CPF Wage Ceiling 2026: What the S$8,000 Salary Cap Means for Your CPF Contributions

The complete Singapore employee guide — how the phased increases work, how much more you contribute, and how to maximise your retirement savings.

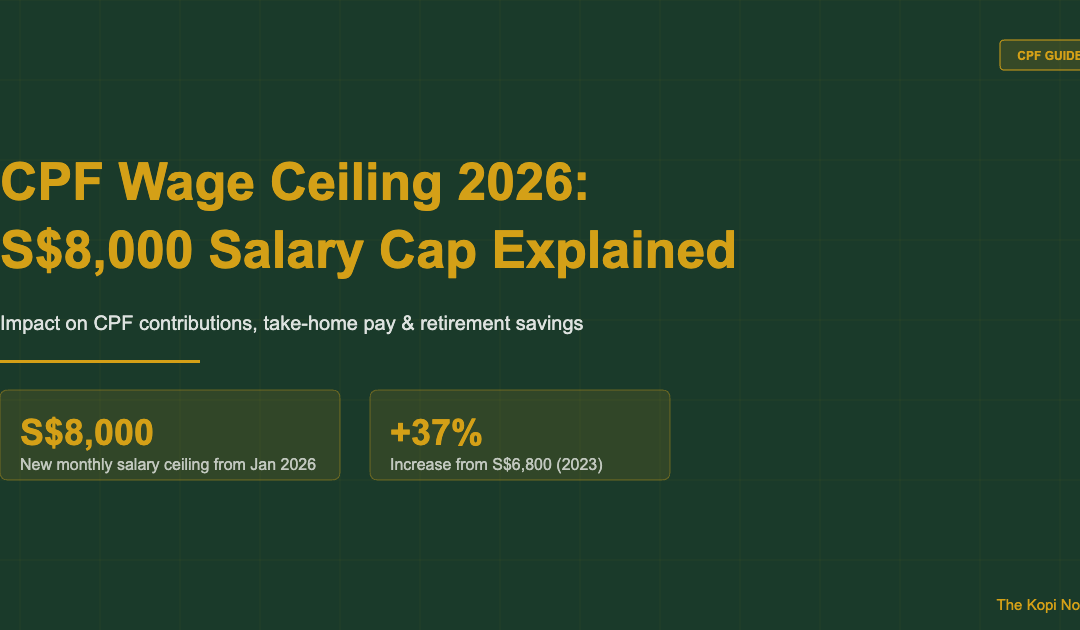

The CPF Ordinary Wage (OW) ceiling rose to S$8,000 per month from 1 January 2026 — the final step in a four-phase increase roadmap announced in 2023. For a Singaporean employee earning S$8,000 per month or more, this means CPF contributions are now computed on the full S$8,000, up from S$7,400 in 2025. Employers and employees earning above the old ceiling will see higher monthly CPF inflows, boosting OA, SA, and MediSave balances and accelerating retirement savings.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

Table of Contents

Contents — Click to expand

- What Is the CPF Ordinary Wage Ceiling?

- The Phased Increase Roadmap (2023–2026)

- How Much More Will You Contribute?

- CPF Contribution Rates by Age Group (2026)

- Senior Worker Contribution Rate Changes

- Impact on Take-Home Pay

- Long-Term Impact on Retirement Savings

- What Should You Do?

- Frequently Asked Questions

What Is the CPF Ordinary Wage Ceiling?

The CPF Ordinary Wage (OW) ceiling is the maximum monthly salary on which CPF contributions are calculated. Any salary earned above this cap does not attract CPF contributions for the ordinary wage component. It is distinct from the Annual Wage Supplement (AWS) and bonuses, which fall under the Additional Wage (AW) ceiling — a separate S$102,000 annual cap minus total ordinary wages contributed.

Before the 2023 Budget announcement, the OW ceiling had been frozen at S$6,000 since 2016. The government recognised this had not kept pace with median wage growth, leaving higher-earning Singaporeans with proportionally lower CPF accruals relative to their actual income. The four-phase roadmap was introduced specifically to close this gap and strengthen retirement adequacy.

As at 1 January 2026, the OW ceiling is S$8,000 per month — an increase of S$2,000 (or 33%) from the pre-2023 level of S$6,000.

The Phased Increase Roadmap (2023–2026)

The Ministry of Manpower (MOM) and CPF Board implemented the ceiling increase in four tranches to give employers time to plan for higher payroll costs. Here is the full timeline:

| Effective Date | New OW Ceiling | Change | Max Monthly CPF (≤55) |

|---|---|---|---|

| Before Sep 2023 | S$6,000 | — | S$2,220 |

| 1 Sep 2023 | S$6,300 | +S$300 | S$2,331 |

| 1 Jan 2024 | S$6,800 | +S$500 | S$2,516 |

| 1 Jan 2025 | S$7,400 | +S$600 | S$2,738 |

| 1 Jan 2026 (current) | S$8,000 | +S$600 | S$2,960 |

Source: CPF Board, Ministry of Manpower (MOM), January 2026. Max monthly CPF calculated at 37% total rate (employee 20% + employer 17%) for workers aged ≤55.

The roadmap is now complete. No further OW ceiling increases have been announced for 2027 or beyond as at June 2026.

How Much More Will You Contribute?

The practical impact depends entirely on your monthly salary. Workers earning S$6,800 or below in 2025 saw no change from the 2026 ceiling increase — they were already below both the old and new caps. The increase only affects those earning more than S$7,400 (the 2025 ceiling). Here is a worked breakdown:

Example: A Singapore employee earning S$8,000/month, aged 35, employed since 2025.

- Under the 2025 ceiling (S$7,400): Total CPF = 37% × S$7,400 = S$2,738/month (employee: S$1,480; employer: S$1,258)

- Under the 2026 ceiling (S$8,000): Total CPF = 37% × S$8,000 = S$2,960/month (employee: S$1,600; employer: S$1,360)

- Additional CPF per month: S$222 (employee: +S$120; employer: +S$102)

- Additional CPF per year: S$2,664

Over a 20-year working horizon, and assuming a 4% p.a. OA interest rate compound growth, that extra S$222/month compounds to approximately S$82,000 in additional CPF savings — a meaningful boost to retirement adequacy.

If you want to model your specific scenario, try TKN’s Singapore retirement calculator which factors in CPF OA/SA/RA balances, CPF LIFE payouts, and investment portfolio projections side by side.

CPF Contribution Rates by Age Group (2026)

The total CPF contribution rate varies by age. Older workers contribute and receive lower rates to remain cost-competitive in the labour market. All rates below apply to the monthly ordinary wage up to S$8,000.

| Age Group | Employee Rate | Employer Rate | Total Rate | Max Monthly CPF (S$8k) |

|---|---|---|---|---|

| ≤55 | 20% | 17% | 37% | S$2,960 |

| 55–60 | 15% | 15% | 30% | S$2,400 |

| 60–65 | 10.5% | 11.5% | 22% | S$1,760 |

| 65–70 | 7.5% | 9% | 16.5% | S$1,320 |

| Above 70 | 5% | 7.5% | 12.5% | S$1,000 |

Source: CPF Board contribution rate table, June 2026. Applicable to Singapore Citizens and Permanent Residents.

Senior Worker Contribution Rate Changes

Alongside the wage ceiling increase, CPF Board has been incrementally raising contribution rates for senior workers (aged 55–70) as part of the same 2023 Budget roadmap. The goal is to bring older workers’ CPF accrual rates closer to those of younger workers by 2030.

For the 55–60 age band, the combined rate rose from 26% (pre-2023) to 30% in January 2026 — a 4 percentage point increase phased over three years. This is particularly relevant for employees who are approaching Singapore’s re-employment age, which was raised to 69 in 2026 (with a statutory retirement age of 64 effective July 2026). To understand how this affects your overall CPF investment strategy, it is worth stress-testing your retirement income assumptions as your rate changes.

The changes do require employers to budget higher CPF payroll costs for older workers. However, the government has provided Wage Credit Scheme (WCS) support to offset part of the employer-side cost increase, particularly for lower-income senior workers.

Impact on Take-Home Pay

Higher CPF contributions reduce employees’ take-home cash — but only on the employee portion. Here is the net take-home effect at various salary levels after the 2026 ceiling change:

| Monthly Salary | 2025 Employee CPF | 2026 Employee CPF | Change in Take-Home |

|---|---|---|---|

| S$6,000 | S$1,200 | S$1,200 | No change |

| S$7,000 | S$1,480 | S$1,400 | +S$80 take-home |

| S$7,400 | S$1,480 | S$1,480 | No change |

| S$7,800 | S$1,480 | S$1,560 | −S$80 take-home |

| S$8,000+ | S$1,480 | S$1,600 | −S$120 take-home |

Source: CPF Board contribution rate table (June 2026). Employee CPF rate of 20% applies to workers aged ≤55. Workers aged 55–60 see smaller take-home reductions due to a lower employee rate (15%).

The trade-off is real: higher earners take home S$120 less per month in cash — but gain S$120 in CPF savings (split across OA, SA, and MediSave), which earn risk-free rates of 2.5%–5% p.a. For long-term retirement planning, this is generally a positive forced-savings outcome. You can use TKN’s CPF take-home pay calculator to model your exact scenario.

Long-Term Impact on Retirement Savings

The wage ceiling increase has the most meaningful impact for Singaporeans in the S$7,400–S$10,000 income range who are mid-career (ages 30–50). For these workers, the additional CPF contributions compound over 15–25 years before retirement, materially improving CPF LIFE payout prospects.

Scenario: Employee earns S$8,000/month, aged 35, retires at 65 (30-year horizon). Additional monthly CPF from ceiling increase: S$222/month total (employer + employee).

- OA portion (23 out of 37 percentage points) accrues at 2.5% p.a., with an extra 1% on the first S$20,000

- SA portion (8 out of 37 percentage points) accrues at 4% p.a., with an extra 1% on the first S$40,000

- MediSave portion (6 out of 37 percentage points) accrues at 4% p.a.

Over 30 years, this incremental S$222/month in CPF (weighted across OA/SA/MA at blended ~3.5% p.a.) compounds to approximately S$135,000 in additional CPF wealth. If transferred to the Retirement Account (RA) at 55 to meet the Enhanced Retirement Sum (ERS), this could boost CPF LIFE payouts by S$300–S$500 per month in retirement.

For context, the CPF ERS in 2026 is approximately S$426,000. Higher OW ceiling contributions make it meaningfully easier for higher earners to hit FRS or ERS targets without large voluntary top-ups.

Want to see how your retirement picture stacks up? The retirement planning guide walks through CPF LIFE payout scenarios and how to build passive income on top of CPF. You can also explore passive income strategies in Singapore to supplement your CPF LIFE payouts in retirement.

What Should You Do?

If you earn above S$7,400 per month, here are the practical steps to take now that the S$8,000 ceiling is in effect:

1. Check your January 2026 payslip

Your employer is legally required to apply the new ceiling from 1 January 2026. Log in to the CPF portal or check your CPF Statement to confirm that contributions are being computed on the correct base wage.

2. Update your retirement plan projections

If you were using S$7,400 as your CPF base in any retirement calculator, update it to S$8,000. The difference accumulates significantly over time. Use the CPF Retirement Sum Calculator to project your BRS/FRS/ERS readiness.

3. Consider voluntary top-ups to maximise SA/RA

The ceiling increase boosts your SA automatically, but if your SA has already reached the Full Retirement Sum (FRS), excess OW contributions flow to OA. In that case, consider voluntary cash top-ups to family members’ CPF accounts for additional tax relief under the Retirement Sum Topping-Up (RSTU) scheme.

4. Invest your OA wisely

The higher OA balance from the ceiling increase may give you additional CPF Investment Scheme (CPFIS) headroom. You can invest OA savings in eligible instruments — including Singapore REITs and ETFs — after keeping S$20,000 in your OA. See TKN’s CPF investment strategy guide for a framework.

5. Explore SRS contributions

If the ceiling increase reduces your take-home pay by S$120/month, this is also a good time to check whether topping up your Supplementary Retirement Scheme (SRS) account with a robo-advisor like Endowus (referral code 2V343) or Syfe (referral code SRPRFFFCD) makes sense. SRS contributions are deductible from chargeable income — reducing your income tax liability while growing your retirement nest egg.

Disclaimer: CPF rules are complex and change periodically. Always verify current rates and limits at cpf.gov.sg or consult a licensed financial adviser for personalised advice.

Frequently Asked Questions

What is the CPF wage ceiling in 2026?

The CPF Ordinary Wage (OW) ceiling is S$8,000 per month from 1 January 2026. This is the final step in a four-phase increase roadmap announced in Singapore Budget 2023. CPF contributions are only calculated on ordinary wages up to this cap — any monthly salary above S$8,000 does not attract further CPF contributions on the ordinary wage component.

How does the S$8,000 CPF salary ceiling affect my take-home pay?

If your monthly salary is S$7,400 or below, there is no change to your take-home pay from the 2026 ceiling increase. If you earn between S$7,401 and S$8,000, your employee CPF contributions increase by 20% on the additional wage above S$7,400 — reducing take-home by up to S$120/month for workers earning exactly S$8,000. The flip side is that your CPF OA, SA, and MediSave balances grow faster.

Is the CPF wage ceiling S$6,800, S$7,400, or S$8,000 in 2026?

The current ceiling as at January 2026 is S$8,000 per month. The S$6,800 figure applied from January 2024 to December 2024, and S$7,400 applied throughout 2025. The phased roadmap (S$6,300 → S$6,800 → S$7,400 → S$8,000) is now complete and no further changes have been announced.

Does the CPF wage ceiling apply to both Singapore Citizens and PRs?

Yes, the S$8,000 OW ceiling applies equally to Singapore Citizens (SC) and Permanent Residents (PR). However, CPF contribution rates differ slightly: first and second-year PRs have graduated contribution rates that phase up to full SC rates over time. The ceiling itself is the same for all SC and PR employees working in Singapore.

What happens to CPF contributions for salaries above S$8,000?

Salary above S$8,000 per month does not attract CPF contributions on the ordinary wage component. However, bonuses and variable pay (Additional Wages or AW) are still subject to CPF up to the Annual Wage Supplement (AWS) ceiling — which is calculated as S$102,000 minus the total ordinary wages already contributed in that year. So a worker earning S$10,000/month still gets CPF contributions on S$8,000 of their base pay plus eligible bonuses up to the AW ceiling.

How does the higher CPF wage ceiling help with retirement planning?

For a 35-year-old earning S$8,000/month, the ceiling increase adds approximately S$222/month in total CPF contributions (employer + employee). Compounded over 30 years at a blended CPF interest rate of ~3.5% p.a., this adds an estimated S$135,000 to total CPF wealth by age 65 — potentially boosting CPF LIFE monthly payouts by S$300–S$500 in retirement. The SA portion in particular benefits from the 4% p.a. guaranteed rate, making it a powerful long-term forced savings vehicle.

Can I use my extra CPF contributions to invest in REITs or ETFs?

Yes — the additional OA contributions from the wage ceiling increase can be invested through the CPF Investment Scheme (CPFIS-OA), provided you keep a minimum of S$20,000 in your OA. CPFIS-eligible assets include Singapore REITs listed on SGX, approved unit trusts, and endowment insurance policies. Note that SA funds cannot be invested once they reach the Full Retirement Sum (FRS). For a list of the best S-REITs available via CPFIS, see TKN’s guide on the best S-REITs in Singapore 2026.

Grow Your CPF Savings Further

Invest your OA via CPFIS or grow your SRS account with Singapore’s top robo-advisors. Use our referral links for exclusive sign-up bonuses.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.