CPF Contribution Changes April 2026: Complete Guide for Singapore Workers

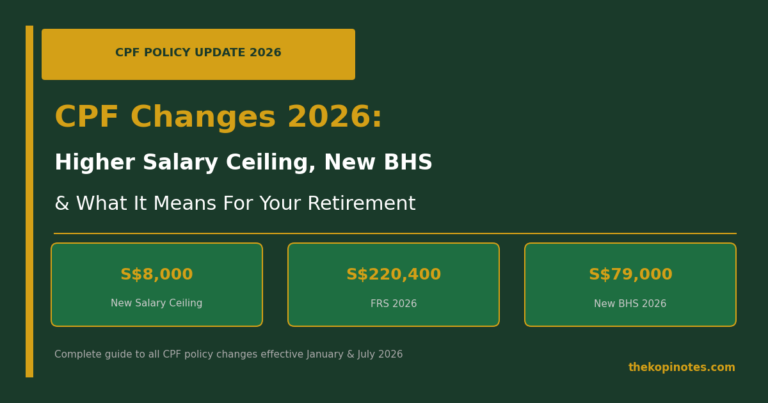

From 1 January 2026, Singapore’s CPF contribution rates for senior workers aged 55–65 increased by 1.5 percentage points in total — employer rates up 0.5% and employee rates up 1%. The monthly Ordinary Wage (OW) ceiling also rose to $8,000 (from $7,400), meaning higher earners now contribute CPF on a larger slice of their salary. All new contributions from the rate increase go directly into the Retirement Account (RA) to strengthen retirement savings.

Not financial advice. All figures are for educational reference only. Data as at April 2026 unless noted.

Table of Contents

Show Contents

- Overview: What Changed from 1 January 2026

- Full CPF Contribution Rate Table 2026

- Ordinary Wage Ceiling Raised to $8,000

- Dollar Impact: How Much More Goes Into Your CPF?

- Where Does the Extra CPF Go? Retirement Account Explained

- Government Offsets for Employers: CTO and SEC

- Investing Your CPF RA: Options Available

- Action Steps for Workers and Employers

- Frequently Asked Questions

Overview: What Changed from 1 January 2026

Singapore’s CPF system has been on a phased journey to close the gap between younger workers (who contribute at the full 37% total rate) and older workers (who historically contributed at lower rates). The changes effective 1 January 2026 mark a significant milestone — the final step in raising the Ordinary Wage ceiling and another increment in senior worker contribution rates.

The 2026 changes affect three groups specifically:

Workers aged above 55 to 60: Total CPF contribution rate rises from 32.5% to 34%. Employer share increases from 15.5% to 16%; employee share increases from 17% to 18%.

Workers aged above 60 to 65: Total CPF contribution rate rises from 23.5% to 25%. Employer share increases from 12% to 12.5%; employee share increases from 11.5% to 12.5%.

Workers aged above 65 to 70 and above 70: Rates remain unchanged at 16.5% and 12.5% respectively for 2026.

For workers aged 55 and below, the total 37% rate (employer 17% + employee 20%) remains unchanged.

This is part of Singapore’s Retirement and Re-employment Act (RRA) roadmap, announced by the government to gradually align senior worker contribution rates with those of younger workers, recognising that Singaporeans are working longer and need more retirement savings.

Full CPF Contribution Rate Table 2026

The table below shows the complete CPF contribution rates from 1 January 2026, for employees earning more than $750 per month. Rates for employees earning $500–$750 per month are phased and differ — refer to the CPF Board’s full rate table for those brackets.

| Age Group | Employer (%) | Employee (%) | Total (%) | Change vs 2025 |

|---|---|---|---|---|

| 55 and below | 17% | 20% | 37% | No change |

| Above 55 to 60 | 16% (+0.5%) | 18% (+1%) | 34% | +1.5% |

| Above 60 to 65 | 12.5% (+0.5%) | 12.5% (+1%) | 25% | +1.5% |

| Above 65 to 70 | 9% | 7.5% | 16.5% | No change |

| Above 70 | 7.5% | 5% | 12.5% | No change |

Source: CPF Board, effective 1 January 2026. Rates apply to employees earning >$750/month.

Ordinary Wage Ceiling Raised to $8,000

One of the most impactful changes for 2026 is the final step in the phased increase of the Ordinary Wage (OW) ceiling — the maximum monthly wage on which CPF contributions are calculated. From 1 January 2026, the OW ceiling rises from $7,400 to $8,000.

This means Singapore workers earning between $7,401 and $8,000 per month will now have CPF contributions calculated on their full salary, not capped at $7,400. For a worker earning $8,000/month, this represents an additional $600 base for CPF calculations each month.

The OW ceiling increase follows a phased schedule that began in 2023:

| Effective Date | OW Ceiling | Change |

|---|---|---|

| Before Sep 2023 | $6,000 | Baseline |

| 1 Sep 2023 | $6,300 | +$300 |

| 1 Jan 2024 | $6,800 | +$500 |

| 1 Jan 2025 | $7,400 | +$600 |

| 1 Jan 2026 | $8,000 | +$600 (Final step) |

Source: CPF Board. The Annual Salary Ceiling remains at $102,000.

The Annual Salary Ceiling remains unchanged at $102,000, which caps the total CPF-eligible wages per year (including both ordinary and additional wages like bonuses).

If you are building long-term wealth in Singapore, understanding how CPF feeds into your retirement planning is crucial. Use our Singapore retirement planning calculator to model how these changes affect your projected retirement nest egg.

Dollar Impact: How Much More Goes Into Your CPF?

For workers aged 55–60, the combined 1.5% rate increase translates to real dollars every month. Here are worked examples using Singapore dollar figures at different salary points:

Example 1: Worker aged 58, earning $5,000/month

Previously (2025): Total CPF = $5,000 × 32.5% = $1,625/month

From Jan 2026: Total CPF = $5,000 × 34% = $1,700/month

Additional CPF per month: $75 (employer pays $25 extra; employee pays $50 extra)

Additional CPF per year: $900 more into RA

Example 2: Worker aged 57, earning $8,000/month (OW ceiling)

Previously (2025): Total CPF on $7,400 × 32.5% = $2,405/month

From Jan 2026: Total CPF on $8,000 × 34% = $2,720/month

Additional CPF per month: $315 (combination of rate increase + OW ceiling lift)

Additional CPF per year: $3,780 more into RA

Example 3: Worker aged 62, earning $6,000/month

Previously (2025): Total CPF = $6,000 × 23.5% = $1,410/month

From Jan 2026: Total CPF = $6,000 × 25% = $1,500/month

Additional CPF per month: $90 (employer pays $30 extra; employee pays $60 extra)

Additional CPF per year: $1,080 more into RA

Note that the increase in employee contributions means a slight reduction in take-home pay. For a worker aged 58 earning $5,000, take-home reduces by $50/month — offset by a government CPF investment strategy advantage as that $50 earns guaranteed 4% p.a. in the RA.

Where Does the Extra CPF Go? Retirement Account Explained

A critical detail of the 2026 CPF changes: the entire increase from higher rates goes directly into the Retirement Account (RA), up to the Full Retirement Sum (FRS). This is not split across OA, SA, and MA like regular CPF contributions — it goes exclusively to RA.

For 2026, the key CPF retirement sums are:

| Retirement Sum | Amount (2026) | What It Means |

|---|---|---|

| Basic Retirement Sum (BRS) | $106,500 | Minimum CPF LIFE payout (~$900–$1,000/mo) |

| Full Retirement Sum (FRS) | $213,000 | Standard CPF LIFE payout (~$1,650–$1,800/mo) |

| Enhanced Retirement Sum (ERS) | $426,000 | Maximum CPF LIFE payout (~$3,300–$3,600/mo) |

Source: CPF Board 2026. Payout estimates are approximate and depend on CPF LIFE plan chosen at age 65.

The RA earns a guaranteed 4% per annum interest rate (plus an additional 1% on the first $60,000). This makes it one of the best risk-free returns available to Singapore residents. By channelling the rate increase directly to RA, the government ensures additional contributions compound towards CPF LIFE payouts.

If you want to model your projected CPF LIFE monthly payouts with these new rates, our CPF LIFE payout calculator has been updated for 2026 figures. For a broader view of how CPF fits into passive income planning, see our guide on passive income strategies in Singapore.

Government Offsets for Employers: CTO and SEC

To cushion the cost increase for employers, especially small and medium enterprises (SMEs), the government provides two key financial support schemes:

1. Contribution Offset (CTO)

The CPF Transition Offset (CTO) covers 50% of the employer’s CPF contribution increase in 2026. This is automatically credited to employers — no application needed. For each senior worker aged 55–65, the employer receives a CTO rebate on the 0.5 percentage point increase in their CPF contribution rate.

For example, if an employer has a worker aged 58 earning $6,000/month, the employer’s CPF increase is $6,000 × 0.5% = $30/month. The CTO covers 50%, so the employer nets only $15/month in additional cost per such employee.

2. Senior Employment Credit (SEC)

The Senior Employment Credit (SEC) provides wage offsets of up to 8% of the monthly wages of eligible senior workers to employers who hire Singaporeans aged 60 and above. The SEC is tiered by age and salary, and is paid quarterly by IRAS.

Together, the CTO and SEC mean most SMEs hiring senior workers will see their net cost impact from the 2026 CPF changes significantly cushioned — particularly for workers earning below $4,000/month who attract higher SEC rates.

For workers looking to optimise their overall investment picture alongside CPF, platforms like Endowus allow you to invest CPF OA funds in unit trusts, providing potential returns above the CPF OA’s 2.5% floor. You can also explore Syfe for investing your cash savings alongside growing your CPF RA.

Investing Your CPF RA: Options Available

Unlike the CPF Ordinary Account (OA) which can be invested via the CPF Investment Scheme (CPFIS), the Retirement Account is generally not investable under CPFIS once it is set up at age 55. Funds in your RA are locked in to grow at 4% p.a. and power your CPF LIFE payouts.

However, workers who have not yet turned 55 can still invest their OA and SA savings before the RA is created. Under CPFIS-OA, you can invest in unit trusts, ETFs, and stocks listed on the SGX. Under CPFIS-SA, only lower-risk instruments are permitted.

Key investment options available for CPF OA funds include index ETFs like SPDR STI ETF, and through robo-advisor platforms. Our full guide on CPF investment strategy covers how to optimise returns on your OA, SA, and MA balances before age 55.

For those who want to build a passive income portfolio outside CPF, Singapore REITs (S-REITs) remain one of the most popular choices, offering 5–7% dividend yields. See our list of best S-REITs in Singapore 2026 and our Singapore REIT ETF guide for a diversified approach to retirement income building.

For straightforward cash management alongside CPF, consider the FSMOne platform, which offers unit trusts and bond funds with low minimum investment sizes — useful for parking savings between CPF top-up windows.

Action Steps for Workers and Employers

For employees aged 55–65: Check your January 2026 CPF statement to confirm the new contribution rates have been applied correctly. Log into my.cpf.gov.sg and verify your RA balance reflects the incremental top-ups from the rate increase.

For workers near the $8,000 OW ceiling: If your monthly salary is between $7,401 and $8,000, you now have a higher CPF contribution base. Verify with your employer that payroll has been updated — some HR systems needed manual updates for the ceiling change.

For employers: Ensure your payroll software has been updated to reflect the new contribution rates and OW ceiling. The CTO will be automatically credited — no application needed. For SEC claims, submit quarterly via the IRAS myTax Portal.

For retirement planning: Use the updated contribution rates in your retirement projections. If you are not yet 55, consider using the higher projected RA balance in your CPF LIFE payout estimates. Our retirement calculator and Singapore T-bills guide can help you model short-term and long-term savings scenarios side by side.

Frequently Asked Questions

When exactly did the CPF contribution changes take effect?

Does the CPF rate increase affect my take-home pay?

I am 54 years old. Do the 2026 changes affect me?

What is the Ordinary Wage (OW) ceiling and why does it matter?

How does the CTO (CPF Transition Offset) work for employers?

Can I voluntarily top up my CPF RA to reach the Enhanced Retirement Sum?

How do CPF changes affect S-REIT or ETF investors?

Disclaimer: This article is for educational purposes only and does not constitute financial advice. CPF rates and retirement sums are subject to government policy changes. Always verify the latest figures directly with CPF Board (cpf.gov.sg). The Kopi Notes may earn referral fees from links to financial platforms on this page.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.