Valuation | S$2.25 billion |

| No. of Properties | 28 (25 SG + 3 AU) |

| Committed Occupancy | 96.8% |

| WALE | 4.0 years |

| Analyst Target Price | S$1.65 (BUY) |

Source: AIMS APAC REIT FY2026 Annual Results, May 2026

9M FY2026 DPU: Key Results Breakdown

For the nine months ended 31 December 2025 (9M FY2026), AIMS APAC REIT reported DPU of 7.25 Singapore cents, representing a 2.5% increase year-on-year. This was supported by positive rental reversions, higher occupancy, and lower property operating expenses — specifically electricity costs.

Gross revenue for 9M FY2026 rose 1.4% year-on-year to S$141.1 million, while net property income (NPI) grew a stronger 4.1% to S$103.7 million. Distributions to unitholders reached S$59.3 million (+3.1% YoY).

| Period | DPU (¢) | YoY Change | Ex-Date / Payment |

|---|---|---|---|

| Q1 FY2026 (Apr–Jun 2025) | 2.35¢ | +1.7% | Sep 2025 |

| Q2 FY2026 (Jul–Sep 2025) | 2.37¢ | +2.2% | Dec 2025 |

| Q3 FY2026 (Oct–Dec 2025) | 2.53¢ | +3.3% | Mar 2026 |

| 9M FY2026 Subtotal | 7.25¢ | +2.5% | — |

| Q4 FY2026 (Jan–Mar 2026) | 2.60¢ | +4.0% | Jun 2026 |

| FY2026 Full Year Total | 9.850¢ | +2.6% | — |

Source: AIMS APAC REIT quarterly distribution announcements, FY2026

The Q4 distribution of 2.60¢ per unit was accompanied by the launch of a Distribution Reinvestment Plan (DRP), allowing unitholders to receive new units at approximately a 2.5% discount to market price. At the estimated issue price of S$1.42, the implied DRP yield works out to approximately 6.9% — materially above the 6.3% cash yield at S$1.57 market price.

FY2026 Full Year Financial Performance

AIMS APAC REIT’s FY2026 results (year ending 31 March 2026) delivered broad-based improvement. Gross revenue rose 2.2% year-on-year to S$190.7 million, while NPI grew a stronger 5.7% to S$141.3 million — expanding NPI margin to 74.1% from 71.7% in FY2025.

| Metric | FY2026 | FY2025 | YoY Change |

|---|---|---|---|

| Gross Revenue | S$190.7M | S$186.6M | +2.2% |

| Net Property Income | S$141.3M | S$133.7M | +5.7% |

| NPI Margin | 74.1% | 71.7% | +2.4 pts |

| Distributable Income | S$80.6M | S$78.2M | +3.1% |

| DPU | 9.850¢ | 9.600¢ | +2.6% |

| NAV per Unit | S$1.28 | S$1.23 | +4.1% |

| Portfolio Valuation | S$2.25B | S$2.13B | +5.9% |

| Aggregate Leverage | 26.8% | 28.9% | -2.1 pts |

| Interest Coverage Ratio | 2.7× | 2.5× | +0.2× |

| Rental Reversion | +7.7% | +20.0% | Normalised |

Source: AIMS APAC REIT FY2026 Annual Results Press Release, May 2026

A key highlight is the perpetual securities refinancing: AIMS APAC REIT issued S$150M at 4.10% p.a. (January 2026) and S$100M at 4.25% p.a. (March 2026), using proceeds to redeem S$250M of 5.375% perpetual securities due for reset in September 2026. This significantly reduces cost of capital and should support DPU stability through FY2027.

DPU History FY2019–FY2026: A Track Record of Growth

Despite a temporary dip in FY2024 following a S$100M equity fund raising (EFR), AIMS APAC REIT has delivered a broadly upward DPU trajectory. The FY2026 DPU of 9.85¢ is the highest in the REIT’s history.

| Financial Year | DPU (Singapore cents) | YoY Change |

|---|---|---|

| FY2019 (ended Mar 2019) | 9.60¢ | — |

| FY2020 (ended Mar 2020) | 9.05¢ | -5.7% (COVID impact) |

| FY2021 (ended Mar 2021) | 9.45¢ | +4.4% |

| FY2022 (ended Mar 2022) | 9.65¢ | +2.1% |

| FY2023 (ended Mar 2023) | 9.70¢ | +0.5% |

| FY2024 (ended Mar 2024) | 9.05¢ | -6.7% (EFR dilution) |

| FY2025 (ended Mar 2025) | 9.60¢ | +6.1% (recovery) |

| FY2026 (ended Mar 2026) | 9.850¢ | +2.6% (record high) |

Source: AIMS APAC REIT annual reports and quarterly distribution announcements, FY2019–FY2026

The FY2024 dip was deliberate: the Manager raised S$100M via EFR to fund acquisitions and reduce leverage. The enlarged unit base temporarily diluted DPU, but the REIT more than recovered in FY2025–FY2026. This short-term dilution for long-term balance sheet strength is a sign of disciplined capital management.

Portfolio Overview: 28 Properties, S$2.25 Billion

AIMS APAC REIT’s S$2.25B portfolio spans 25 Singapore properties and 3 Australian properties, with Singapore contributing approximately 76.5% of gross rental income and Australia 23.5%.

Key portfolio characteristics as at March 2026:

- Committed occupancy: 96.8% — substantially above JTC national average of 88.9%

- WALE: 4.0 years — over 50% of leases expiring beyond FY2030

- Rental reversion FY2026: +7.7% — Logistics & Warehouse +9.8%; Hi-Tech +11.7%

- 183 tenants, over 80% in essential/defensive industries

- 98.2% of single-user leases have built-in rent escalations of 2.0–3.25% p.a.

Recent portfolio activity included the acquisition of 2 Aljunied Avenue 1 (November 2025), AEI completions at 15 Tai Seng Drive and 7 Clementi Loop, and divestments at premium: 3 Toh Tuck Link sold at 32.5% above valuation, 8 Senoko South Road at 11.1% above valuation. For investors building a diversified S-REIT portfolio, AIMS APAC REIT’s industrial focus provides differentiated exposure with embedded data centre optionality.

Capital Management & Balance Sheet Strength

At 26.8% aggregate leverage, AIMS APAC REIT sits well below the MAS 50% regulatory limit and is among the lowest-geared S-REITs. This headroom provides significant capacity for debt-funded acquisitions without triggering equity fund raisings.

- Fixed-rate debt: 80% — up from 65% at December 2025

- Interest coverage ratio: 2.7×

- Weighted average debt maturity: 2.2 years — no maturities until FY2027

- AUD hedge: 69% of expected AUD distributable income on rolling 4-quarter basis

- Liquidity: S$263.4M in undrawn facilities plus bank balances

The perpetual securities refinancing — replacing S$250M of 5.375% perps with new 4.10% and 4.25% tranches — locks in approximately 90–115 basis points of annual savings on a quarter-billion in capital. For Singapore investors considering AIMS APAC REIT through Endowus or Syfe, the low gearing is a key risk mitigation factor in today’s higher-rate environment.

Data Centre Upside: NSW IDA Endorsement

The most significant medium-term catalyst is the NSW Government Investment Delivery Authority (IDA) endorsement of AIMS APAC REIT’s Macquarie Park and Bella Vista assets for data centre development (April 2026). The IDA assessed nearly A$92.6 billion in proposals and endorsed only 15 projects worth A$51.9 billion — AIMS APAC REIT’s two assets were among them, alongside sites owned by Microsoft, NEXTDC, Goodman, and Stockland.

The REIT’s strategy includes JV or co-development partnerships with institutional data centre operators, targeted acquisitions of land-rich assets near energy infrastructure, and capitalising on Australia’s Five Eyes security status driving sovereign data demand. Timeline to revenue contribution is likely 2–4 years per site, with execution risks. However, if even one site proceeds to conversion, the NAV uplift and rental step-up could be transformational — optionality not currently priced into the unit price at S$1.57.

Peer Yield Comparison: AIMS APAC REIT vs Singapore Industrial REITs 2026

| REIT | Ticker | Yield (approx.) | Gearing | Sub-Sector |

|---|---|---|---|---|

| AIMS APAC REIT | O5RU | ~6.3% | 26.8% | Industrial / Logistics |

| CapitaLand Ascendas REIT | A17U | ~6.1% | 39.0% | Diversified Industrial |

| Mapletree Industrial Trust | ME8U | ~6.5% | 34.0% | Industrial / Data Centres |

| Mapletree Logistics Trust | M44U | ~6.2% | 40.7% | Logistics |

| Frasers Logistics & Commercial | BUOU | ~6.0% | 32.5% | Logistics / Commercial |

| ESR-LOGOS REIT | J91U | ~7.0% | 37.2% | Industrial / Logistics |

| Sabana REIT | M1GU | ~7.5% | 28.0% | Industrial (SG-only) |

Source: Company reports, analyst estimates, June 2026. Approximate figures.

AIMS APAC REIT’s 26.8% gearing is comfortably the lowest among large industrial peers. At 40% leverage (still well below MAS limits), AIMS APAC REIT could add approximately S$600M+ in debt-funded acquisitions — meaningful pipeline optionality for FY2027 and beyond. Explore the Singapore REIT ETF guide for a fund-based approach to industrial REIT exposure, or read the full AIMS APAC REIT investor guide for deeper analysis. For a broader sector view, see the S-REIT sectors comparison.

How to Buy AIMS APAC REIT in Singapore (CPF / SRS / Cash)

AIMS APAC REIT (O5RU) is listed on the SGX and is CPFIS-OA eligible. The minimum purchase is 1 board lot = 100 units (~S$157 at current prices).

| Platform | Commission | CPF/SRS | Best For |

|---|---|---|---|

| FSMOne | 0.08%, min S$10 | CPF OA ✓, SRS ✓ | Cheapest CDP broker |

| Syfe Trade | 0.06%, min S$1.99 | Cash only | Low-cost cash trading |

| DBS Vickers | 0.18%, min S$18 | CPF OA ✓, SRS ✓ | DBS banking integration |

| IBKR | 0.05%, min S$2.50 | Cash only | Active traders, margin |

Source: Platform fee schedules, June 2026.

At ~6.3% trailing yield, O5RU offers approximately 380 basis points above the CPF OA rate of 2.5% — though investors accept market price risk. Use the S-REIT yield vs bond spread calculator to evaluate the current risk premium. For CPF OA purchases, FSMOne (code P0544985) offers the cheapest brokerage. Use the retirement planning calculator to model how O5RU distributions fit into your passive income goals.

Verdict: Buy, Hold or Sell? (June 2026)

Our assessment: BUY / ACCUMULATE on dips.

Bull case: FY2026 marks a new DPU high (9.85¢) with strong fundamentals — 96.8% committed occupancy, 26.8% leverage (lowest among large industrial peers), and a management team that has delivered 720% total returns since 2009. NSW IDA endorsement of Macquarie Park and Bella Vista for data centre development is not priced in. At S$1.57, analyst consensus target of S$1.65 implies ~5% capital upside plus ~6.3% income = ~11% total return potential.

Key risks: AUD/SGD FX (23.5% of GRI from Australia, 69% hedged); FY2027 refinancing (~S$275M due); data centre execution timeline (2–4 years); macro/manufacturing headwinds in Singapore.

Bottom line: For income-focused Singapore investors seeking industrial REIT exposure with low refinancing risk and data centre optionality, AIMS APAC REIT at current prices offers a compelling risk-adjusted entry. The DRP at S$1.42 (~6.9% yield) is particularly attractive for long-term compounders.

Start Investing in S-REITs Today

Use a referral code to get bonus credits when you sign up for a Singapore investment platform.

Frequently Asked Questions: AIMS APAC REIT 2026

What is AIMS APAC REIT's 9M FY2026 DPU?

What is the current dividend yield of AIMS APAC REIT?

How does AIMS APAC REIT's gearing compare to peers?

Is AIMS APAC REIT CPF-eligible?

What is the data centre opportunity for AIMS APAC REIT?

What are the main risks of investing in AIMS APAC REIT?

How do I buy AIMS APAC REIT in Singapore?

What is the Distribution Reinvestment Plan (DRP) and should I participate?

What is the analyst target price for AIMS APAC REIT?

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.