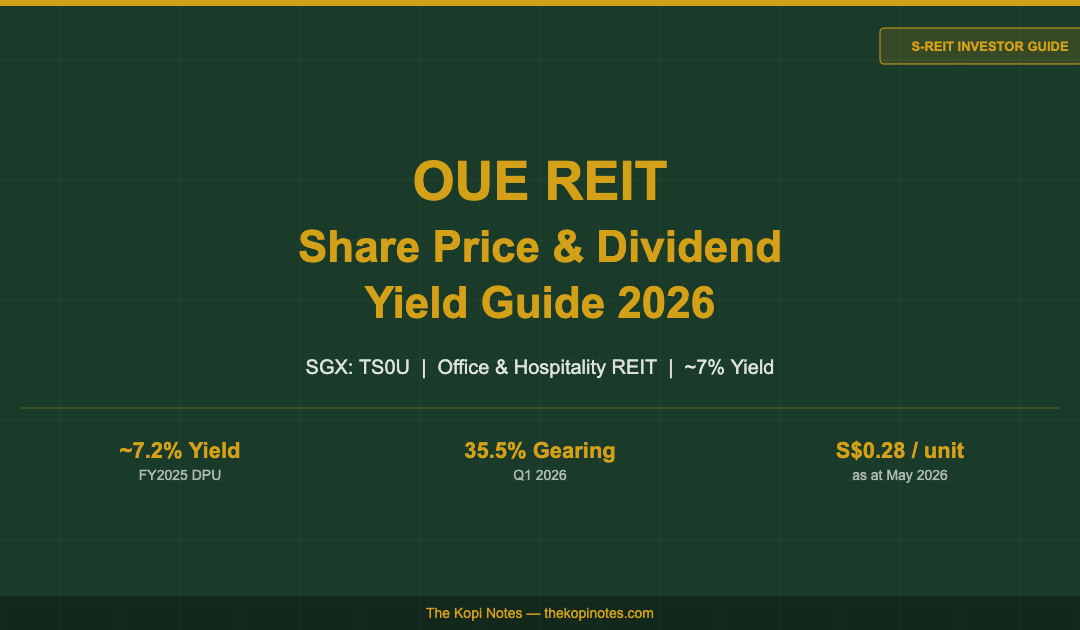

OUE REIT Share Price & Dividend Yield Guide 2026 (SGX: TS0U)

A complete Singapore investor’s guide — DPU history, dividend yield analysis, share price outlook, and 2026 data.

OUE REIT (SGX: TS0U) is a Singapore-listed REIT that owns a diversified portfolio of office and hospitality assets across Singapore, China, and Japan. As at May 2026, OUE REIT trades at approximately S$0.28 per unit, offering an indicative dividend yield of around 7.2% based on its FY2025 DPU of 2.02 Singapore cents. With a gearing ratio of 35.5% — one of the lowest among Singapore commercial REITs — OUE REIT appeals to investors seeking above-market income with a relatively conservative balance sheet.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

Table of Contents

Contents — Click to expand

What Is OUE REIT?

OUE REIT (SGX: TS0U) is a real estate investment trust listed on the Singapore Exchange. It is sponsored by OUE Limited, one of Singapore’s established property conglomerates with roots in the hospitality and commercial sectors. The REIT was listed in January 2014 and has since grown into a diversified vehicle encompassing premium office towers and upscale hotels.

Unlike single-sector S-REITs such as pure-play industrial or logistics trusts, OUE REIT straddles two property classes: commercial office space and hospitality assets. This dual-mandate structure offers some income diversification — office leases provide stable long-term cash flows, while hotels contribute variable income that tracks tourism and business travel trends.

As at Q1 2026, OUE REIT’s portfolio spans Singapore (its core market), Shanghai, and Japan, giving investors exposure to pan-Asian commercial real estate from a Singapore-regulated trust structure. Income distributions are paid semi-annually in Singapore dollars.

Key Facts at a Glance

| Metric | Detail |

|---|---|

| SGX Ticker | TS0U |

| Full Name | OUE Real Estate Investment Trust |

| Sponsor | OUE Limited (Riady Group affiliate) |

| Listing Date | January 2014 |

| Sector | Diversified (Office + Hospitality) |

| Share Price (May 2026) | ~S$0.28 per unit |

| FY2025 DPU | 2.02 Singapore cents |

| Indicative Yield (FY2025 DPU) | ~7.2% at S$0.28 |

| Gearing Ratio | 35.5% (as at Q1 2026) |

| Distribution Frequency | Semi-annual (June & December) |

| Market Capitalisation | ~S$1.3 billion (May 2026) |

Source: OUE REIT investor relations & SGX, June 2026

OUE REIT Share Price History

OUE REIT’s share price has had a volatile ride since listing, largely tracking the broader S-REIT market’s sensitivity to interest rates. The unit price peaked above S$0.50 during the low-rate environment of 2018–2019, before the COVID-19 pandemic dealt a heavy blow to its hospitality income stream. The REIT has since traded in a compressed range as investors await a sustained recovery in both office occupancy and hotel RevPAU.

| Period | Approx. Price Range | Key Driver |

|---|---|---|

| 2019 | S$0.48 – S$0.55 | Low rates, hospitality boom |

| 2020 | S$0.18 – S$0.44 | COVID crash, hotel closures |

| 2021 | S$0.26 – S$0.37 | Partial recovery, border reopening |

| 2022 | S$0.28 – S$0.38 | Rate hike cycle begins |

| 2023 | S$0.24 – S$0.34 | High rates compress valuations |

| 2024 | S$0.24 – S$0.30 | Soft office market, rate relief hopes |

| 2025–2026 YTD | S$0.26 – S$0.31 | Gradual rate cuts, hospitality recovery |

Source: SGX, OUE REIT investor relations. Prices are indicative ranges only.

At the current price of approximately S$0.28, OUE REIT trades at a meaningful discount to its reported Net Asset Value (NAV). This price-to-NAV discount is both an opportunity — high yield on entry — and a signal that the market remains cautious about the pace of Singapore CBD office recovery and OUE’s China hospitality exposure.

DPU History & Dividend Yield Analysis

OUE REIT’s DPU (distribution per unit) history reflects the dual drag of rising financing costs and the slow recovery of its hospitality segment. After paying out 3.35¢ in FY2019, distributions collapsed during COVID, and the REIT has yet to return to pre-pandemic payout levels. FY2025 DPU of 2.02¢ marked a modest recovery — up from 1.88¢ in FY2024 — driven by improving hotel RevPAU and stable office rents at OUE Bayfront.

A Singapore investor holding 100,000 units at S$0.28 per unit (a S$28,000 position) would have received approximately S$2,020 in distributions for FY2025, representing a 7.2% cash-on-cash yield — well above the S-REIT sector average of approximately 5.5–6.0% as at mid-2026.

Portfolio Overview

OUE REIT’s portfolio is anchored by two premium Singapore office towers — OUE Bayfront and OUE Downtown — alongside a cluster of hospitality assets. The office segment contributes the majority of net property income (NPI) and provides a stable, leasing-driven revenue base. The hospitality segment, which includes Hilton Singapore Orchard (1,080 rooms, one of Singapore’s largest hotels) and assets in Shanghai and Japan, adds variable income linked to tourism and corporate travel demand.

| Asset | Type | Location | NLA / Rooms | Occupancy |

|---|---|---|---|---|

| OUE Bayfront | Grade A Office | Singapore CBD | ~306,000 sq ft | ~92% |

| OUE Downtown | Grade A Office | Singapore CBD | ~569,000 sq ft | ~90% |

| Hilton Singapore Orchard | Hotel (Master Lease) | Orchard Road, SG | 1,080 rooms | N/A (master lease) |

| Crowne Plaza Changi Airport | Hotel | Changi, Singapore | 563 rooms | ~78% RevPAU |

| Mandarin Orchard Shanghai | Hotel | Shanghai, China | 507 rooms | Recovery mode |

Source: OUE REIT Q1 2026 business update & annual report. Occupancy figures are indicative.

The Hilton Singapore Orchard operates under a master lease structure, meaning OUE REIT receives a fixed base rent plus variable income tied to the hotel’s gross operating profit — providing both income floor and upside participation. Crowne Plaza Changi Airport benefits from Changi’s position as one of Asia’s busiest transit hubs, though RevPAU recovery has been gradual post-pandemic. The Shanghai asset remains a drag as China’s corporate travel recovery lags Singapore and Japan.

Financial Health & Gearing

OUE REIT’s balance sheet is one of its more attractive features. At 35.5% aggregate leverage as at Q1 2026 — well below MAS’s 50% statutory limit — the REIT has meaningful debt headroom. For context, a Singapore investor comparing OUE REIT against a higher-geared peer like Suntec REIT (gearing ~42.5%) would note that OUE’s lower leverage reduces refinancing risk and provides buffer against property devaluations.

All-in financing cost stands at approximately 3.8% as at Q1 2026, with a debt maturity profile spread across 2026–2030. Interest coverage ratio (ICR) is approximately 2.6×, above MAS’s minimum threshold of 1.5× but below the 3×+ levels typical of lower-risk S-REITs like ParkwayLife REIT. Investors should monitor ICR trends closely as the REIT’s hotel income remains variable.

On NAV: OUE REIT’s book NAV is approximately S$0.49–S$0.52 per unit as at end-2025. At a market price of S$0.28, the REIT trades at roughly 54–57 cents on the dollar — a steep discount to book that reflects investor scepticism about the China hospitality recovery and Singapore CBD office valuations. For yield-focused buyers, this discount implies that even a partial re-rating could produce meaningful capital upside alongside the 7%+ income stream. For more on evaluating S-REIT balance sheets, see the best S-REITs in Singapore 2026 guide.

OUE REIT vs Peer S-REITs

How does OUE REIT stack up against comparable Singapore REITs? The table below compares OUE REIT with six peers across yield, gearing, and sector positioning. Note that Sasseur REIT offers the highest yield but carries unique China outlet-mall risk; Keppel REIT and CICT offer lower yields but stronger institutional tenant quality.

| S-REIT | Sector | Indicative Yield | Gearing | Strength |

|---|---|---|---|---|

| OUE REIT (TS0U) | Office + Hospitality | ~7.2% | 35.5% | High yield, low gearing |

| Suntec REIT (T82U) | Office + Retail | ~6.0% | ~42.5% | SG/AU/UK diversification |

| Keppel REIT (K71U) | Office | ~5.8% | ~40.2% | Premium office, MBFC anchor |

| MPACT (N2IU) | Retail + Office | ~6.2% | ~36.5% | VivoCity anchor, pan-Asia |

| Frasers Centrepoint Trust (J69U) | Suburban Retail | ~5.6% | ~39.4% | HDB heartland malls, defensive |

| CICT (C38U) | Retail + Office | ~5.5% | ~37.8% | Largest SG REIT, highest liquidity |

| Sasseur REIT (CRPU) | China Outlet Malls | ~9.5% | ~24.5% | Highest yield, highest China risk |

Source: SGX & REIT investor relations pages, June 2026. Yields are indicative based on trailing DPU and prevailing market prices.

OUE REIT sits in the attractive middle ground — its 7.2% yield significantly exceeds the blue-chip commercial REITs (CICT at 5.5%, Keppel at 5.8%), yet its 35.5% gearing is materially lower than peers like Suntec (42.5%). The trade-off is that OUE REIT’s DPU trajectory remains uncertain, linked as it is to China hospitality recovery and Singapore Grade A office renewal rates. To explore other high-yield options, see our guide to passive income Singapore strategies.

How to Buy OUE REIT in Singapore

OUE REIT (SGX: TS0U) is available on the Singapore Exchange and can be purchased through any SGX-connected broker. It is not CPF Investment Scheme (CPFIS) approved, so investors cannot use CPF OA funds to buy OUE REIT. However, it is eligible under the Supplementary Retirement Scheme (SRS) — an attractive route for investors seeking to reduce taxable income while building a dividend-yielding portfolio.

Recommended brokers for purchasing OUE REIT:

- Interactive Brokers (IBKR) — lowest commission (~USD 1.50 minimum per trade), best for investors with larger portfolios (S$20,000+). Supports fractional-lot buying of SGX stocks.

- Syfe Brokerage — commission-free SGX trades for the first year, suitable for beginners. Use the Syfe referral code for a sign-up bonus.

- FSMOne — 0.08% commission with a S$10 minimum, CDP-linked. Ideal for investors who want direct CDP ownership of their S-REIT units. Use the FSMOne referral code P0544985 for fee savings.

- moomoo Singapore — competitive fees, good charting tools, suitable for active investors. See the moomoo Singapore review for a full breakdown.

Step-by-step buying process: (1) Open and fund your brokerage account in SGD; (2) Search for OUE REIT using ticker TS0U or the full name; (3) Check the current bid/ask spread before placing your order — OUE REIT has moderate liquidity so a limit order near the last traded price is advisable; (4) Place your buy order in board lots (1 lot = 1,000 units, ~S$280 at current prices); (5) Confirm your CDP or custodian holdings after settlement (T+2).

For a broader framework on building a dividend portfolio, the Singapore retirement calculator can help you model how OUE REIT’s distributions contribute to your income goals.

Buy, Hold or Avoid? Investor Verdict

OUE REIT is a yield play for investors with a moderate risk appetite and a multi-year time horizon. Here is how to frame the decision:

OUE REIT may suit you if: you are seeking income yield above 7% from a Singapore-regulated REIT; you are comfortable with variable hospitality income and can tolerate a 1–2 year DPU recovery timeline; you want exposure to Singapore Grade A office at a deep NAV discount; your time horizon is 3+ years.

Consider alternatives if: you need predictable, stable DPU growth (ParkwayLife REIT or AIMS APAC REIT may be better fits); you want CPF-investable S-REITs (Frasers Centrepoint Trust and CICT are CPFIS-approved); you are concerned about China hospitality risk (opt for Singapore-only REITs); you prefer higher liquidity (CICT and Keppel REIT have much higher daily trading volumes).

For investors building a diversified S-REIT income portfolio, OUE REIT can serve as a high-yield satellite position — complementing more defensive anchors like FCT or ParkwayLife. Pair it with an Endowus referral code account to access professionally managed REIT fund exposure alongside your direct SGX holdings. For a deeper look at the broader REIT universe, see our Singapore REIT ETF guide and the full S-REIT sectors Singapore 2026 comparison.

Disclaimer: This article is for educational purposes only. Investing in REITs involves risk, including the possible loss of capital. Always consult a licensed financial adviser before making investment decisions.

Frequently Asked Questions

What is OUE REIT and what does it invest in?

OUE REIT (SGX: TS0U) is a Singapore-listed diversified REIT sponsored by OUE Limited. It invests in a mix of Grade A office properties — primarily OUE Bayfront and OUE Downtown in Singapore’s CBD — and hospitality assets including Hilton Singapore Orchard (1,080 rooms), Crowne Plaza Changi Airport, and hotel properties in Shanghai and Japan. Distributions are paid semi-annually in Singapore dollars.

What is OUE REIT's current dividend yield?

Based on OUE REIT’s FY2025 DPU of 2.02 Singapore cents and a unit price of approximately S$0.28 (as at May 2026), the indicative trailing dividend yield is approximately 7.2%. This yield is higher than most Singapore commercial REITs but reflects the uncertainty in OUE REIT’s hospitality income recovery. Yield will change with both DPU and share price movements.

Can I buy OUE REIT with my CPF savings?

No. OUE REIT is not included in the CPF Investment Scheme (CPFIS) approved list, meaning you cannot use CPF OA or SA funds to purchase TS0U directly. However, OUE REIT is eligible for purchase through the Supplementary Retirement Scheme (SRS), which allows you to use SRS funds via an SRS-linked brokerage account. SRS contributions also qualify for income tax relief of up to S$15,300 per year for Singapore Citizens and PRs.

Is OUE REIT safe? What are the main risks?

OUE REIT’s key risks include: (1) China hospitality exposure — the Shanghai hotel’s recovery depends on China corporate travel, which remains uneven; (2) Singapore CBD office vacancy — if Grade A office leasing demand weakens, rental reversions could disappoint; (3) interest rate sensitivity — while gearing is moderate at 35.5%, the REIT’s financing costs remain above historical lows; (4) DPU variability — as a diversified REIT with variable hotel income, DPU is not guaranteed and has declined significantly from pre-COVID highs. As with all S-REIT investments, capital loss is possible.

Which broker is best for buying OUE REIT in Singapore?

For OUE REIT specifically, Interactive Brokers (IBKR) offers the lowest trading fees for SGX stocks, making it ideal for larger positions. Syfe Brokerage is the most beginner-friendly option with commission-free SGX trades. FSMOne (referral code P0544985) offers CDP-linked ownership at 0.08% commission with a S$10 minimum — a good choice if you want your units in your own CDP account rather than a custodian account. All three platforms support SGX board lot trading in OUE REIT (TS0U).

What is OUE REIT's gearing and is it a concern?

OUE REIT’s aggregate leverage (gearing) stands at approximately 35.5% as at Q1 2026 — comfortably below MAS’s 50% statutory limit and lower than many Singapore commercial REIT peers. This gives the trust meaningful headroom to take on additional debt for acquisitions or to weather a property valuation decline without breaching regulatory limits. That said, investors should monitor its interest coverage ratio (approximately 2.6× as at Q1 2026) given the variable nature of hotel income.

How does OUE REIT compare to Suntec REIT?

OUE REIT and Suntec REIT are both Singapore diversified commercial REITs, but they differ in several ways. OUE REIT offers a higher yield (~7.2% vs Suntec’s ~6.0%) and lower gearing (35.5% vs ~42.5%), but Suntec REIT has greater portfolio diversification across Singapore, Australia, and the UK, and significantly higher market cap and trading liquidity. Suntec REIT’s DPU has shown more consistent quarterly distributions, while OUE REIT’s semi-annual payouts have been more volatile due to its hospitality segment.

Ready to Start Investing in S-REITs?

Open a brokerage account and earn referral bonuses when you sign up through our links.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.