MariBank Interest Rate Singapore 2026: What You Need to Know

Updated June 2026 · Digital Banks · 8 min read

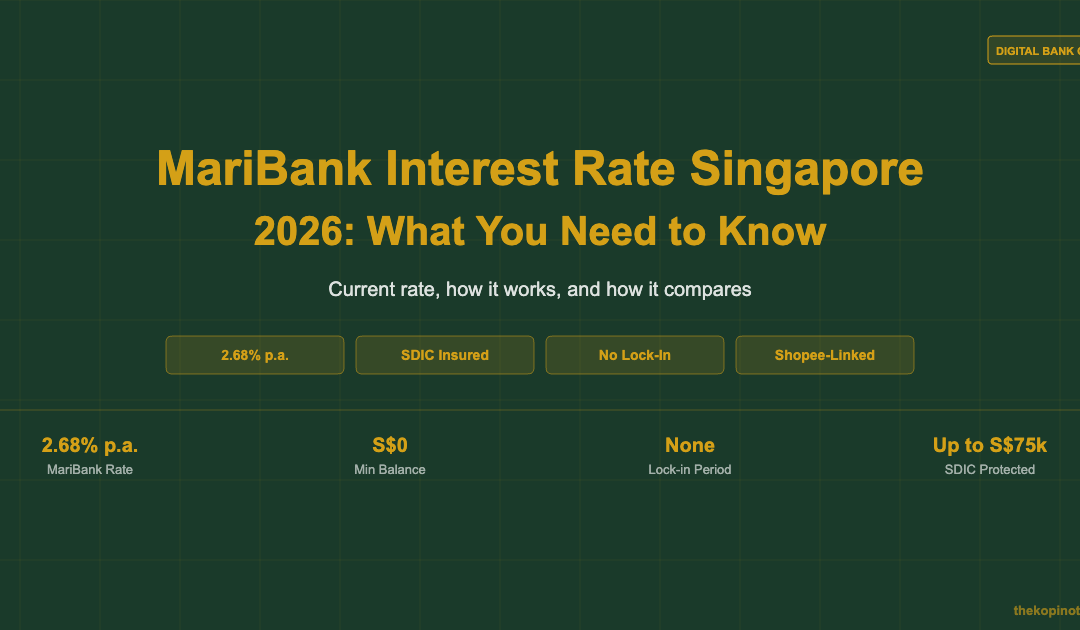

MariBank currently pays 2.68% per annum on savings — one of the highest base rates among Singapore digital banks in June 2026, with no minimum balance, no salary credit requirement, and no lock-in period. Interest accrues daily and is credited monthly. SDIC-insured up to S$75,000, MariBank is a full digital bank licence holder regulated by MAS, making it a compelling option for Singaporeans who want better returns on everyday savings without complex conditions.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

- MariBank pays 2.68% p.a. — no conditions, no minimum balance, daily accrual.

- Your deposits are SDIC-insured up to S$75,000 — same protection as a traditional bank.

- Best suited for Shopee users and those who want high-yield savings without salary crediting requirements.

📋 Table of Contents

MariBank current interest rate (June 2026)

As of June 2026, MariBank pays a base savings interest rate of 2.68% per annum. This is the headline rate — no tiering, no salary crediting condition, and no minimum balance required.

MariBank is owned by Sea Limited, the parent company of Shopee and Garena. It received a full digital bank licence from the Monetary Authority of Singapore (MAS) in 2022 and launched its savings account in 2023.

For context, traditional bank savings accounts in Singapore typically offer 0.05%–0.1% on base savings without salary crediting — more than 50 times less than MariBank’s current rate.

Has the MariBank interest rate changed recently?

MariBank adjusts its savings rate periodically in response to Singapore Overnight Rate Average (SORA) movements and competitive dynamics. The rate was higher in 2023–2024 when Singapore interest rates were elevated. As SORA has normalised in 2025–2026, MariBank’s rate has compressed slightly. The current 2.68% p.a. (June 2026) remains one of the best no-condition savings rates available to Singapore residents.

Always check the MariBank app for the current live rate — it can change without prior notice.

How MariBank interest works

Understanding how MariBank calculates and pays interest helps you maximise what you earn. Here’s the mechanics:

Daily accrual: Interest is calculated on your daily closing balance. If you deposit S$10,000 on 1 June, you start earning from that day. The formula is: (Balance × 2.68%) ÷ 365 per day.

Monthly crediting: Accrued interest is credited to your account at the end of each calendar month. You’ll see an “Interest Earned” line item in your transaction history.

Example: S$20,000 in MariBank for 12 months

At 2.68% p.a. on a S$20,000 balance:

- Monthly interest: approximately S$44.67

- Annual interest: approximately S$536

- Effective annual yield with monthly compounding: approximately 2.71% p.a.

Compare this to keeping the same S$20,000 in a traditional bank at 0.05% p.a.: you’d earn just S$10 per year. MariBank pays more than 50× that, with no conditions attached.

If you’re building a long-term savings plan, use the retirement planning calculator to model how different rates compound over time.

MariBank vs GXS Bank vs Trust Bank interest rates

Three main digital banks in Singapore compete on savings rates in 2026: MariBank, GXS Bank (backed by Grab and Singtel), and Trust Bank (backed by Standard Chartered and FairPrice Group). Here’s how they compare:

Source: GXS Bank, MariBank, Trust Bank, OCBC, DBS websites — June 2026. Base rates shown.

| Bank | Base Rate | Conditions | SDIC | Min. Balance |

|---|---|---|---|---|

| GXS Bank | 3.00% p.a. | None | ✓ Yes | S$0 |

| MariBank | 2.68% p.a. | None | ✓ Yes | S$0 |

| Trust Bank | 2.40% p.a. | None | ✓ Yes | S$0 |

| OCBC/DBS (base) | 0.05% p.a. | None (base only) | ✓ Yes | S$0 |

Source: Bank websites, June 2026.

GXS Bank pays more — so why choose MariBank?

GXS Bank’s 3.00% p.a. is higher than MariBank’s 2.68%. The gap is S$32 per year on a S$10,000 balance. From a pure rate standpoint, GXS edges ahead.

However, MariBank has a different value proposition: the Shopee ecosystem. If you shop regularly on Shopee, MariBank integrates payments, cashback, and savings in one place. MariBank also offers SpeedSend for fast transfers to Malaysian accounts — useful if you regularly send money across the Causeway.

Many Singaporeans hold accounts with multiple digital banks. For complementary low-risk savings options, the Singapore Savings Bonds guide and T-bills guide cover other options worth considering.

How much can you earn? Returns by balance

Here’s a practical breakdown showing annual interest earned at MariBank, GXS Bank, and Trust Bank at different balance levels — all calculated at June 2026 stated rates.

Source: TKN calculations at June 2026 stated rates. SDIC insurance limit is S$75,000 per depositor per bank.

SDIC deposit insurance covers up to S$75,000 per depositor per institution. GXS Bank, MariBank, and Trust Bank are separate institutions — you can hold S$75,000 in each and be fully insured. If your savings exceed S$75,000, spread them across multiple banks.

Is MariBank safe? SDIC insurance explained

MariBank holds a full digital bank licence granted by MAS in 2022 — the highest banking licence tier in Singapore, same as traditional banks like DBS or OCBC.

Your deposits are protected by the Singapore Deposit Insurance Corporation (SDIC) up to S$75,000 per depositor per bank. If MariBank were ever to fail, you’d receive up to S$75,000 back through SDIC within 21 working days.

| Protection Layer | Detail |

|---|---|

| MAS Regulation | Full digital bank licence — same tier as traditional banks |

| SDIC Insurance | Up to S$75,000 per depositor — automatically applies |

| Parent Company | Sea Limited — NYSE-listed, parent of Shopee and Garena |

| Capital Requirements | Full bank licence requires minimum S$1.5B paid-up capital under MAS framework |

Source: MAS digital bank licensing framework; SDIC Singapore. Data as at June 2026.

Short answer: yes, MariBank is safe for deposits up to S$75,000. For amounts above that, spread across multiple institutions. See the full MariBank review for a deeper look.

Any conditions to earn the full MariBank interest rate?

This is where MariBank truly stands out. To earn the full 2.68% p.a., there are zero conditions:

- No minimum balance — you earn from S$0.01 upwards.

- No salary crediting — no paycheck required.

- No minimum spend — no card spending requirement.

- No lock-in — withdraw anytime without penalty.

Compare this to traditional bank accounts: DBS Multiplier requires salary crediting plus a qualifying product; OCBC 360 requires salary crediting, saving, and spending to hit bonus tiers. MariBank’s 2.68% is available from day one, dollar one.

Is there a cap on how much earns the 2.68%?

MariBank does not publish an explicit balance cap — unlike some banks that cap bonus rates at S$50,000 or S$100,000. However, SDIC insurance only covers up to S$75,000. For balances beyond that, consider spreading across multiple institutions.

For savings beyond cash, the Endowus referral code gets you started with managed fund investing, and the Syfe referral code offers a sign-up bonus for robo-advisory portfolios.

How to open a MariBank account and start earning

Opening a MariBank account takes about 10–15 minutes via the app:

- Download the MariBank app from App Store or Google Play.

- Register using Singpass — NRIC and details pre-filled via MyInfo.

- Verify your identity — face recognition completes KYC.

- Fund your account — transfer via PayNow or FAST. No minimum needed.

- Start earning — interest accrues from the next calendar day.

Use referral code 2DCT80WQ for any available MariBank sign-up bonus. GXS Bank code YONG477 and Trust Bank code HTWYQP95 also offer bonuses if you want to open accounts with the other digital banks as well.

See the moomoo Singapore review if you’re looking to invest beyond savings, and the passive income Singapore 2026 guide for a broader strategy combining savings, REITs, and ETFs.

Disclaimer: Referral codes may earn The Kopi Notes a referral fee at no cost to you. All rates are as at June 2026 and subject to change. Not financial advice.

Frequently Asked Questions

What is MariBank's current interest rate?

Is MariBank interest rate better than GXS Bank?

How is MariBank interest calculated?

Is there a minimum balance to earn MariBank interest?

Does MariBank pay interest if you withdraw during the month?

Can Singapore PR or foreigners open a MariBank account?

Does MariBank interest get taxed in Singapore?

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. Interest rates stated are as at June 2026 and are subject to change at any time without notice. SDIC insurance covers up to S$75,000 per depositor per institution — verify current coverage at sdic.org.sg. MariBank is regulated by MAS. Referral codes may earn The Kopi Notes a referral commission at no cost to you. Always read the bank’s terms and conditions before opening an account.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.