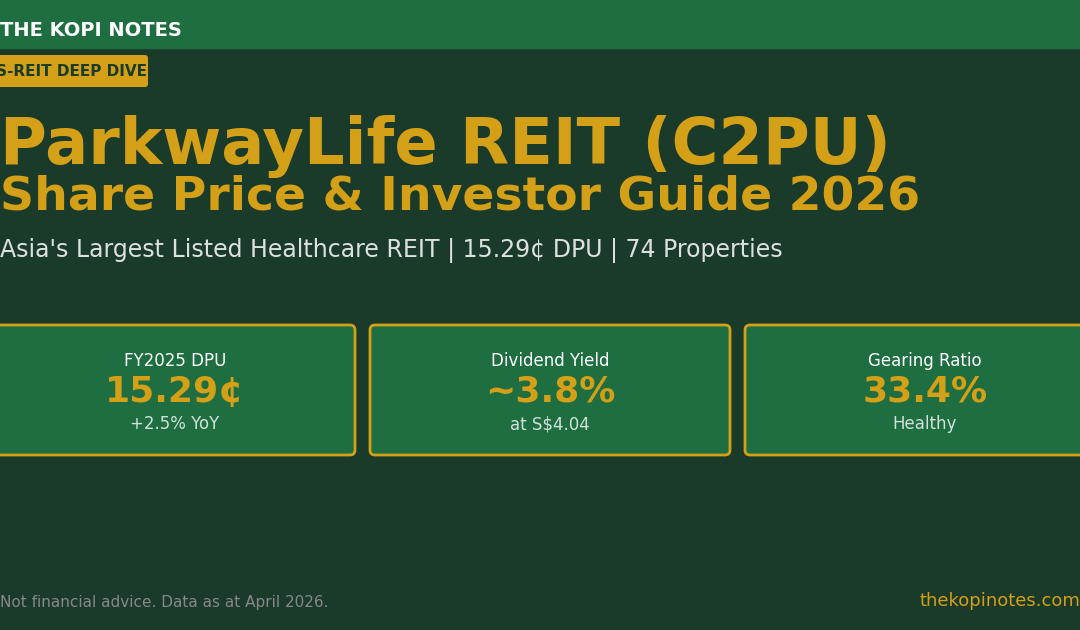

ParkwayLife REIT (C2PU): Complete Investor Guide 2026

Asia’s largest listed healthcare REIT — 15.29¢ DPU • 74 properties • Singapore, Japan & France

ParkwayLife REIT (SGX: C2PU) is Asia’s largest listed healthcare real estate investment trust, with a portfolio of 74 properties valued at approximately S$2.57 billion spanning Singapore, Japan, and France. For Singapore investors seeking defensive, inflation-linked income, PLife REIT stands apart: its master leases are structured with built-in rent escalation mechanisms, and it has delivered 17 consecutive years of DPU growth — a feat virtually unmatched in the S-REIT universe.

This guide covers everything you need to know about ParkwayLife REIT’s share price, DPU history, dividend yield, portfolio strategy, and 2026 outlook — including the landmark 24.3% Singapore hospital rent jump that should drive meaningful DPU growth this year.

This article is for informational purposes only and does not constitute financial advice. Data as at April 2026. Always conduct your own due diligence before investing.

Table of Contents

Contents — Click to expand

- What Is ParkwayLife REIT?

- Share Price Performance 2026

- DPU History (FY2019–FY2025)

- Dividend Yield Analysis

- Portfolio: Singapore, Japan & France

- The 2026 Singapore Hospital Rent Jump

- Key Financial Metrics & Gearing

- Peer Comparison with Other S-REITs

- 2026 Outlook & Catalysts

- Is ParkwayLife REIT Worth Buying?

- How to Invest in C2PU via CPF/SRS

- Frequently Asked Questions

What Is ParkwayLife REIT?

ParkwayLife REIT was listed on SGX in August 2007 and is managed by Parkway Trust Management Limited, a wholly-owned subsidiary of IHH Healthcare Berhad — one of the world’s largest private healthcare groups. This ownership structure is central to PLife REIT’s appeal: its Singapore anchor assets (Mount Elizabeth, Gleneagles, and Parkway East hospitals) are leased back to IHH under a long-term master lease with CPI-linked rent escalation.

Key facts (as at 31 December 2025):

- Portfolio size: 74 properties, total AUM ~S$2.57 billion

- Markets: Singapore (3 hospitals), Japan (60 nursing homes & care facilities), France (11 nursing homes)

- REIT manager: Parkway Trust Management (subsidiary of IHH Healthcare)

- DPU track record: 17 consecutive years of growth

- Listing date: 23 August 2007, SGX Mainboard

PLife REIT is often described as a “defensive” S-REIT because its healthcare tenants — hospitals and nursing homes — generate relatively stable, demand-inelastic revenue regardless of economic cycles. Ageing populations across Singapore, Japan, and France only strengthen the long-term demand thesis.

ParkwayLife REIT Share Price 2026

As at April 2026, ParkwayLife REIT (C2PU) trades at approximately S$4.04 per unit. Here is the current share price context:

| Metric | Value |

|---|---|

| Share Price (Apr 2026) | S$4.04 |

| 52-Week Range | S$3.92 – S$4.44 |

| Market Capitalisation | ~S$1.75 billion |

| P/NAV | ~1.0x – 1.1x |

| Average 12-Month Analyst Target | S$4.81 |

| Units Outstanding | ~432 million |

C2PU has shown relative resilience in 2026 despite macro headwinds — the defensive nature of healthcare assets and the upcoming Singapore rent uplift have supported sentiment. Analyst consensus sits at Buy/Accumulate with a price target range of S$4.11 to S$5.45.

DPU History: 17 Consecutive Years of Growth

One of PLife REIT’s most compelling attributes is its unbroken DPU growth streak — 17 consecutive years from listing through FY2025. In a period that included the Global Financial Crisis, COVID-19, and aggressive interest rate hikes, PLife REIT never cut its distribution.

| Financial Year | DPU (cents) | YoY Growth |

|---|---|---|

| FY2019 | 13.35¢ | +1.7% |

| FY2020 | 13.56¢ | +1.6% |

| FY2021 | 14.08¢ | +3.8% |

| FY2022 | 14.40¢ | +2.3% |

| FY2023 | 14.77¢ | +2.6% |

| FY2024 | 14.92¢ | +1.0% |

| FY2025 | 15.29¢ | +2.5% |

The FY2025 DPU of 15.29 Singapore cents was driven by 7.6% gross revenue growth and 8.0% NPI growth, supported by the France portfolio (11 nursing homes acquired December 2024) and continued organic rental growth in Japan. The second-half FY2025 DPU alone was 7.64¢, up 3.5% YoY.

For CPF and SRS investors, distributions are paid semi-annually (typically around March and September). You can use our DRIP Calculator to model what reinvesting PLife REIT distributions would do to your long-term returns.

Dividend Yield Analysis

At S$4.04 per unit and a FY2025 DPU of 15.29¢, PLife REIT’s trailing dividend yield is approximately 3.8%. This is below the S-REIT sector average of 5–6%, which often prompts investors to ask: is PLife REIT overvalued?

The answer lies in understanding what you are paying for:

- Quality premium: PLife REIT’s 17-year unbroken DPU growth streak commands a valuation premium over peers with more volatile distributions.

- Inflation linkage: Singapore hospital rents are CPI-linked, providing built-in income protection against rising prices.

- Operator quality: IHH Healthcare (one of Asia’s largest listed hospital groups) is the anchor tenant in Singapore — credit risk is extremely low.

- Defensive demand: Healthcare services are largely non-cyclical. Nursing home and hospital occupancy does not collapse in recessions.

That said, investors seeking higher income immediately may prefer higher-yielding S-REITs. Our S-REIT Dividend Yield Calculator helps you compare income across the sector and our REIT Yield vs Bond Spread Calculator shows whether the current yield makes sense relative to the risk-free rate.

Chart: ParkwayLife REIT’s ~3.8% yield is the lowest in the peer group, reflecting its defensive premium. Source: SGX filings, company results, April 2026.

Portfolio Overview: Singapore, Japan & France

PLife REIT owns 74 healthcare properties across three countries. Here is a breakdown of each segment:

Singapore (3 properties — ~53% of AUM)

The three Singapore hospitals — Mount Elizabeth, Gleneagles, and Parkway East — are the crown jewel of the portfolio. They are leased to IHH Healthcare subsidiaries on long-term master leases with:

- CPI-linked annual rent escalation (typically 1–3% per year)

- A minimum guaranteed rent reviewed every three years

- A 2026 rent reset to S$99.1 million (up 24.3% from S$79.7 million in FY2025)

Though just three properties, Singapore contributes the majority of income stability and predictability.

Japan (60 properties — ~34% of AUM)

Japan’s rapidly ageing population makes it a natural fit for healthcare REIT expansion. PLife REIT’s 60 Japan nursing homes and care facilities are spread across multiple prefectures. The Japan portfolio benefits from:

- Long-term leases (typically 10–20 years) with established Japanese nursing home operators

- Yen-denominated income, with partial currency hedging

- Organic rent escalation embedded in most leases

France (11 properties — ~13% of AUM)

In December 2024, PLife REIT completed the acquisition of 11 nursing homes in France — its first foray into Europe. The France portfolio contributed S$5.8 million in gross revenue in 1H2025 and was immediately accretive to DPU. The REIT also secured tax exemptions on foreign-sourced dividend and interest income, generating annual tax savings of ~S$1.7 million.

The 2026 Singapore Hospital Rent Jump: A Game-Changer

The single most important catalyst for PLife REIT in 2026 is the 24.3% increase in minimum guaranteed rent for its Singapore hospitals, rising from S$79.7 million in FY2025 to S$99.1 million in FY2026. This uplift was built into the 2021 master lease renewal — when IHH agreed to a ~40% rent increment and a 20-year lease extension in exchange for long-term certainty.

In practice, this means PLife REIT’s Singapore income is locked in at meaningfully higher levels from 2026 onward. Management guided at the 2026 AGM that this uplift — combined with continued Japan organic growth and France accretion — is expected to drive DPU growth in FY2026. Analyst forecasts point to FY2026 DPU of approximately 16.5–17.0¢, implying potential yield improvement even at current prices.

Key Financial Metrics & Gearing (FY2025)

| Metric | FY2025 Value |

|---|---|

| Gross Revenue | ~S$185M (+7.6% YoY) |

| Net Property Income (NPI) | ~S$172M (+8.0% YoY) |

| Distributable Income | ~S$99M (+9.1% YoY) |

| Full-Year DPU | 15.29¢ (+2.5% YoY) |

| Gearing Ratio | 33.4% |

| % Borrowings on Fixed Rate | ~97% |

| Total Assets (AUM) | ~S$2.57 billion |

| Occupancy Rate | >99% (master leases) |

| Debt Maturity (LT) | Oct 2026 (next major) |

PLife REIT’s gearing of 33.4% is well below the MAS regulatory cap of 50%, giving it ample headroom for further acquisitions. With 97% of borrowings on fixed rates, the REIT is largely insulated from near-term interest rate volatility — a significant advantage in the current environment. You can model gearing scenarios using our S-REIT Gearing Ratio Calculator.

Peer Comparison: PLife REIT vs Other S-REITs

| REIT | Sector | Yield (Apr 2026) | Gearing | DPU Growth |

|---|---|---|---|---|

| ParkwayLife REIT | Healthcare | ~3.8% | 33.4% | 17 yrs consecutive |

| Frasers Centrepoint Trust | Retail | ~6.0% | ~39% | Stable |

| Mapletree Logistics Trust | Industrial/Logistics | ~6.4% | ~39% | Declining |

| CapitaLand Ascendas REIT | Industrial | ~5.8% | ~36% | Stable |

| Keppel DC REIT | Data Centre | ~4.3% | ~33% | Growing |

PLife REIT’s lower yield reflects its defensive premium. Investors willing to accept a lower current yield in exchange for greater income certainty, CPI linkage, and historically unbroken DPU growth will find C2PU compelling. For a full comparison of S-REIT yields, see our Best S-REITs Singapore 2026 guide.

2026 Outlook & Key Catalysts

Looking ahead, several tailwinds support PLife REIT’s FY2026 performance:

- Singapore rent uplift (+24.3%): The S$19.3M increase in minimum Singapore hospital rent is locked in from FY2026. This single item is expected to be the primary DPU growth driver in 2026.

- France accretion continuing: The 11 France nursing homes acquired in December 2024 will contribute a full year of income in FY2026 (vs. only partial in FY2025).

- Japan organic growth: Lease step-ups in Japan nursing homes continue to generate incremental income, supported by Japan’s structural demographic tailwind.

- Sustainable financing milestone: In February 2026, PLife REIT established its Sustainable Financing Framework and issued its first social loan and green bond, diversifying funding sources and signalling long-term institutional credibility.

- Rate cut tailwind: With 97% of borrowings on fixed rates, PLife REIT is largely protected from near-term rate movements. If rates fall, there is potential for refinancing savings from October 2026 onward.

Key risks to watch: JPY/SGD currency exposure (Japan contributes ~34% of AUM), debt refinancing in October 2026, and any regulatory changes to France’s healthcare reimbursement system.

Is ParkwayLife REIT Worth Buying in 2026?

PLife REIT suits a specific type of Singapore investor: one who prioritises income reliability over maximum yield. If you are building a retirement portfolio and want a REIT you can hold for 10–20 years with minimal drama, C2PU makes a strong case.

Buy if: You want inflation-linked, growing income; you value DPU track record over raw yield; you are comfortable with a 3.8% starting yield that may grow to 4.0–4.5% over time via DPU growth; you want healthcare sector exposure in your S-REIT portfolio.

Think twice if: You need maximum current income (other S-REITs yield 5.5–7%); you are not comfortable with Japan currency exposure; you need short-term capital gains rather than steady income.

For retirement planning context, our Retirement Calculator guide and Retirement Planning Calculator can help you model how PLife REIT distributions fit into your overall income strategy.

How to Invest in PLife REIT via CPF or SRS

ParkwayLife REIT (C2PU) is approved for CPF Investment Scheme (CPFIS-OA) and SRS (Supplementary Retirement Scheme) investing, making it particularly attractive for Singapore investors looking to put idle CPF-OA funds or SRS balances to work.

- CPF-OA: You can invest up to 35% of your investible OA savings in C2PU through any CPFIS-approved broker. Distributions received go into your CPF account (not paid out in cash).

- SRS: Distributions received from SRS holdings are deferred for tax purposes until withdrawal, making PLife REIT a compelling hold in an SRS account.

- Recommended platforms: Endowus (for fund access), or direct SGX brokerage via Tiger Brokers, Syfe Trade, or FSMOne. See our Endowus referral code, Syfe referral code, or FSMOne referral code for sign-up bonuses.

Use our CPFIS Calculator to see whether investing CPF-OA in C2PU makes more sense than leaving it to compound at 2.5% p.a.

Frequently Asked Questions

What is ParkwayLife REIT's current dividend yield?

How often does ParkwayLife REIT pay dividends?

Is ParkwayLife REIT a good long-term investment?

What is ParkwayLife REIT's gearing ratio?

Can I buy ParkwayLife REIT using CPF?

What drove the 24.3% Singapore hospital rent jump in 2026?

Does ParkwayLife REIT have exposure to Japan currency risk?

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.