Best USD Fixed Deposit Rates in Singapore (2026 Guide)

GXS, MariBank, Trust Bank, DBS & more — compared for your USD savings

USD fixed deposits in Singapore pay between 2.40% and 3.50% per year in 2026, depending on which bank you choose and your deposit tenure. Digital banks like GXS and MariBank currently offer the highest rates — up to 3.50% p.a. for USD deposits — while traditional banks like DBS and OCBC sit around 2.50%–2.60%. This guide compares the top options so you can earn more on your spare US dollars.

Not financial advice. All figures are for educational reference only. Rates are indicative as at June 2026 — always verify with the bank before opening a deposit.

- Digital banks (GXS, MariBank) pay the best USD FD rates — up to 3.50% p.a. as at June 2026

- Traditional banks pay less but offer longer tenures and higher deposit limits

- On USD 20,000 for 1 year, you earn ~$700 with GXS vs ~$520 with DBS — a $180 difference

📋 Table of Contents

- What Is a USD Fixed Deposit?

- Best USD Fixed Deposit Rates in Singapore 2026

- Digital Banks: GXS and MariBank USD Rates

- Traditional Banks: DBS, OCBC, UOB, Citibank

- How to Open a USD Fixed Deposit in Singapore

- USD FD vs SGD Fixed Deposit: Which Is Better?

- Tips to Maximise Your USD Deposit Returns

- Frequently Asked Questions

What Is a USD Fixed Deposit?

A USD fixed deposit (FD) is a savings product where you lock in a lump sum of US dollars with a bank for a fixed period — typically 1 month to 12 months — and earn a guaranteed interest rate. At the end of the tenure, you get your principal back plus the interest earned.

Unlike a regular USD savings account, a fixed deposit locks your money away. You generally cannot withdraw early without a penalty (or forfeiting interest). In exchange, banks offer a higher rate than a standard savings account.

Singapore banks offer USD FDs because many Singaporeans and permanent residents hold US dollars — whether from overseas income, investments, or travel. It is a simple way to put idle USD to work while you decide what to do with it long-term.

Best USD Fixed Deposit Rates in Singapore 2026

Here is a side-by-side comparison of the top USD fixed deposit rates available to retail customers in Singapore as at June 2026. We have focused on 3-month and 12-month tenures as these are the most commonly offered.

| Bank | 3-Month Rate | 12-Month Rate | Min. Deposit | Type |

|---|---|---|---|---|

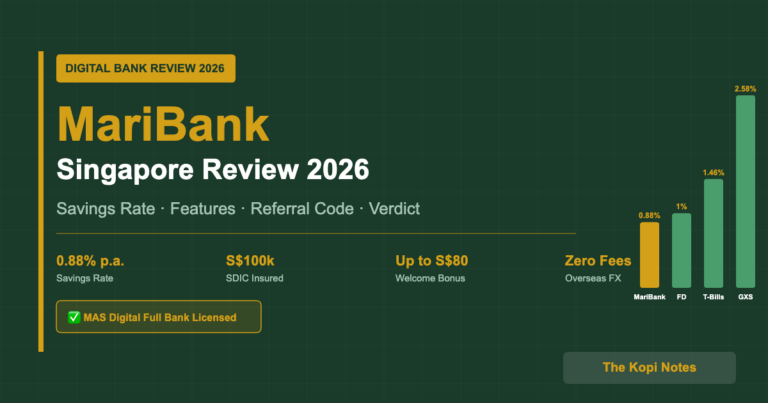

| GXS Bank | 3.50% | 3.20% | USD 500 | Digital |

| MariBank | 3.20% | 3.00% | USD 500 | Digital |

| Trust Bank | 2.80% | 2.70% | USD 1,000 | Digital |

| DBS Bank | 2.60% | 2.55% | USD 5,000 | Traditional |

| OCBC | 2.50% | 2.45% | USD 5,000 | Traditional |

| UOB | 2.40% | 2.35% | USD 5,000 | Traditional |

Source: Individual bank websites and app listings, June 2026. Rates are indicative and subject to change — always verify directly with the bank before opening a deposit.

Digital Banks: GXS and MariBank USD Rates

Singapore’s digital banks have shaken up the fixed deposit market. Without the overhead of physical branches, they can afford to pass higher rates to you. Here is what you need to know about each.

GXS Bank USD Fixed Deposit

GXS Bank — backed by Grab and Singtel — currently offers the highest USD FD rate in Singapore at 3.50% p.a. for a 3-month tenure. The minimum deposit is just USD 500, making it accessible even if you only have a small amount of US dollars sitting idle.

You can open a GXS USD FD entirely within the GXS app in a few minutes. There is no paperwork and no branch visit required. If you are not yet a GXS customer, you can sign up with referral code YONG477 to get a welcome bonus.

One thing to note: GXS USD FDs are covered by the Singapore Deposit Insurance Corporation (SDIC) up to SGD 100,000 in aggregate across all your deposits at GXS. This is the same protection you get at DBS or OCBC.

MariBank USD Fixed Deposit

MariBank — Sea Group’s digital bank — offers 3.20% p.a. on USD deposits for a 3-month tenure, with a minimum of USD 500. MariBank is tightly integrated with Shopee Pay and SeaMoney, so if you are already in that ecosystem it is a natural fit.

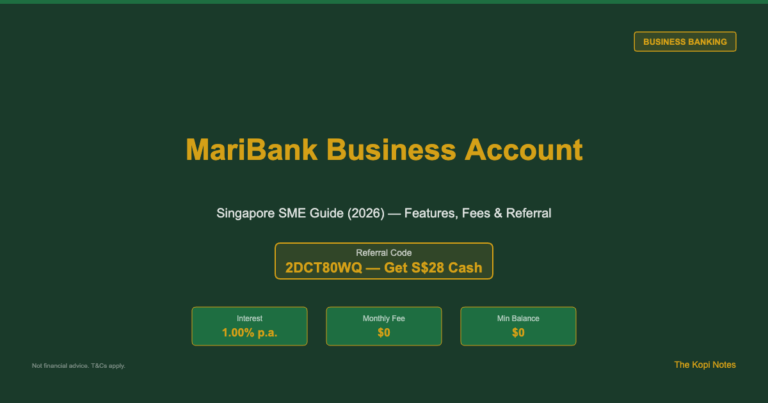

MariBank has been popular for its MariBank review and straightforward app experience. If you want to open a MariBank account, use referral code 2DCT80WQ when signing up.

Both GXS and MariBank are fully licensed digital full banks regulated by MAS — they are not fintech wallets. Your deposits are safe and SDIC-protected.

Traditional Banks: DBS, OCBC, UOB, Citibank

Traditional banks offer lower USD FD rates than digital banks, but they do have some advantages. Higher deposit limits (some banks accept USD 500,000+), longer tenures (up to 24 months), and the comfort of an established institution can matter for larger sums.

DBS USD Fixed Deposit

DBS offers around 2.60% p.a. for a 3-month USD FD, with a minimum deposit of USD 5,000. You can place it online via DBS iBanking or the digibank app. DBS also has a GXS Bank review comparison piece if you want to weigh the options.

OCBC USD Fixed Deposit

OCBC is at 2.50% p.a. for 3 months, also requiring a minimum of USD 5,000. One advantage of OCBC is that existing 360 account holders can sometimes access promotional rates — check the OCBC website or app for current promos before placing your deposit.

Citibank USD Fixed Deposit

Citibank Singapore offers competitive USD rates for Citigold and Citi Priority customers. If you already have a Citibank relationship and maintain a higher balance, you may qualify for preferential rates not listed publicly. Call or log in to check your personalised rate.

How to Open a USD Fixed Deposit in Singapore

Opening a USD FD in Singapore is straightforward. Here is the general process across most banks:

- Have a USD account or fund one first. Most banks require you to have a USD current or savings account before placing a FD. You can fund it by exchanging SGD to USD via your banking app (usually at competitive FX rates).

- Choose your bank and tenure. Decide based on the rate comparison table above. Shorter tenures (1–3 months) let you reinvest at higher rates if they move up. Longer tenures lock in the current rate.

- Apply via the app or online banking. For digital banks (GXS, MariBank, Trust), the entire process is in-app and takes under 5 minutes. For traditional banks, log in to iBanking or visit a branch.

- Confirm and wait for maturity. You will receive a confirmation with the exact interest amount. At maturity, principal + interest is credited back to your account automatically.

One practical tip: if you are converting SGD to USD, compare the FX rate offered by the bank against apps like Wise or YouTrip. Sometimes the spread is significant — especially at traditional banks. A bad FX rate can eat into your FD gains.

For low-risk alternatives to USD FDs, you might also consider Singapore T-bills 2026 guide or Singapore Savings Bonds guide for SGD savings options.

USD FD vs SGD Fixed Deposit: Which Is Better?

This is a common question. The short answer: it depends on what currency you actually need.

| Factor | USD FD | SGD FD |

|---|---|---|

| Typical best rate (2026) | ~3.50% p.a. | ~2.80–3.20% p.a. |

| FX risk | Yes — USD/SGD moves against you | None |

| Best for | Existing USD holdings | SGD savings & local spending |

| SDIC coverage | Yes (SGD equivalent up to S$100k) | Yes (up to S$100k) |

| Withholding tax for SG residents | None | None |

Source: The Kopi Notes comparison, June 2026.

The key risk with USD FDs is currency movement. If the USD weakens against the SGD during your deposit tenure, your SGD returns are lower than the headline rate suggests. For example, if you earn 3.50% in USD but the USD falls 2% against the SGD, your effective SGD return is only about 1.5%.

This is why USD FDs make most sense if you already have US dollars you need to park — from selling US stocks, receiving overseas income, or holding USD for a future purchase. Converting SGD to USD specifically to chase a higher FD rate is riskier than it looks.

Tips to Maximise Your USD Deposit Returns

A few practical ways to get more out of your USD deposits:

1. Ladder your deposits. Instead of locking everything into one 12-month FD, split it across 3-month, 6-month, and 12-month deposits. This way, part of your money comes due every quarter and you can reinvest at whatever rate is available then.

2. Use digital banks for smaller amounts. GXS and MariBank have USD 500 minimums vs USD 5,000 for traditional banks. If you have a smaller USD sum, digital banks are your best option for competitive rates.

3. Check for promotional rates. Banks sometimes run short promotional FD rates that beat their standard rates. The best way to catch these is to follow each bank’s app notifications or check financial community groups on Telegram and Reddit Singapore.

4. Watch the USD/SGD rate before locking in. If the SGD has recently strengthened significantly (meaning your USD is now worth more SGD), it might be a good time to convert some USD to SGD instead of placing a FD — then park that SGD in a Singapore Savings Bond or T-bill.

5. Don’t forget SDIC limits. Your USD deposits are insured by SDIC up to SGD 100,000 in aggregate per bank. If you have large USD holdings, spread them across more than one bank to stay within the SDIC protection limit at each.

For broader passive income strategies, see our guide on passive income Singapore 2026 — it covers FDs alongside T-bills, bonds, REITs, and ETFs so you can see where each fits in your overall portfolio.

Frequently Asked Questions

What is the best USD fixed deposit rate in Singapore right now?

Are USD fixed deposits in Singapore safe?

Is there withholding tax on USD FD interest in Singapore?

Can I withdraw a USD FD early?

What is the minimum amount for a USD fixed deposit in Singapore?

Should I convert SGD to USD to get a higher FD rate?

How does GXS Bank compare to DBS for USD fixed deposits?

The Bottom Line

If you have US dollars sitting idle in a savings account earning near zero, a USD fixed deposit is one of the easiest wins in personal finance right now. Digital banks — particularly GXS and MariBank — have made it more accessible than ever with low minimums and fully in-app onboarding.

For most Singaporeans with USD holdings under USD 50,000, GXS Bank is our pick for the best rate (3.50% p.a. as at June 2026) combined with low minimums and SDIC protection. If you prefer to keep everything under one roof at a traditional bank, DBS offers the most seamless experience even if the rate is lower.

Remember: only park USD you genuinely have — do not convert SGD to USD just to chase the rate. The FX risk can easily outweigh the interest advantage.

Looking to put your SGD savings to work too? Check out our Singapore retirement calculator to see how these deposits fit into your bigger financial picture, or explore our passive income Singapore 2026 guide for a complete overview of your options.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial advice. Interest rates change frequently — verify all figures directly with the respective bank before making any financial decision. The Kopi Notes may earn a referral fee if you sign up using referral codes on this page.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.