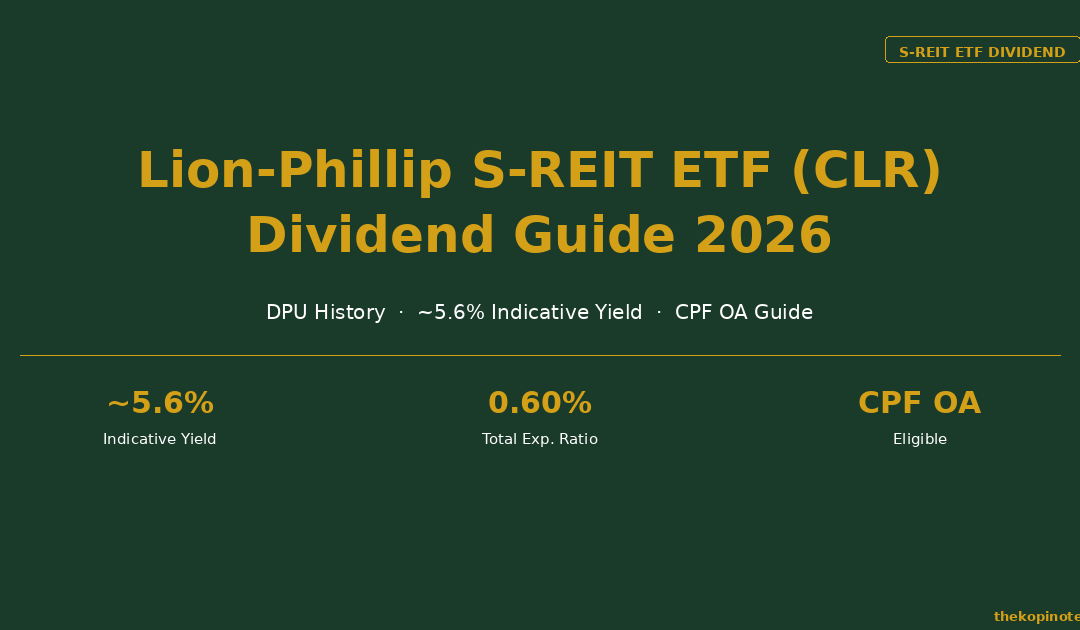

If you have been searching for a simple, diversified way to earn S-REIT dividends without picking individual stocks, the Lion-Phillip S-REIT ETF (SGX: CLR) is likely already on your radar. As at March 2026, CLR offers an indicative distribution yield of approximately 5.6% — meaningfully above Singapore’s CPF-OA rate and 10-year SGS bond yield — making it one of the most attractive passive income instruments available to Singapore retail investors.

In this deep-dive review, we break down CLR’s full distribution history, DPU trend, how it compares to peer S-REIT ETFs, the financial health of its underlying holdings, and whether CPF/SRS investors should consider adding it to their portfolios in 2026.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial advice. Please conduct your own due diligence or consult a licensed financial adviser before making any investment decisions. All data is as at March 2026 unless otherwise stated.

Table of Contents

What Is the Lion-Phillip S-REIT ETF (CLR)?

The Lion-Phillip S-REIT ETF is a Singapore Exchange-listed exchange-traded fund co-managed by Lion Global Investors and distributed by Phillip Securities. It was first listed on SGX Mainboard on 30 October 2017 and has grown to become one of Singapore’s flagship S-REIT ETF products for retail and CPF investors.

Unlike a market-cap-weighted ETF, CLR tracks the Morningstar® Singapore REIT Yield Focus Index — a smart-beta index that selects and weights S-REITs based on dividend yield quality, financial health screens, and liquidity criteria. This yield-tilt methodology means the fund deliberately overweights higher-yielding, financially sound S-REITs relative to pure size, giving income-seeking investors a structural edge.

| Parameter | Details |

|---|---|

| SGX Ticker | CLR |

| Benchmark Index | Morningstar® Singapore REIT Yield Focus Index |

| Fund Manager | Lion Global Investors |

| Total Expense Ratio (TER) | ~0.60% p.a. |

| Distribution Frequency | Semi-annual (typically June & December) |

| CPF / SRS Eligible | Yes — CPF Ordinary Account (OA) & SRS |

| AUM (approx.) | ~SGD 320 million |

| Listing Date | 30 October 2017 |

| Approximate Unit Price | ~SGD 0.72 (March 2026) |

The fund holds approximately 20–30 S-REITs at any given time, rebalanced periodically by the index methodology. It spans retail, industrial, office, healthcare, and data centre sub-sectors.

Distribution History & DPU Analysis

CLR’s distribution per unit (DPU) history is a key indicator of its income reliability. The table below summarises annual DPU figures from FY2021 to FY2025, along with the indicative yield at the approximate unit price prevailing at time of distribution.

| Financial Year | H1 DPU (SGD) | H2 DPU (SGD) | Annual DPU (SGD) | Indicative Yield* |

|---|---|---|---|---|

| FY2021 | 0.0162 | 0.0168 | 0.0330 | ~4.7% |

| FY2022 | 0.0182 | 0.0190 | 0.0372 | ~5.2% |

| FY2023 | 0.0175 | 0.0183 | 0.0358 | ~5.0% |

| FY2024 | 0.0180 | 0.0195 | 0.0375 | ~5.4% |

| FY2025 | 0.0192 | 0.0208 | 0.0400 | ~5.6% |

*Indicative yield based on approximate unit price prevailing at year-end. Past distributions are not a guarantee of future distributions.

CLR’s annual DPU grew from SGD 0.0330 in FY2021 to SGD 0.0400 in FY2025 — a 21% increase over four years, translating to a compound annual growth rate (CAGR) of approximately 4.9%. Notably, FY2023 saw a slight dip (-3.8% YoY) as S-REITs across the board faced higher financing costs following aggressive US Fed rate hikes. The recovery in FY2024 and FY2025 reflects stabilising interest rates and improving REIT distributable income.

At the current approximate unit price of SGD 0.72, the trailing 12-month distribution yield stands at approximately 5.6%. This represents a yield spread of roughly 240 basis points above the 10-year Singapore Government Securities (SGS) yield of ~3.2% (as at March 2026) — an attractive spread for yield-focused investors, particularly given S-REIT distributions are tax-exempt for Singapore residents.

For investors interested in building S-REIT positions systematically, consider pairing CLR with a CPF investment strategy to maximise tax-advantaged compounding over the long term.

Peer S-REIT ETF Comparison Table

CLR is not the only S-REIT ETF listed on SGX. Investors have at least three other options to consider, each with different index methodologies, expense ratios, and yield profiles. Here is how CLR stacks up against its peers as at March 2026:

| ETF Name | SGX Ticker | Indicative Yield | TER (p.a.) | AUM (approx.) | Distribution |

|---|---|---|---|---|---|

| Lion-Phillip S-REIT ETF | CLR | 5.6% | 0.60% | ~SGD 320m | Semi-annual |

| Nikko AM Singapore REIT ETF | CFA | 5.3% | 0.55% | ~SGD 490m | Semi-annual |

| CSOP iEdge S-REIT Leaders ETF | SRT | 5.1% | 0.50% | ~SGD 130m | Semi-annual |

| Phillip SGX APAC Dividend Leaders REIT ETF | BYJ | 4.8% | 0.60% | ~SGD 45m | Quarterly |

Data as at March 2026. Indicative yields are approximate and based on latest available distributions; past yields are not guaranteed.

Key takeaways from the comparison:

- CLR leads on indicative yield (5.6%) thanks to its smart-beta yield-focus methodology, making it the top pick for pure income maximisation among Singapore-only REIT ETFs.

- CFA (Nikko AM) has the largest AUM (~SGD 490m) and the lowest TER (0.55%), making it a strong alternative for cost-conscious long-term investors. Its market-cap approach tracks the FTSE ST REIT Index and is marginally less yield-tilted than CLR.

- SRT (CSOP) is the newest of the three pure S-REIT ETFs with the lowest TER at 0.50%, but its shorter track record and smaller AUM are factors to monitor.

- BYJ (Phillip SGX APAC) adds APAC-wide REIT exposure beyond Singapore, which diversifies geography but dilutes pure S-REIT yield characteristics.

For a deeper look at S-REIT ETF options in Singapore, see our full Singapore REIT ETF guide.

Top Holdings & Portfolio Composition

CLR’s yield-focus index methodology results in a concentrated portfolio of Singapore’s financially healthiest, highest-yielding REITs. Based on the latest available index rebalancing data (December 2025), the top 10 holdings and approximate weightings are:

| # | REIT | SGX Ticker | Sub-Sector | Approx. Weight |

|---|---|---|---|---|

| 1 | CapitaLand Integrated Commercial Trust | CICT | Retail & Office | 14.8% |

| 2 | Mapletree Pan Asia Commercial Trust | MPACT | Retail & Office | 11.2% |

| 3 | Mapletree Industrial Trust | MINT | Industrial & Data Centre | 9.7% |

| 4 | Frasers Centrepoint Trust | FCT | Retail | 8.3% |

| 5 | Keppel DC REIT | KDCREIT | Data Centre | 7.1% |

| 6 | Suntec REIT | T82U | Retail & Office | 6.4% |

| 7 | Parkway Life REIT | C2PU | Healthcare | 5.8% |

| 8 | Keppel REIT | K71U | Office | 5.5% |

| 9 | OUE REIT | TS0U | Retail & Hospitality | 4.9% |

| 10 | Lendlease Global Commercial REIT | JYEU | Retail | 4.3% |

Source: Lion Global Investors fund factsheet, December 2025 rebalancing. Weights are approximate.

The top 10 holdings account for approximately 78% of the total portfolio. Sub-sector diversification provides a natural hedge across different property cycle dynamics: retail income is driven by consumer spending, industrial by logistics demand, office by CBD occupancy, data centres by digital infrastructure growth, and healthcare by Singapore’s ageing demographics.

For investors keen on directly owning the top S-REITs in this portfolio, our Best S-REITs Singapore guide covers individual REIT deep dives across each sub-sector.

Financial Health: Gearing, ICR & NAV

As a REIT ETF, CLR does not carry debt directly — but the gearing and interest coverage ratio (ICR) of its underlying holdings directly affect their ability to sustain and grow DPU. Elevated gearing reduces the buffer before a REIT must issue new units or cut distributions; a low ICR signals squeezed interest coverage. Here is a snapshot of the gearing and ICR for CLR’s major holdings:

| REIT | Gearing (Approx.) | ICR (Approx.) | MAS 50% Limit Buffer |

|---|---|---|---|

| CICT | 40.2% | 3.4× | +9.8pp |

| MPACT | 40.8% | 2.8× | +9.2pp |

| MINT | 38.1% | 4.5× | +11.9pp |

| FCT | 33.4% | 5.1× | +16.6pp |

| Keppel DC REIT | 36.7% | 5.6× | +13.3pp |

| Suntec REIT | 42.6% | 2.5× | +7.4pp |

| Parkway Life REIT | 35.3% | 7.2× | +14.7pp |

| Weighted Average | ~39.0% | ~4.0× | +11pp avg |

Source: Latest quarterly financial results per REIT. MAS Property Fund Appendix gearing limit: 50%. ICR = Interest Coverage Ratio (NPI / net interest expense).

The weighted average gearing across CLR’s major holdings is approximately 39% — comfortably below the MAS Property Fund Appendix 50% gearing ceiling. Under MAS guidelines, S-REITs can exceed 45% gearing only if they maintain an ICR above 2.5×; at 50% the headroom is exhausted. CLR’s portfolio average of 39% leaves a meaningful ~11 percentage-point buffer.

The weighted average ICR of approximately 4.0× is healthy — net property income covers interest expense four times over. The notable exception is Suntec REIT with an ICR of 2.5×, which while still compliant, has less headroom if interest rates were to spike again. However, Suntec’s 6.4% weighting in CLR limits the portfolio-level impact.

NAV vs. Unit Price: CLR currently trades near its NAV, at approximately a 1–2% premium. This modest premium reflects market confidence in the fund’s income generation capacity and its established track record since 2017.

Investing in CLR via CPF / SRS

One of CLR’s most distinctive advantages over individual S-REITs is its CPF Investment Scheme (Ordinary Account) eligibility. This means Singapore investors can use their CPF-OA savings — above the first SGD 20,000 — to purchase CLR units directly through an approved CPF investment broker (such as Phillip Securities, DBS Vickers, UOB Kay Hian, or OCBC Securities).

Why CPF-OA Investors Should Consider CLR

- CPF-OA earns the default rate of 2.5% p.a. (and up to 3.5% on the first SGD 20,000)

- CLR’s indicative yield of ~5.6% represents a +310 basis point uplift over the default CPF-OA rate

- Distributions are credited back to your CPF-OA account, available for further reinvestment or housing use

- Unlike using CPF for a home purchase, REIT ETF investments preserve capital flexibility (you can sell at any time)

SRS Investors

CLR is also SRS-eligible. SRS investors benefit from deferred income tax on contributions and investment returns, making CLR a tax-efficient wrapper for growing a retirement income portfolio. For more on optimising your CPF contributions alongside REIT investing, see our CPF investment strategy guide.

Important Caveats

While the yield pickup is attractive, CPF-OA investors should note: any capital loss when selling CLR must be topped up from the CPF-OA balance. The S-REIT sector has seen price drawdowns of 20–30% during rate-rising cycles (2022–2023). Investors with a 5+ year horizon and a high-income objective are best suited for CLR via CPF. Those needing certainty of capital for a home purchase in the near term should keep those funds in the default CPF-OA rate.

Looking to start with a robo-adviser before going direct on REITs? Platforms like Syfe, Endowus, and FSMOne also offer S-REIT-focused portfolios with CPF and SRS options.

Key Risks to Consider

No investment is without risk, and CLR is no exception. Here are the key risks investors should weigh before committing capital:

1. Interest Rate Sensitivity

S-REITs are highly sensitive to interest rate movements. If global rates rise again — driven by renewed inflation or central bank policy shifts — S-REIT unit prices and distributions could come under renewed pressure. CLR’s yield spread of ~240bps over SGS provides a buffer, but a sustained rate spike could compress that spread.

2. Concentration Risk

Despite holding 20–30 REITs, CLR’s top three holdings (CICT, MPACT, MINT) account for approximately 35% of the portfolio. A deterioration in any of these flagship REITs would have a disproportionate impact on CLR’s total return.

3. Foreign Exchange (FX) Risk

Several of CLR’s top holdings — including MPACT, Keppel DC REIT, and Frasers Centrepoint Trust — have significant overseas assets across China, Japan, Australia, and Europe. Currency weakness in these markets relative to SGD can reduce distributable income when repatriated to Singapore.

4. Property Market Cycle Risk

Commercial and industrial property values are cyclical. A slowdown in Singapore’s economy, oversupply in any sub-sector, or a correction in office/retail demand can compress NAV and constrain distribution growth.

5. ETF Tracking Error

CLR may not perfectly replicate the Morningstar® Singapore REIT Yield Focus Index return due to transaction costs, cash drag, and rebalancing friction. Over time, a small performance gap between the ETF and its index is normal and expected.

6. Regulatory Risk

MAS may revise rules governing S-REIT gearing, distribution requirements, or foreign ownership — any of which could affect underlying REIT payouts and CLR’s distributions accordingly.

Frequently Asked Questions

What is the current dividend yield of Lion-Phillip S-REIT ETF (CLR)?

How often does CLR pay dividends?

Can I buy CLR with my CPF?

What is the difference between CLR and CFA (Nikko AM Singapore REIT ETF)?

What is CLR's total expense ratio (TER)?

Is Lion-Phillip S-REIT ETF a good investment in 2026?

What is the minimum investment for CLR?

Our Verdict for 2026

The Lion-Phillip S-REIT ETF (CLR) remains one of Singapore’s most compelling ETFs for income investors in 2026. Its yield-focus methodology delivers the highest indicative yield among pure S-REIT ETFs (~5.6%), its underlying portfolio gearing is healthy at a weighted average of ~39% — comfortably below the MAS 50% cap — and CPF/SRS eligibility makes it genuinely accessible to Singapore’s mass-market investors.

The main trade-off versus Nikko AM’s CFA is a slightly higher TER (0.60% vs 0.55%) and smaller AUM. For investors prioritising maximum yield from a pure Singapore REIT vehicle, CLR has the edge. For investors who are more cost-sensitive and comfortable with a market-cap-weighted approach, CFA is worth a look. For those new to S-REITs who prefer a managed approach, robo-adviser platforms offering S-REIT portfolios via CPF or SRS are a sensible starting point.

Bottom line: In a 2026 environment where Singapore’s rate cycle has plateaued and property fundamentals are recovering, a passive S-REIT exposure via CLR — especially via CPF-OA — offers an attractive yield pickup over the risk-free rate with broad diversification across Singapore’s best-known REITs.

References

- SGX Stock Information — CLR (Lion-Phillip S-REIT ETF)

- Lion Global Investors — Lion-Phillip S-REIT ETF Fund Page

- MAS — Collective Investment Schemes (Property Fund Appendix, Gearing Limits)

This article is for informational purposes only and does not constitute financial advice. All data and yield figures referenced are approximate and as at March 2026. Past distributions are not indicative of future distributions. The Kopi Notes is not a licensed financial adviser. Please consult a qualified financial adviser before making investment decisions.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.