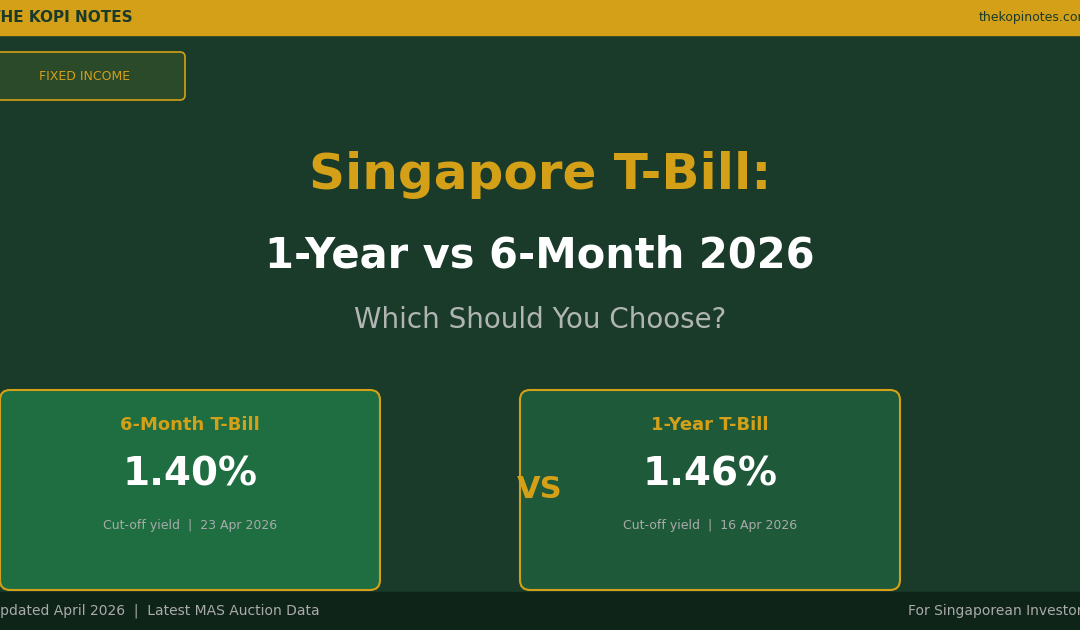

Singapore T-bills have become one of the most popular short-term investments for local investors — low risk, government-backed, and offering yields that often beat fixed deposits. But if you’re deciding between the 6-month T-bill and the 1-year T-bill, which one makes more sense for you right now?

Based on the latest April 2026 MAS auction results, the 6-month T-bill cut-off yield came in at 1.40% p.a. (23 Apr 2026), while the 1-year T-bill yielded 1.46% p.a. (16 Apr 2026). The gap is narrow — but your choice should come down to more than just yield. Liquidity needs, reinvestment risk, and your broader retirement or CPF strategy all play a role.

In this guide, we break down both instruments, compare their April 2026 yields head-to-head, and help you decide which is the right fit for your portfolio.

Table of Contents

What Are Singapore T-Bills?

Singapore Treasury Bills (T-bills) are short-term debt instruments issued by the Singapore Government through the Monetary Authority of Singapore (MAS). They are sold at a discount to their face value, and the difference between your purchase price and the face value (S$1,000 per lot) represents your interest return.

Key features:

- Issued by: Singapore Government (via MAS) — AAA-rated sovereign debt

- Minimum investment: S$1,000 (multiples of S$1,000)

- Tenures: 6 months or 1 year

- Interest: Paid at maturity (zero-coupon, discount instrument)

- Eligible accounts: Cash (via bank/CDP), CPF-OA, SRS

- Tax: Returns are not subject to Singapore income tax

T-bills are auctioned on a competitive and non-competitive bid basis. Most retail investors submit non-competitive bids — you receive the auction’s cut-off yield regardless of your bid price, guaranteed allotment up to S$1 million per auction.

Latest April 2026 Auction Results

Here are the most recent cut-off yields from MAS T-bill auctions in April 2026:

| T-Bill Tenor | Issue Code | Auction Date | Cut-Off Yield | Total Applications |

|---|---|---|---|---|

| 6-Month | BS26108W | 23 Apr 2026 | 1.40% p.a. | S$19.2 billion |

| 1-Year | BY26101H | 16 Apr 2026 | 1.46% p.a. | S$12.4 billion |

| 6-Month (prev) | BS26107X | 9 Apr 2026 | 1.47% p.a. | S$14.6 billion |

| 1-Year (prev) | BY26100L | 15 Jan 2026 | 1.44% p.a. | S$12.1 billion |

Source: MAS T-Bill Statistics. Cut-off yields are indicative and subject to change at each auction.

Notably, demand for the 6-month T-bill surged to S$19.2 billion in the 23 April auction — a significant jump from S$14.6 billion previously. This reflects strong retail appetite for short-duration government paper, likely driven by global macro uncertainty and investors parking cash while waiting for interest rate clarity.

The 1-year T-bill currently offers a slight premium of 6 basis points over the 6-month instrument (1.46% vs 1.40%). This narrow spread is unusual — typically the 1-year should offer a more meaningful premium for the extra duration risk.

6-Month vs 1-Year T-Bill: Key Differences

Both instruments are issued by the same sovereign borrower and carry zero credit risk, but they differ in ways that matter to practical investors:

| Feature | 6-Month T-Bill | 1-Year T-Bill |

|---|---|---|

| Current yield (Apr 2026) | 1.40% p.a. | 1.46% p.a. |

| Auction frequency | Every 2 weeks | Quarterly |

| Lock-up period | 6 months | 12 months |

| Reinvestment frequency | Twice per year | Once per year |

| Reinvestment risk | Higher (rates may fall) | Lower (locked in longer) |

| Liquidity | Better (shorter lock-up) | Lower |

| CPF-OA eligible | Yes | Yes |

| SRS eligible | Yes | Yes |

| Early redemption | Not allowed (secondary market only) | Not allowed (secondary market only) |

The Reinvestment Risk Trade-Off

With the 6-month T-bill, you’ll need to reinvest every 6 months. If rates fall by the time your T-bill matures, your next rollover will be at a lower yield. The 1-year T-bill locks in today’s 1.46% for a full 12 months — valuable if you believe rates are heading lower.

Conversely, if you expect rates to rise (e.g., due to a Fed hawkish pivot or MAS tightening), rolling the 6-month T-bill gives you the flexibility to capture higher yields sooner.

Yield Comparison: T-Bills vs Fixed Deposits vs SSB (April 2026)

T-bills don’t exist in a vacuum. Here’s how they compare to other low-risk instruments for the cash portion of your portfolio:

| Instrument | Yield / Return | Lock-Up | Flexibility |

|---|---|---|---|

| 6-Month T-Bill | 1.40% p.a. | 6 months | No early exit |

| 1-Year T-Bill | 1.46% p.a. | 12 months | No early exit |

| Best Fixed Deposits (Apr 2026) | Up to 1.50% p.a. | 3–12 months | Penalty for early break |

| SSB (Apr 2026 issue) — 1 Year | 1.40% p.a. | Flexible (redeem any month) | Full flexibility, no penalty |

| SSB — 10-Year Average | 2.14% p.a. | Up to 10 years | Full flexibility |

| CPF-OA (if not invested) | 2.50% p.a. | N/A (in CPF) | Use for T-bills, housing, CPFIS |

Rates as of April 2026. Fixed deposit rates vary by bank and deposit size. SSB 10-year average is for the April 2026 issue.

Key takeaway: At 1.46%, the 1-year T-bill edges out the SSB at the 1-year mark (1.40%) and competes closely with the best fixed deposits (up to 1.50%). The SSB’s full flexibility — redeem any month with no penalty — makes it appealing if you might need the money before maturity. However, if you’re certain you won’t need the funds for 12 months, the 1-year T-bill or a competitive fixed deposit may serve you better.

For longer-term savings (3–10 years), the SSB’s 10-year average of 2.14% is hard to beat for a capital-guaranteed product. And if the money is sitting in your CPF-OA, the baseline 2.50% return means investing in T-bills below that rate would actually reduce your effective return after accounting for the CPF floor.

You can compare T-bill, SSB, and fixed deposit yields side by side using our T-Bill, SSB & Fixed Deposit Comparison Calculator.

Who Should Choose Which T-Bill?

Choose the 6-Month T-Bill If:

- You need your money back within 6 months (e.g., upcoming housing downpayment, emergency buffer)

- You believe interest rates may rise — rolling every 6 months lets you capture higher yields

- You want to reinvest regularly and stay flexible in a volatile rate environment

- You’re using CPF-OA funds and want to align with CPF’s quarterly interest crediting cycle

Choose the 1-Year T-Bill If:

- You won’t need the capital for at least 12 months

- You believe rates will fall over the next year — locking in 1.46% now protects you from rate drops

- You want lower admin burden (only one rollover per year vs two)

- You’re building a simple bond ladder with annual rungs

Consider Alternatives If:

- Yields are below your CPF-OA rate (2.50%): Leaving funds in CPF-OA may be more beneficial than investing in T-bills at 1.40–1.46%

- You need full flexibility: Singapore Savings Bonds (SSB) offer monthly redemption with no lock-up — at the same 1-year yield of 1.40%

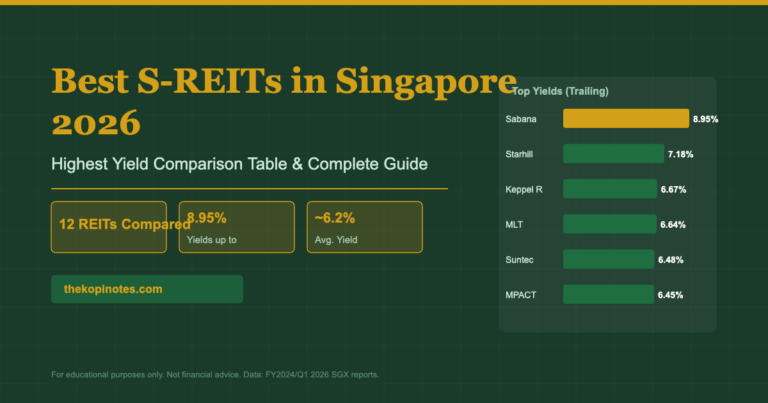

- You’re looking for higher income: Consider S-REITs or dividend ETFs for yields of 5–7%, with appropriate risk tolerance. See our Best S-REITs Singapore 2026 guide

For retirement planning context, understanding how your short-term cash instruments (T-bills, SSB, FD) fit alongside long-term CPF LIFE and investment assets is essential. Use our Retirement Planning Calculator to model your full income picture.

How to Apply for Singapore T-Bills

You can apply for T-bills through ATM, internet banking, or mobile banking from DBS/POSB, OCBC, and UOB. Applications open approximately 1 week before each auction and close at noon on the business day before the auction date.

Application Methods

- ATM: Select “Bonds / Bills / Shares” → “T-Bills” at any DBS/POSB, OCBC, or UOB ATM

- Internet Banking: Log in → Investments → Singapore Government Securities

- CPF-OA: Via CPF Investment Scheme (CPFIS) — submit through your bank’s CPF investment portal

- SRS: Through your SRS operator bank (DBS, OCBC, or UOB)

Non-Competitive vs Competitive Bids

Retail investors typically submit non-competitive bids. You are guaranteed full allotment at the auction’s cut-off yield, regardless of where that yield falls. Competitive bids (used mainly by institutions) specify a maximum yield — bids at or above the cut-off yield may not be fully allotted.

For most retail investors, non-competitive bids are the simpler and safer choice.

Using CPF-OA to Invest in T-Bills

One common question is whether it’s worth investing CPF Ordinary Account (OA) funds into T-bills. Here’s the key consideration:

- CPF-OA earns a guaranteed 2.50% p.a. floor rate

- The latest 6-month T-bill yields 1.40%, the 1-year T-bill yields 1.46%

- Both are below the CPF-OA floor rate — investing would reduce your returns

This means that in the current rate environment (April 2026), using CPF-OA funds for T-bills is likely not advantageous. Your CPF-OA already earns more sitting uninvested.

However, there may be tactical reasons — for example, if you expect to use the funds for a housing downpayment within the next 12 months and want the capital returned to CPF-OA in time. In that case, the slightly lower yield is an acceptable trade-off for the certainty of getting the cash back on schedule.

For SRS funds, the calculus is different — SRS earns 0.05% p.a. at the bank, making T-bills at 1.40–1.46% significantly more attractive for deployed SRS savings.

See also: CPF Investment Strategy Guide for a full breakdown of CPFIS options and when to invest your CPF-OA.

Upcoming T-Bill Auctions 2026

MAS publishes the T-bill auction calendar in advance. The 6-month T-bill is auctioned every 2 weeks (alternating Wednesdays), while the 1-year T-bill is auctioned quarterly. Check the MAS Issuance Calendar for the latest schedule.

With the 6-month T-bill now at 1.40% — down from the recent high of 1.47% (9 Apr) — the trend in early-to-mid April 2026 suggests some moderation in short-term yields. Whether this continues depends heavily on:

- US Federal Reserve rate decisions and forward guidance

- MAS monetary policy stance (SGD NEER policy)

- Demand dynamics from institutional and retail investors

- Singapore inflation and GDP outlook

For real-time yield tracking and comparison, our T-Bill, SSB & Fixed Deposit Comparison Calculator lets you model different yield scenarios for your cash allocation.

Try Our Free T-Bill Calculator

Compare T-bill, SSB, and fixed deposit yields side by side. Model your cash returns across different tenures and interest rate scenarios.

Frequently Asked Questions

What is the current Singapore T-bill yield in April 2026?

Should I choose the 6-month or 1-year T-bill?

Can I invest CPF-OA funds in Singapore T-bills?

Are Singapore T-bill returns taxable?

How do T-bills compare to Singapore Savings Bonds (SSB)?

How often are Singapore T-bill auctions held?

What happens when my T-bill matures?

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.