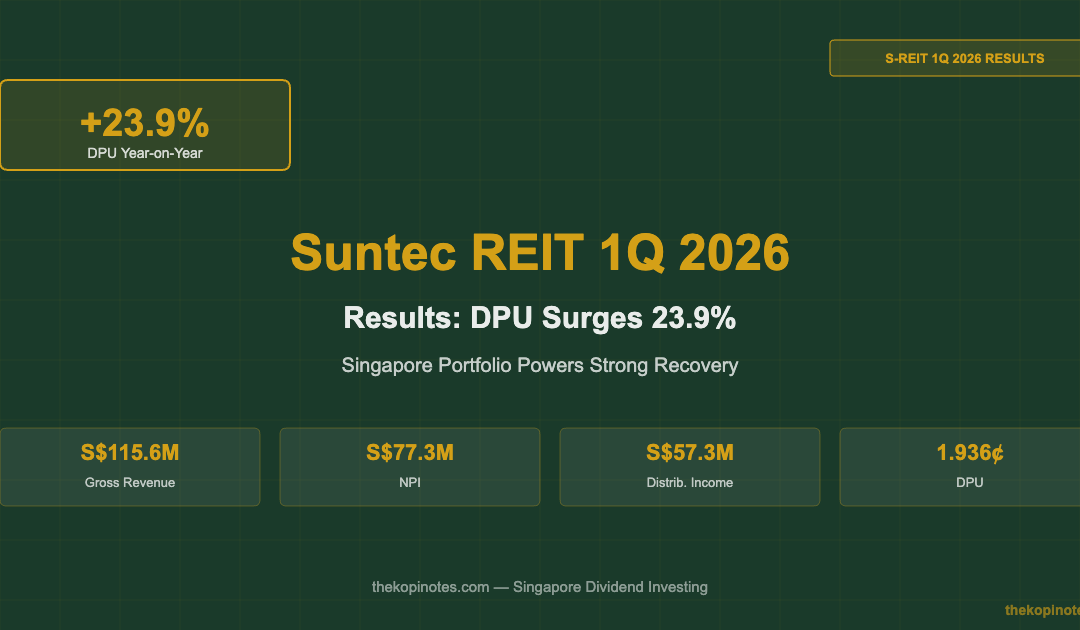

Suntec REIT 1Q 2026 Results: DPU Surges 23.9% as Singapore Portfolio Leads Recovery

A deep-dive into Suntec REIT’s first quarter FY2026 business update — financials, occupancy, debt, and what it means for income investors.

Suntec REIT (SGX: T82U) delivered a strong 1Q 2026 results update, with Distribution Per Unit (DPU) jumping 23.9% year-on-year to 1.936 Singapore cents. Distributable income surged 24.8% to S$57.3 million — driven by near-full occupancy in its Singapore office and retail assets, lower financing costs, and the restoration of Australian Managed Investment Trust (MIT) status. Gross revenue rose 1.9% to S$115.6 million for the quarter ended 31 March 2026.

Not financial advice. All figures are for educational reference only. Data sourced from Suntec REIT 1QFY2026 Business Update (April 2026) unless stated.

- DPU rose 23.9% YoY to 1.936 cents — the strongest quarterly growth in recent years

- Singapore office occupancy hit 98.8% with rent reversions of +4.9%; retail near-full at 99.0% with +15.0% reversion

- Lower debt costs (3.56% vs 3.71%) added S$5.8M to distributable income — a structural tailwind

Table of Contents

1Q 2026 Financial Highlights at a Glance

Suntec REIT’s first quarter 2026 business update (released 23 April 2026) showed broad-based improvement. The headline number is eye-catching: DPU surged 23.9% year-on-year. But the story underneath is just as important — stable top-line revenue, lower financing costs, and the recovery of Australian withholding tax provisions that had weighed on income in 1Q 2025.

Here’s the full financial summary:

| Metric | 1Q FY2025 | 1Q FY2026 | Change |

|---|---|---|---|

| Gross Revenue | S$113.5M | S$115.6M | +1.9% |

| Property Operating Expenses | S$36.4M | S$38.3M | +5.2% |

| Net Property Income (NPI) | S$77.1M | S$77.3M | +0.3% |

| Distributable Income | S$45.9M | S$57.3M | +24.8% |

Source: Suntec REIT 1QFY2026 Business Update Press Release, April 2026

The gap between NPI growth (+0.3%) and distributable income growth (+24.8%) is worth understanding. NPI was largely flat because higher leasing commissions offset the revenue gains. But distributable income jumped because:

- Joint venture income from MBFC and One Raffles Quay rose 9.0% year-on-year

- Financing costs fell by S$5.8 million — a direct result of lower interest rates and active refinancing

- A high Australian withholding tax provision in 1Q 2025 (due to temporary MIT status loss) was absent in 1Q 2026, creating a favourable base effect

Singapore Office & Retail Performance

The Singapore portfolio is the engine of Suntec REIT. It includes Suntec City Office, a 66.3% stake in Suntec Singapore Convention & Exhibition Centre, plus one-third interests in One Raffles Quay and Marina Bay Financial Centre (MBFC) Towers 1 and 2.

In 1Q 2026, Singapore delivered across the board.

| Segment | Occupancy (1Q 2026) | vs Prior Quarter | Rent Reversion |

|---|---|---|---|

| Singapore Office | 98.8% | +0.6pp | +4.9% |

| Singapore Retail (Suntec City Mall) | 99.0% | –0.5pp | +15.0% |

Source: Suntec REIT 1QFY2026 Business Update Presentation Slides, April 2026

The office occupancy improvement to 98.8% came from stronger leasing at Suntec City Office, One Raffles Quay, and MBFC Towers 1 and 2. The CBD office market in Singapore remains tight — with limited core CBD office supply coming through, landlords like Suntec REIT hold pricing power.

Retail is a standout. A rental reversion of +15.0% means tenants who renewed or signed new leases in 1Q 2026 paid 15% more than their expiring leases. That’s a strong signal of retail demand at Suntec City Mall.

The slight dip in retail occupancy to 99.0% (from 99.5% in 4Q 2025) reflects planned tenant churn — weaker operators exiting to create space for higher-quality tenants. Management expects committed occupancy to remain high with rent reversion near 10% going forward.

Suntec Convention faces more uncertainty. Corporates are taking a “wait-and-see” approach on events amid global macro uncertainty. Near-term opportunities from Middle East events provide some offset. Management expects Suntec Convention performance to remain stable in 2026.

For more context on how Suntec compares across the S-REIT universe, see our best S-REITs in Singapore 2026 guide, which covers yield, NAV discount, and debt metrics across the sector.

Australia & UK Portfolio Update

Suntec REIT’s overseas portfolio spans Australia (Sydney, Melbourne, Adelaide) and the United Kingdom (London). These assets add diversification but also face headwinds from their respective markets.

| Market | Occupancy (1Q 2026) | vs 4Q 2025 | Key Properties |

|---|---|---|---|

| Australia | 90.7% | +0.1pp | 177 Pacific Hwy, 21 Harris St, 55 Currie St, Southgate Complex, 477 Collins St |

| United Kingdom | 92.5% | Unchanged | The Minster Building, Nova Properties |

Source: Suntec REIT 1QFY2026 Business Update Presentation Slides, April 2026

Australia remains challenging. Incentive levels for office leases in Melbourne and Adelaide are running at 40–50% — meaning landlords often offer fit-out support or rent-free periods to attract tenants. That compresses net effective rent even when headline occupancy looks stable. Suntec REIT is adapting by subdividing large floor plates and creating fitted suites.

In the UK, vacancy levels in the City and West End of London sit at 7–8%, particularly in fringe locations and older buildings. Suntec’s Nova Properties is performing stably, but The Minster Building is impacted by vacancies with enhancement works ongoing.

The key win in Australia for 1Q 2026 was the retention of MIT (Managed Investment Trust) status. In 1Q 2025, its loss had led to a high withholding tax provision which depressed distributable income. Its restoration in 1Q 2026 contributed meaningfully to the 24.8% jump in distributable income — a favourable base effect that will benefit FY2026 comparisons.

Debt Profile and Financing Costs

Higher borrowing costs have been the biggest overhang for S-REITs over the past few years. In 1Q 2026, the tide turned meaningfully for Suntec REIT.

| Metric | 4Q FY2025 | 1Q FY2026 | Change |

|---|---|---|---|

| Aggregate Leverage | 41.5% | 41.6% | +0.1pp |

| Interest Coverage Ratio | 2.1x | 2.2x | +0.1x |

| Average Cost of Debt | 3.71% | 3.56% | -0.15pp |

| % Borrowings at Fixed Rates | ~65% | ~65% | Unchanged |

Source: Suntec REIT 1QFY2026 Business Update Press Release, April 2026

The average cost of debt fell from 3.71% to 3.56% — a reduction of 15 basis points. That directly translated into S$5.8 million lower financing costs, which flowed straight into distributable income. With 65% of borrowings on fixed rates, Suntec REIT has significant protection against rate volatility. The remaining 35% on floating rates will continue to benefit if central banks cut further.

Aggregate leverage at 41.6% sits slightly above management’s target of 40.0% — and well below the MAS regulatory limit of 50%. Near-term refinancing risk is low: only 3.9% of borrowings (S$160 million) mature in the remaining three quarters of FY2026.

For income investors planning a long retirement horizon, Suntec’s improving debt profile signals distribution sustainability. Our retirement planning calculator Singapore can help you model how a 5% yield REIT fits into your overall retirement income plan.

DPU and Distribution Details

Here’s what matters most to income investors — the actual cash you receive per unit.

| Detail | Value |

|---|---|

| 1Q FY2026 DPU | 1.936 Singapore cents |

| 1Q FY2025 DPU (comparative) | 1.563 Singapore cents |

| Year-on-Year Change | +23.9% |

| Ex-Date | 30 April 2026 |

| Record Date | 4 May 2026 |

| Payout Date | 29 May 2026 |

Source: Suntec REIT 1QFY2026 Business Update Press Release, April 2026

A 23.9% jump in DPU in a single quarter is exceptional. But context matters: part of this is the favourable base effect from 1Q 2025, when the absence of MIT status created a higher withholding tax provision in Australia. Strip out that base effect, and underlying DPU growth would be lower. Still, lower financing costs and improved operational performance are structural improvements — not one-off events.

At a share price of approximately S$1.47 (as at June 2026), Suntec REIT trades at a forward yield of around 5.2%. Analyst consensus target price is S$1.61, implying approximately 9.5% potential upside. That combination of yield and capital upside is what makes Suntec REIT worth watching for income investors right now.

For a broader view of how Suntec fits into the Singapore REIT landscape, our REIT Singapore complete guide 2026 covers how to evaluate yield, NAV discount, and debt metrics systematically across the sector.

Management Outlook for FY2026

CEO Mr Chong Kee Hiong’s commentary was cautiously optimistic. The core Singapore portfolio is performing well. The wild cards are Suntec Convention and the overseas assets.

Singapore Office: Management expects occupancy to remain high, with positive rent reversion near 5%. Limited CBD office supply and tight vacancies keep the market in landlords’ favour. This is a reliable income segment for 2026.

Suntec City Mall: Retail growth may moderate as consumers turn cautious amid global economic uncertainties. However, committed occupancy is expected to remain high with rent reversion near 10%. Mall management is actively refreshing the tenant mix to attract new market entrants and drive shopper traffic.

Suntec Convention: The most uncertain segment. Corporates are taking a “wait-and-see” approach on event spending. Near-term opportunities from Middle East events provide some offset. Management expects stability rather than growth here in 2026.

Australia: Competitive leasing conditions persist, with high incentive levels in Melbourne and Adelaide. Revenue is expected to be stable, supported by strong occupancies at key assets like 177 Pacific Highway and 477 Collins Street.

United Kingdom: London vacancy remains elevated at 7–8% in fringe locations. Nova Properties should be stable; The Minster Building remains impacted by vacancies with enhancement works underway.

What This Means for Income Investors

Here’s the plain-English summary of what Suntec REIT’s 1Q 2026 results mean for you as an income investor in Singapore.

The positives are real. Singapore office and retail are near-fully occupied. Rent reversions are strongly positive. Financing costs are falling. These are structural improvements that should sustain distributions through FY2026.

The 24.8% distributable income jump is partly a base effect. The Australian MIT status issue in 1Q 2025 created an unusually high withholding tax provision. Its absence in 1Q 2026 flatters the comparison. Don’t expect 24% growth every quarter — but underlying growth is still solid.

Overseas assets carry risk. Australia and the UK face leasing headwinds that Singapore doesn’t. If global office demand softens further, these assets could weigh on consolidated NPI.

Aggregate leverage at 41.6% is manageable but elevated. It limits Suntec’s ability to make debt-funded acquisitions near-term. The management target is 40% — they’re making progress.

At ~5.2% forward yield with analyst upside of ~9.5%, Suntec REIT offers a reasonable total return case for investors willing to accept the overseas property mix. For pure Singapore-focused REIT exposure, you might prefer alternatives like Mapletree Industrial Trust or CapitaLand Integrated Commercial Trust. But for income with diversification across three geographies, Suntec remains a solid mid-tier S-REIT.

Thinking about how to build a passive income portfolio around S-REITs? Our passive income Singapore 2026 guide covers how dividend investors approach portfolio construction — including how much to allocate to S-REITs versus bonds and CPF savings.

If you’re investing via a robo-advisor or managed platform, check the Endowus referral code for the Endowus Income Portfolios which include S-REIT exposure, or the Syfe referral code (code: SRPRFFFCD) for Syfe REIT+ — a curated S-REIT portfolio that includes diversified commercial REIT holdings.

Frequently Asked Questions

What was Suntec REIT's DPU for 1Q 2026?

Suntec REIT’s Distribution Per Unit (DPU) for 1Q FY2026 (quarter ended 31 March 2026) was 1.936 Singapore cents — up 23.9% year-on-year from 1.563 cents in 1Q FY2025. The payout date for this distribution was 29 May 2026, with an ex-date of 30 April 2026.

Why did Suntec REIT's distributable income jump 24.8% in 1Q 2026?

The 24.8% jump in distributable income to S$57.3 million was driven by three factors. First, stronger performance from the Singapore office and retail portfolio — near-full occupancy with positive rent reversions. Second, lower financing costs, with the average cost of debt falling from 3.71% to 3.56%, saving S$5.8 million. Third, a favourable base effect — in 1Q 2025, the loss of Australian Managed Investment Trust (MIT) status led to a higher withholding tax provision that did not recur in 1Q 2026.

What is Suntec REIT's occupancy rate in 1Q 2026?

Suntec REIT’s Singapore office portfolio occupancy was 98.8% as at 1Q 2026, up 0.6 percentage points from 4Q 2025. Singapore retail was at 99.0%, slightly lower than the 99.5% in 4Q 2025 due to planned tenant churn. Its Australia portfolio occupancy was 90.7% and the UK portfolio was 92.5% — both remaining above 90%.

Is Suntec REIT a good buy in 2026?

This is not financial advice, but here is the factual picture. At approximately S$1.47 per unit (as at June 2026), Suntec REIT offers a forward yield of around 5.2%. Analyst consensus target price is S$1.61, implying about 9.5% potential upside. Its Singapore portfolio is near-fully occupied with strong positive rent reversions, and financing costs are falling. The main risks are its overseas assets in Australia and the UK, which face more challenging leasing markets, and aggregate leverage of 41.6% which limits near-term acquisition capacity.

What is Suntec REIT's aggregate leverage in 2026?

Suntec REIT’s aggregate leverage was 41.6% as at 31 March 2026, slightly above its management target of 40.0%. The MAS regulatory limit for S-REITs is 50%, so Suntec remains well within compliance. Near-term refinancing risk is low — only 3.9% of borrowings (approximately S$160 million) are due in the remaining three quarters of FY2026.

How does Suntec REIT compare to other commercial S-REITs in Singapore?

Suntec REIT is one of Singapore’s largest diversified commercial REITs, owning office and retail assets in Singapore, Australia, and the UK. Compared to CapitaLand Integrated Commercial Trust (CICT) or Keppel REIT, Suntec has greater overseas exposure which adds diversification but also risk. Its Singapore CBD assets — Suntec City, One Raffles Quay, and MBFC stakes — are among the most prime commercial properties in the city-state. Its forward yield of ~5.2% is competitive with peers. For Singapore-focused commercial REIT exposure without overseas risk, CICT may be a closer comparison.

Start Earning Passive Income from S-REITs

Invest in Singapore REITs through robo-advisors or brokerages. Use our referral links for sign-up bonuses.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.