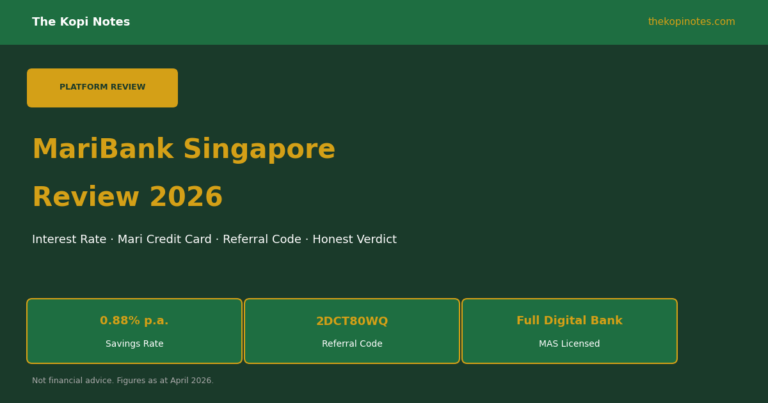

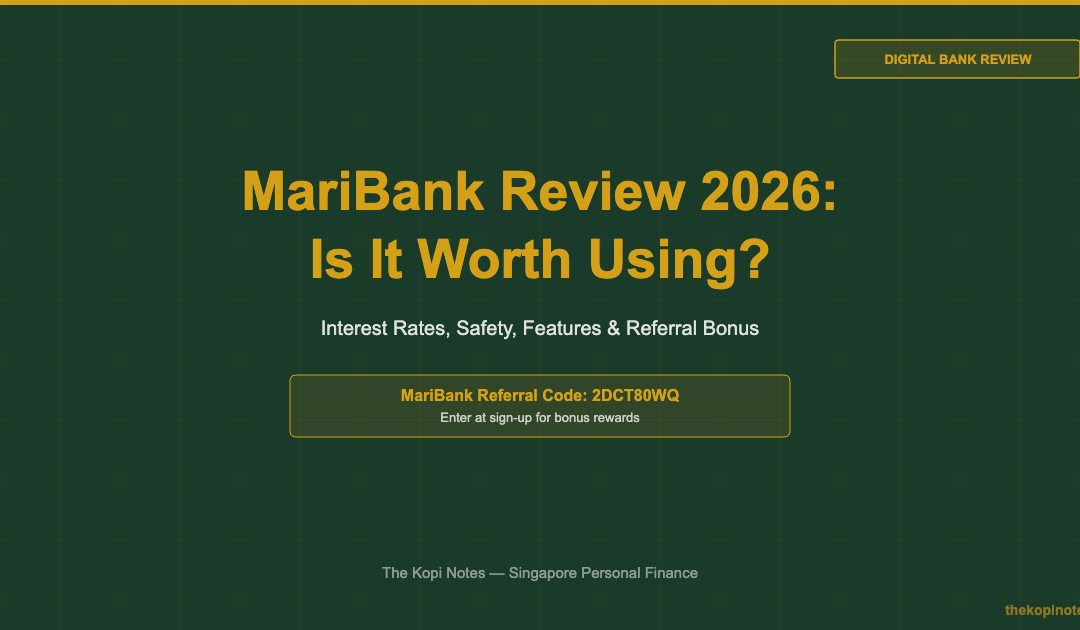

MariBank Review 2026: Is It Worth Using?

An honest, data-driven review of MariBank’s interest rates, safety, features, and whether it belongs in your Singapore banking setup.

MariBank is a fully digital bank licensed by the Monetary Authority of Singapore (MAS), owned by Sea Limited — the same group behind Shopee and Garena. It offers a savings account paying 2.68% p.a. with no minimum balance, personal loans, and a referral bonus when you sign up with code 2DCT80WQ. Your deposits are protected up to S$75,000 by the Singapore Deposit Insurance Corporation (SDIC).

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

- MariBank pays 2.68% p.a. with zero minimum balance — competitive for a no-strings account

- It is MAS-licensed and SDIC-insured up to S$75,000 — your money is safe

- Use referral code 2DCT80WQ at sign-up to unlock a bonus reward

What Is MariBank?

MariBank is one of Singapore’s newest fully digital banks. It launched in 2022 after Sea Limited — the Nasdaq-listed tech conglomerate behind Shopee and Garena — was awarded a Digital Full Bank (DFB) licence by MAS in 2020.

Unlike traditional banks such as DBS or OCBC, MariBank has no physical branches. Everything is done through the MariBank app, available on iOS and Android. You open your account online in minutes, with no paperwork and no minimum deposit required.

Sea Limited’s deep roots in Southeast Asia’s digital economy give MariBank a unique angle: it is tightly integrated with the Shopee ecosystem. If you’re a Shopee seller or frequent shopper, MariBank has specific features designed around that use case — including the ability to link your Shopee account and access seller financing.

As at June 2026, MariBank is in a full public launch and available to Singapore residents aged 18 and above with a valid Singpass.

Key Facts at a Glance

| Metric | Detail |

|---|---|

| Full Name | MariBank (Singapore) |

| Parent Company | Sea Limited (NYSE: SE) |

| MAS Licence | Digital Full Bank (DFB) |

| SDIC Protected | Yes — up to S$75,000 per depositor |

| Savings Interest Rate | 2.68% p.a. (as at June 2026) |

| Minimum Balance | S$0 |

| Fall-below Fee | None |

| Personal Loans | Yes (rates vary) |

| Referral Code | 2DCT80WQ |

| Eligibility | Singapore residents, 18+, valid Singpass |

Source: MariBank official website, June 2026

MariBank Interest Rates 2026

MariBank’s savings account currently pays 2.68% p.a. on your full balance with no strings attached. You don’t need to credit your salary, hit a minimum spend, or jump through hoops to earn this rate.

That makes it genuinely useful as a high-interest parking account. Compare this to a standard POSB or Maybank savings account paying 0.05–0.10% — the difference on a S$10,000 balance is roughly S$258 vs S$10 a year.

The catch: 2.68% is not the highest available. GXS Bank offers up to 3.00% p.a. on its FlexiDeposit, and traditional banks like OCBC 360 or UOB One can reach 4–5% if you hit their salary and spend requirements. However, those accounts require monthly salary crediting and card spend — making them unsuitable if you just want to park cash freely.

For a no-condition savings account, MariBank is among the most competitive options in Singapore as at June 2026.

MariBank Interest Rate History

| Period | Rate p.a. | Notes |

|---|---|---|

| 2022 (launch) | 2.00% | Introductory rate |

| 2023 | 2.50% | Rate increase with Fed hikes |

| 2024 | 2.65% | Peak rate environment |

| June 2026 | 2.68% | Current rate |

Source: MariBank, various announcements. Historical rates approximate.

Is MariBank Safe?

Yes — MariBank is a fully licensed bank in Singapore. It holds a Digital Full Bank (DFB) licence granted by MAS, which is the same regulatory category as traditional banks like DBS and OCBC. This is the highest tier of banking licence MAS issues.

Your deposits with MariBank are protected by the Singapore Deposit Insurance Corporation (SDIC) for up to S$75,000 per depositor. If MariBank were ever to fail (which, given its MAS oversight, is highly unlikely), you would receive your money back up to that threshold.

Being owned by Sea Limited — a publicly listed company on the New York Stock Exchange with a market cap in the tens of billions — also adds a layer of financial stability. Sea’s balance sheet is well-capitalised, and MariBank operates under MAS’s strict ongoing supervision.

The short answer: yes, MariBank is safe. It is regulated, insured, and backed by a large public company. Use it like you would any other MAS-licensed bank in Singapore, and you’re protected by the same laws.

MariBank Features: What Can You Do?

MariBank is not yet as feature-rich as full-service banks like DBS or OCBC, but it covers the essentials well:

Savings Account — Earn 2.68% p.a. on your full balance with no minimum and no salary crediting requirement. Interest is credited monthly.

Personal Loans — MariBank offers unsecured personal loans to eligible customers. Approval is done in-app, and rates are competitive for digital lenders. If you’re an existing Shopee seller, you may access MariBank’s merchant financing at preferential rates. You can learn more about loan options via the Singapore retirement calculator to model how borrowing fits your financial plan.

Debit Card — MariBank issues a Mastercard debit card for everyday spending. You can use it at any merchant that accepts Mastercard, including for online purchases.

Shopee Integration — Because of Sea’s ownership, MariBank connects natively with your Shopee account. Sellers can use it for business cash management, and buyers can link it for seamless checkout.

Fast Transfers — PayNow and FAST transfers are supported. You can send and receive money instantly from any Singapore bank.

No ATM Access — As a purely digital bank, MariBank does not have its own ATM network. Cash withdrawals are via the NETS network — but if you’re using MariBank as a savings vehicle rather than a daily transactional account, this is rarely an issue.

MariBank vs GXS Bank vs Trust Bank

Singapore now has three main digital banks: MariBank, GXS Bank (backed by Grab and Singtel), and Trust Bank (backed by Standard Chartered and FairPrice Group). Here’s how they compare:

| Feature | MariBank | GXS Bank | Trust Bank |

|---|---|---|---|

| Parent | Sea Limited | Grab + Singtel | StanChart + NTUC |

| Savings Rate | 2.68% p.a. | 3.00% p.a. | 1.50% p.a. |

| Min. Balance | S$0 | S$0 | S$0 |

| SDIC Protected | Up to S$75,000 | Up to S$75,000 | Up to S$75,000 |

| Personal Loans | Yes | Yes (Flex Loan) | Limited |

| Debit Card | Mastercard | Visa | Mastercard |

| Referral Code | 2DCT80WQ | YONG477 | HTWYQP95 |

| Ecosystem | Shopee | GrabPay | FairPrice / LinkPoints |

Source: MariBank, GXS Bank, Trust Bank websites, June 2026. Rates subject to conditions and change.

Bottom line: If you want the highest unconditional rate, GXS Bank currently edges MariBank at 3.00% p.a. But if you’re a Shopee user, MariBank makes more sense as your everyday digital bank. Trust Bank is best if you shop at NTUC FairPrice frequently, where it integrates with your LinkPoints. If you’re building a serious savings and investment strategy, consider also using a platform like Endowus referral code for cash management with higher returns through money market funds.

MariBank Referral Code 2026

When you sign up for MariBank, enter referral code 2DCT80WQ to unlock a bonus reward. The referral programme typically offers additional interest or cashback for new accounts — check the MariBank app for the latest terms.

How to use it: download the MariBank app → start the account opening process → enter the referral code when prompted during sign-up. You’ll need your Singpass to verify your identity.

If you’re also looking at other digital banks, the GXS Bank referral code is YONG477 and the Trust Bank referral code is HTWYQP95. All three are worth signing up for since there’s no minimum balance — you can spread your cash across them to capture the best rates and bonuses.

Who Should Use MariBank?

MariBank is ideal if you:

- Want a no-fuss savings account earning above 2.5% without salary crediting

- Are a Shopee user or seller who wants integrated banking

- Need a personal loan with quick in-app approval

- Want to diversify your deposits across multiple SDIC-insured banks

Consider alternatives if you:

- Can hit the conditions for OCBC 360 or UOB One — those pay 4–5% p.a. but require salary crediting and card spend

- Want the absolute highest unconditional rate — GXS Bank’s 3.00% beats MariBank’s 2.68%

- Shop primarily at NTUC FairPrice — Trust Bank integrates better with that ecosystem

- Want to invest your savings in the market — use a platform like Syfe or check the passive income Singapore guide for ideas beyond savings accounts

For most Singaporeans building a financial base, it makes sense to hold accounts at 2–3 digital banks simultaneously — MariBank for Shopee integration and solid interest, GXS for the slightly higher rate, and Trust Bank for FairPrice rewards. There’s no cost to having multiple accounts since none have fall-below fees. You might also want to compare options via the moomoo Singapore review if you’re investing alongside saving.

Disclaimer: Not financial advice. Interest rates change frequently. Always verify directly with MariBank before making decisions. Deposits are protected by SDIC up to S$75,000 per depositor per bank.

Frequently Asked Questions

What is MariBank and who owns it?

MariBank is a fully licensed digital bank in Singapore owned by Sea Limited — the technology conglomerate behind Shopee and Garena. Sea Limited was awarded a Digital Full Bank (DFB) licence by MAS in 2020, and MariBank launched in 2022. It operates entirely through a mobile app with no physical branches.

Is MariBank safe? Is my money protected?

Yes. MariBank holds a Digital Full Bank licence from MAS, Singapore’s financial regulator — the same licence category as DBS, OCBC, and UOB. All deposits are protected by the Singapore Deposit Insurance Corporation (SDIC) up to S$75,000 per depositor. This is the same protection as any major Singapore bank.

What is MariBank's interest rate in 2026?

MariBank pays 2.68% p.a. on its savings account as at June 2026. This rate applies to your full balance with no minimum and no salary crediting requirement. Interest is credited monthly. Always check the MariBank app for the latest rate as it can change.

What is the MariBank referral code for 2026?

The MariBank referral code is 2DCT80WQ. Enter this during sign-up in the MariBank app to unlock a referral reward (bonus interest or cashback — check the app for current terms). You’ll need Singpass to open the account.

How does MariBank compare to GXS Bank and Trust Bank?

All three are MAS-licensed digital banks with no minimum balance and SDIC protection. GXS Bank currently offers the highest unconditional savings rate at 3.00% p.a. MariBank pays 2.68% p.a. and has strong Shopee integration. Trust Bank pays 1.50% p.a. but offers NTUC FairPrice LinkPoints rewards. Many Singapore savers hold accounts at two or all three to maximise benefits and spread SDIC coverage.

Can I use MariBank as my main bank account?

MariBank covers the basics — savings, transfers, PayNow, and a Mastercard debit card — so it can function as your main account. However, it lacks an ATM network, fixed deposits, investment products, and some features of full-service banks. Most users keep MariBank as a secondary high-interest savings account alongside a traditional bank for their main salary account and credit card benefits.

Does MariBank offer loans?

Yes, MariBank offers personal loans to eligible Singapore residents. Loan applications are done entirely in-app. If you are a Shopee seller, MariBank also offers merchant financing at potentially preferential rates. Interest rates and approval criteria vary — check the app for current offers and eligibility requirements.

Open MariBank and Earn More on Your Savings

Sign up with referral code 2DCT80WQ for a bonus reward. While you’re at it, explore how to grow your money further.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.