Gold ETFs in Singapore are investment funds that track the price of gold bullion, letting you invest in precious metals without storing physical gold. The most popular options for Singapore investors are the LionGlobal and Lion-OCBC physical gold ETFs listed on SGX, which offer low expense ratios (0.40–0.45% annually) and strong liquidity. They’re perfect for diversifying your portfolio into a defensive asset that historically performs well during economic uncertainty and currency volatility.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

- Gold ETFs give you precious metals exposure without physical storage hassles

- LionGlobal and Lion-OCBC gold ETFs have the lowest costs (0.40–0.45% per year) and best liquidity on SGX

- Gold works as a portfolio hedge—when stocks fall, gold often rises, especially during uncertainty and inflation spikes

What Are Gold ETFs? (And Why Singapore Investors Are Buying Them)

A gold ETF is a fund that holds physical gold bullion on your behalf and lets you buy or sell shares on the stock exchange. Think of it like owning a share of a vault full of gold.

Instead of worrying about storing a gold bar at home—or paying a bank safe deposit box fee—you simply buy units on the SGX like you would any stock. The fund manager manages the actual bullion. You get the upside of gold ownership without the logistics headache.

For Singapore investors, this matters because:

- Tax efficiency: SGX-listed gold ETFs are not subject to Goods and Services Tax (GST) on the gold holding itself, unlike buying physical coins or bars from dealers

- Liquidity: You can sell in seconds during market hours—try selling a gold bar in 30 seconds. It’s harder

- Low minimum: Start with as little as one unit (typically SGD 50–100). Physical gold bars usually cost SGD 5,000+ per gram

- CPF eligibility: Some gold ETFs are approved for CPF Investment Scheme (CPFIS) investment, letting you use your retirement savings to buy gold

The Best Gold ETFs You Can Buy on SGX Today

Singapore’s gold ETF landscape is small but solid. Here are the main options:

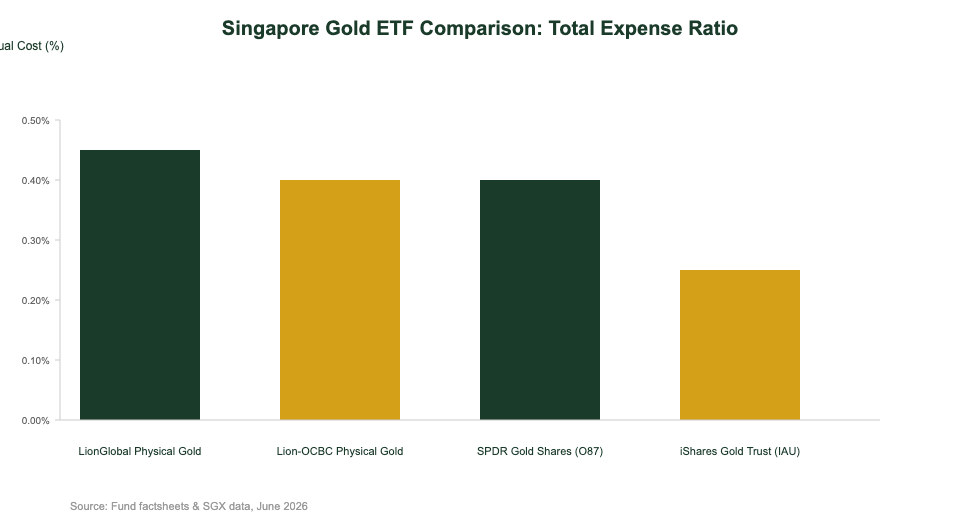

1. LionGlobal Singapore Physical Gold ETF (O89)

- Expense ratio: 0.45% per year

- Listing: SGX (main board)

- Underlying: Physical gold bullion, allocated on a 1:1 gram basis

- Minimum: Typically SGD 50–100 per unit

- Custody: Held by independent custodian

- Best for: SGX familiarity, straightforward allocation model

2. Lion-OCBC Singapore Physical Gold ETF (O78)

- Expense ratio: 0.40% per year (lowest cost option)

- Listing: SGX

- Underlying: Physical gold, same allocated structure

- Minimum: Similar, starting around SGD 50–100

- Custody: OCBC Bank custody

- Best for: Cost-conscious investors, long-term buy-and-hold portfolios

3. SPDR Gold Shares (O87)

- Expense ratio: 0.40% per year

- Listing: SGX (but LSE-listed; trades in SGD on SGX)

- Underlying: Physical gold bullion

- Minimum: SGD 50–100 per unit

- Best for: Investors wanting exposure to a globally-trusted brand (SPDR is State Street)

Why Expense Ratios Matter (And How They Quietly Eat Your Returns)

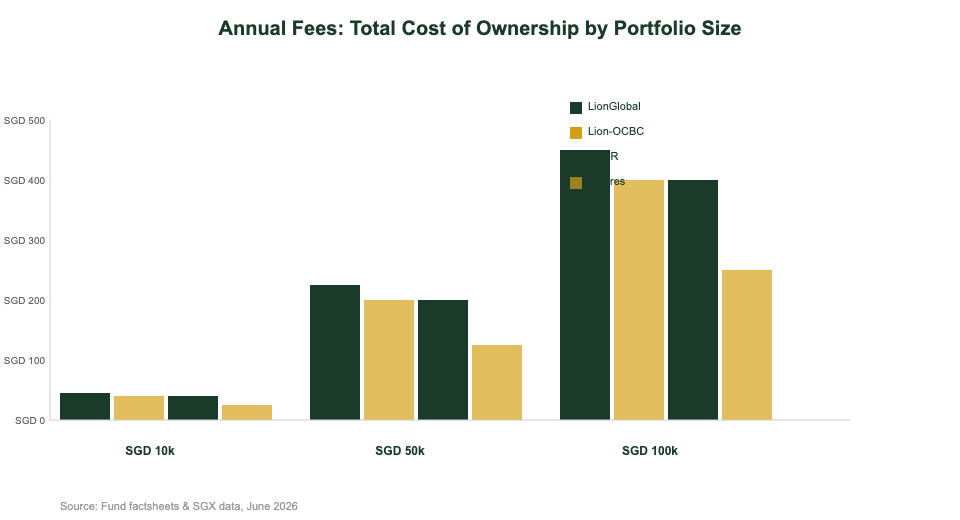

A 0.40% expense ratio sounds tiny. But over 20 years, it compounds.

Imagine you invest SGD 50,000 in a gold ETF with a 0.40% annual fee. That’s SGD 200 per year—or SGD 4,000 over 20 years, before accounting for the opportunity cost (what that money could have earned if invested elsewhere).

On a SGD 100,000 portfolio, that 0.40% fee becomes SGD 8,000 in lost returns over two decades.

The difference between 0.40% and 0.45% might seem negligible:

- SGD 10,000 portfolio: 0.05% difference = SGD 5 per year (seems nothing)

- SGD 100,000 portfolio: 0.05% difference = SGD 50 per year (still small)

- SGD 500,000 portfolio: 0.05% difference = SGD 250 per year (now it’s noticeable)

This is why choosing the Lion-OCBC or SPDR gold ETF (both at 0.40%) beats LionGlobal (0.45%) if you’re planning a large, long-term holding.

How to Buy Gold ETF in Singapore (Step-by-Step)

Step 1: Open a brokerage account

You’ll need a SGX trading account. Popular brokers in Singapore include:

- MooMoo—commission-free, popular with retail investors

- Syfe—robo-advisor with gold ETF options built-in (referral link: Syfe referral code)

- Interactive Brokers—lower fees if you trade frequently

- FSMOne or MariBank—local brokers with SGX access

Step 2: Fund your account

Most brokers accept bank transfers. Fund directly from your DBS, OCBC, or POSB account. Instant transfer typically takes 1–2 minutes.

Step 3: Search for the gold ETF ticker

On your broker’s platform, search for:

- O89 (LionGlobal Singapore Physical Gold ETF)

- O78 (Lion-OCBC Singapore Physical Gold ETF)

- O87 (SPDR Gold Shares)

Step 4: Place a buy order

Select your ETF, choose the number of units, and hit “Buy.” The order executes at the next trading opportunity (market hours: 9:00 AM–5:00 PM SGT, Monday–Friday).

Step 5: Hold and monitor

Gold ETF units appear in your portfolio immediately after settlement (usually T+1, next day). You can hold indefinitely—no expiry date, no forced selling.

Why Gold Matters in Your Portfolio (It’s Not Just a Hedge—It’s Insurance)

Most Singapore investors focus on stocks and bonds. But gold plays a unique role.

Gold rises when:

- Stock markets fall (negative correlation to equities)

- Inflation spikes (gold holds purchasing power)

- Currency weakens (SGD depreciation means gold becomes more expensive for foreign investors, but more valuable for SGD holders)

- Geopolitical uncertainty rises (capital flows into “safe haven” assets)

How much gold should you hold?

Financial advisors typically suggest 5–10% of your portfolio in precious metals. For a SGD 100,000 portfolio, that’s SGD 5,000–10,000 in gold ETFs.

But here’s the honest take: Gold doesn’t generate income. It doesn’t grow earnings. It fluctuates with sentiment and macro conditions.

You’re not holding gold to get rich. You’re holding it so your entire portfolio doesn’t collapse when stocks tank. It’s like insurance on your stock holdings.

Gold ETF vs. Physical Gold vs. Gold Mining Stocks: Which Is Right for You?

Physical Gold (coins or bars):

- ✓ Complete control—it’s in your hands

- ✓ No counterparty risk—you don’t depend on a fund manager

- ✗ High storage costs (bank safe box: SGD 50–200 per year)

- ✗ Harder to sell quickly (dealers have bid-ask spreads)

- ✗ Insurance costs

- ✗ Minimum viable purchase is expensive (SGD 5,000+ for a meaningful bar)

Gold ETFs (O78, O87, O89):

- ✓ Liquid—sell in 30 seconds during market hours

- ✓ Low cost (0.40–0.45% annually)

- ✓ Start with SGD 50–100

- ✓ Custodian handles security and insurance

- ✗ You depend on the fund manager’s integrity

- ✗ Slightly higher tracking error than physical (not perfect, but minimal)

Gold Mining Stocks:

- ✓ Potential for higher returns (earnings growth + gold price appreciation)

- ✗ Volatile—mining company profits swing wildly with metal prices AND operational efficiency

- ✗ Not pure gold exposure (you’re also betting on mining company management)

- ✗ Less reliable as a portfolio hedge

Bottom line: For most Singapore retail investors, gold ETFs (specifically O78 or O87) offer the best blend of low cost, liquidity, and simplicity.

Tax Implications for Gold ETF Investors in Singapore

Good news: Singapore has no capital gains tax. If you buy gold ETF at SGD 100 per unit and sell at SGD 120, that SGD 20 gain is 100% yours—no tax owed.

But watch out for:

- Withholding tax (dividend tax): If your gold ETF pays distributions (some do), foreign withholding tax might apply. SGX-listed physical gold ETFs are typically exempt, but check the fund factsheet

- Foreign withholding on overseas sales: If you sell overseas-listed gold ETFs (less common in Singapore), you might face capital gains tax abroad

- GST exemption: SGX-listed gold ETFs are exempt from GST. Physical gold from dealers is NOT exempt (10% GST on purchase price)

Action step: Download the fund factsheet for your chosen gold ETF (O78, O87, or O89) and check the “Tax Considerations” section. It’s 2–3 pages and critical to understand before investing.

Key Risks: What Can Go Wrong?

Gold price volatility: Gold swings 10–20% in a year. In 2023, it rose 13%. In 2022, it fell 6%. If you need the money in 6 months, you might catch a downturn.

Counterparty risk: You’re trusting the custodian (usually a major bank) to actually hold the gold. This is extremely low risk for established funds like SPDR or Lion-OCBC, but it exists.

Tracking error: ETF fees and fund operations mean the ETF return might lag the spot gold price by 0.40–0.50% annually. This is expected and already factored into the expense ratio.

Currency risk: Gold is priced globally in USD. If SGD strengthens against the USD, your gold returns take a hit in SGD terms (and vice versa). This cuts both ways—a weaker SGD boosts your returns.

Liquidity risk (minimal): O78, O87, and O89 are highly liquid on SGX. But during extreme market stress, even major ETFs can see wider bid-ask spreads. Unlikely, but possible.

Quick Comparison: Which Gold ETF Should You Buy?

| Metric | LionGlobal (O89) | Lion-OCBC (O78) | SPDR (O87) |

|---|---|---|---|

| Expense Ratio | 0.45% | 0.40% | 0.40% |

| Listing | SGX | SGX | SGX |

| Underlying Asset | Physical gold | Physical gold | Physical gold |

| Custody | Independent | OCBC Bank | State Street |

| Liquidity | High | High | Very High |

| Best For | Local familiarity | Cost-conscious, long-term | Global brand trust |

Source: Fund factsheets and SGX data, June 2026

Building a Diversified Portfolio With Gold ETFs

Here’s how a typical 40-year-old Singapore investor might structure a portfolio using gold ETFs:

- 60% Global equities (VWRA or CSPX ETFs): SGD 60,000 — broad diversification, long-term growth engine

- 15% S-REIT ETFs: SGD 15,000 — local income yield (4–5% distributions), inflation hedge

- 10% Singapore bonds or T-bills: SGD 10,000 — capital preservation, lower volatility

- 10% Gold ETF (O78 or O87): SGD 10,000 — portfolio insurance, currency hedge, inflation protection

- 5% Cash: SGD 5,000 — emergency buffer, rebalancing flexibility

This mix is designed to weather different economic scenarios:

- Stock market crash? Bonds and gold cushion the fall (they often rise when stocks tank)

- Inflation spike? S-REITs and gold maintain purchasing power

- Currency weakness? Gold and global equities appreciate in SGD terms

Rebalance annually. If gold has grown to 15% of your portfolio (because prices rose), trim it back to 10% and redeploy to other assets. This forces you to “buy low, sell high” automatically.

5 Common Gold ETF Mistakes (And How to Avoid Them)

1. Buying gold at the absolute peak of hype (2011, 2020)

Gold spikes on fear. When gold is making headlines in the news, it’s often already expensive. Dollar-cost average instead: invest SGD 500 every month, regardless of price. You’ll catch both highs and lows.

2. Holding too much gold (20%+ of portfolio)

Gold doesn’t grow. Stocks do. A 20% gold allocation in a 40-year-old’s portfolio is excessive. You’re sacrificing long-term compound returns for a hedge you may not need. Stick to 5–10%.

3. Forgetting to rebalance

If gold doubles in value, your allocation drifts from 10% to 20%. Now you’re overexposed. Rebalance every 12 months. Sell high (gold), buy low (stocks or bonds that lagged).

4. Choosing the wrong broker and overpaying on fees

Some brokers charge SGD 12.50 per SGX trade. Others charge SGD 0. If you’re investing in small amounts (e.g., SGD 500 per month), high commissions kill returns. Use commission-free brokers like MooMoo or Syfe.

5. Panic-selling during crashes

Gold fell 30% in 2013, yet it rebounded and hit all-time highs by 2024. If you sell during dips, you crystallize losses. Gold is a long-term holding. Stay disciplined.

Table of Contents

Can I hold gold ETF in my CPF account?

Yes, but only specific gold ETFs are CPFIS-approved. Check with the CPF Board’s approved investment list. Not all SGX gold ETFs are CPFIS-eligible—verify before buying. If approved, you can use your CPF-IS funds to invest, which is tax-advantaged.

What's the minimum investment amount for a gold ETF?

One unit. Gold ETF unit prices typically range from SGD 50–100, so your minimum is effectively SGD 50–100 to buy just one unit. After that, you can buy fractions (if your broker supports it) or additional whole units. Some brokers allow buy-and-hold with as little as SGD 100 per order.

Do gold ETFs pay dividends or distributions?

Physical gold ETFs (O78, O87, O89) rarely pay distributions because they don’t generate income—they just hold gold. However, some funds may have minor distributions from interest earned on cash reserves. Check the fund factsheet. If there are distributions, they’re typically tiny (under 0.2% yield).

Should I buy gold now or wait for a dip?

Time in the market beats timing the market. Nobody can predict gold’s next move. Instead of guessing, use dollar-cost averaging: invest SGD 500–1000 every month, regardless of price. Over 10 years, this smooths out volatility and eliminates the regret of waiting for a dip that never comes (or buying a peak).

Can gold ETFs go to zero?

Extremely unlikely. Gold has been money for 5,000 years. Physical gold has intrinsic value. Unlike stocks (which depend on company profitability), gold’s value is underpinned by physical scarcity and global demand. A gold ETF collapse would require complete loss of confidence in gold itself, which is not a realistic scenario.

Is it better to buy gold ETFs or gold bonds (e.g., Savings Bonds)?

Different tools for different goals. Gold ETFs track the gold price directly. Singapore Savings Bonds (where available) offer fixed interest + capital protection. If you want pure gold exposure and liquidity, use ETFs. If you want guaranteed interest with a safety floor, use bonds. Many investors hold both.

What happens if the gold custodian (e.g., OCBC) goes bankrupt?

Your gold is held separately from the fund manager’s or custodian’s own assets. This is called “segregated custody.” Even if OCBC or the fund manager failed, your gold is protected because it’s legally ring-fenced. This is standard practice for all major ETFs and is overseen by regulators. The risk is minimal.

How do I sell my gold ETF?

Same way you sell any SGX stock. Log into your broker’s platform during market hours (9 AM–5 PM SGT, Mon–Fri), select your gold ETF position, enter the number of units, and click “Sell.” The order executes at the next trading opportunity. Settlement is T+2 (2 business days), and cash lands in your account.

Are there any hidden fees I should know about?

The main fee is the expense ratio (0.40–0.45%). Your broker may charge a small commission per trade (SGD 0–20, depending on the broker). There’s no hidden fee specific to gold ETFs. Always check your broker’s fee schedule before buying. If you trade frequently, a commission-free broker saves you thousands annually.

Can I use gold ETFs as collateral for a loan?

Some brokers allow margin lending against ETF collateral. This means you can borrow money using your gold ETF holdings as collateral to buy more investments. Interest rates typically start at 3–5% annually. It’s advanced and risky—use only if you understand leverage. Most beginner investors should avoid this.

The Bottom Line: Should You Invest in Gold ETFs?

Gold ETFs are the easiest, cheapest way for Singapore investors to own precious metals. Unlike physical gold, you don’t deal with storage or logistics. Unlike gold futures, you don’t need advanced trading skills. You simply buy and hold.

Start with O78 (Lion-OCBC) or O87 (SPDR) if:

- You want the lowest cost (0.40% annually)

- You plan to hold for 10+ years

- You want a portfolio hedge against stock crashes and inflation

- You have SGD 5,000+ to invest upfront (amount matters less with long timelines)

Skip gold ETFs if:

- You need the money within 3 years (too volatile)

- You want income-generating assets (gold doesn’t pay dividends)

- You want growth at any cost (stocks outpace gold over decades)

- You already hold 15%+ precious metals (overweight to risk)

The best investment is the one you’ll stick with. Gold ETFs are boring, defensive holdings that do exactly what you expect: preserve wealth when everything else is falling. That’s their job. Do it well.

Ready to start? Open a brokerage account (recommend Syfe or MooMoo), fund it, search for O78 or O87, and buy your first units. No complexity. No regrets.

Not financial advice. Consult a licensed financial advisor before making investment decisions. All figures are educational reference only. Data as at June 2026.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.