Top Dividend Stocks in Singapore 2026: S-REITs, ETFs & Blue Chips

Your complete guide to the highest-paying dividend stocks in Singapore — with real yield data, SGD income scenarios, and step-by-step buying instructions.

Singapore’s top dividend stocks span three categories: S-REITs (yielding 5–7%), blue-chip banks like DBS and OCBC (5–6%), and dividend ETFs such as the Lion-Phillip S-REIT ETF. For most retail investors, S-REITs offer the highest yields with quarterly payouts, no capital gains tax, and strong regulatory oversight by MAS. The best picks for 2026 include CapitaLand Ascendas REIT, Mapletree Industrial Trust, and ParkwayLife REIT.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

Table of Contents

Contents — Click to expand

- Why Dividend Investing Works in Singapore

- Best S-REITs for Dividend Income 2026

- Blue-Chip Dividend Stocks: Banks & Telcos

- Dividend ETFs for Instant Diversification

- Full Comparison Table: Yields & Key Metrics

- SGD Income Scenarios by Portfolio Size

- How to Buy Dividend Stocks in Singapore

- Taxation of Dividend Income in Singapore

- Risks to Consider

- Frequently Asked Questions

Why Dividend Investing Works in Singapore

Singapore is one of the most dividend-friendly environments in the world for retail investors. There is no capital gains tax, no dividend withholding tax on locally distributed dividends, and a deep pool of high-quality income-generating assets listed on the Singapore Exchange (SGX). For investors building towards financial independence or retirement, dividend stocks offer something that growth stocks cannot: predictable, recurring cash flow that pays you while you wait.

The Singapore dividend investing landscape falls into three tiers. S-REITs — Singapore Real Estate Investment Trusts — occupy the top tier, mandated by MAS regulations to distribute at least 90% of taxable income to unitholders. This structural rule means S-REIT yields are consistently higher than most other asset classes, typically ranging from 5% to 7% as at June 2026. The second tier consists of blue-chip Singapore companies, chiefly the three local banks (DBS, OCBC, UOB) and telcos (Singtel), which have historically paid 5–6% yields supported by strong earnings. The third tier is dividend ETFs — funds that bundle multiple dividend payers into a single, diversified instrument.

Whether you are a long-term investor building a passive income Singapore portfolio, or someone approaching retirement and wanting a reliable income stream, understanding how to select the right dividend stocks is the starting point. This guide covers all three tiers with real 2026 data.

Best S-REITs for Dividend Income 2026

S-REITs are the cornerstone of any Singapore dividend portfolio. Regulated by the Monetary Authority of Singapore (MAS) and listed on SGX, they provide transparent, quarterly or semi-annual distributions backed by real property assets — offices, industrial parks, data centres, retail malls, and healthcare facilities. Unlike individual property purchases, S-REITs require no stamp duty, are highly liquid, and can be bought in small lots from as little as SGD 200–500.

Here are the standout S-REITs for dividend income in 2026:

CapitaLand Ascendas REIT (A17U)

Singapore’s largest industrial and logistics REIT, CapitaLand Ascendas REIT (CLAR) owns over 220 properties across Singapore, Australia, the US, and Europe. As at Q1 2026, its distribution per unit (DPU) yields approximately 6.1% on a trailing basis. Its diversified tenant base — spanning tech companies, pharmaceutical firms, and data centre operators — provides resilience against sector-specific downturns. CLAR is widely held as a core S-REIT holding for long-term dividend investors, and regularly features in our list of best S-REITs in Singapore 2026.

Mapletree Industrial Trust (ME8U)

Mapletree Industrial Trust (MIT) focuses on flatted factories, hi-tech buildings, and data centres in Singapore and the US. Its data centre exposure — now approximately 50% of assets by value — gives it a structural growth tailwind from AI infrastructure demand. As at Q1 2026, MIT trades at a yield of approximately 6.4%, making it one of the higher-yielding industrial REITs with a credible growth story. Its consistent DPU track record over the past decade makes it a favourite among income investors.

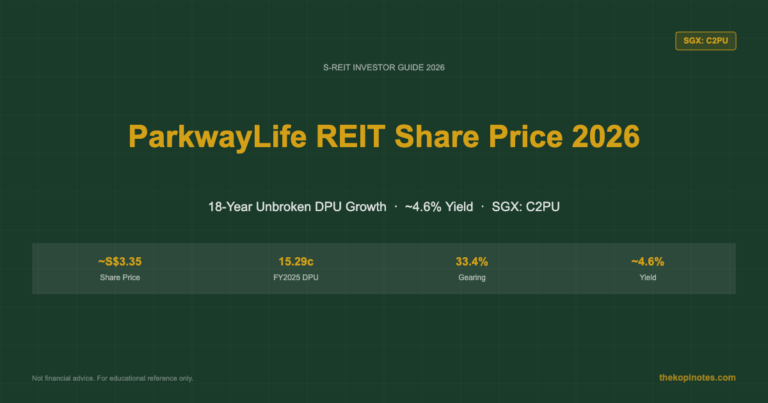

ParkwayLife REIT (C2PU)

ParkwayLife REIT (PLife) is Singapore’s largest healthcare REIT, owning private hospitals in Singapore (including Mount Elizabeth and Gleneagles) and nursing homes in Japan. Its unique defensive positioning — healthcare demand is non-cyclical — has made PLife one of the most consistent DPU growers on SGX. The yield of approximately 4.8% as at June 2026 is lower than industrial peers, but the stability and 15-year unbroken DPU growth track record justify the premium. Suitable for conservative dividend investors who prioritise safety over maximising yield.

Frasers Centrepoint Trust (J69U)

Frasers Centrepoint Trust (FCT) focuses on suburban retail malls in Singapore — Causeway Point, Northpoint City, Waterway Point, and others — serving HDB heartland communities. Singapore’s heartland retail sector has proven defensive through economic cycles because residents shop locally for daily needs. FCT’s yield of approximately 5.8% as at June 2026 is supported by near-full occupancy rates and annual rent escalation clauses built into most leases.

Keppel DC REIT (AJBU)

Keppel DC REIT is Singapore’s first pure-play data centre REIT, owning facilities across Singapore, Europe, and Asia-Pacific. As AI and cloud computing drive hyperscaler demand for colocation capacity, data centre REITs occupy a structurally advantaged position. The yield stands at approximately 5.2% as at June 2026 — lower than some industrial peers because the market prices in stronger growth prospects. Keppel DC REIT suits investors who want dividend income alongside capital appreciation potential.

Blue-Chip Dividend Stocks: Banks & Telcos

Beyond S-REITs, Singapore’s three local banks and major telco offer competitive dividend yields backed by well-regulated, profitable businesses:

| Stock | Ticker | Indicative Yield | Payout Frequency | Notes |

|---|---|---|---|---|

| DBS Group | D05 | ~5.5% | Quarterly | Largest SG bank, consistent DPS growth |

| OCBC Bank | O39 | ~5.2% | Semi-annual | Strong capital ratios, wealth management growth |

| UOB | U11 | ~5.0% | Semi-annual | ASEAN-focused, Citigroup retail integration complete |

| Singtel | Z74 | ~4.2% | Semi-annual | Turnaround story; data centre and 5G growth |

Source: SGX, company investor relations pages, June 2026. Yields are indicative based on trailing 12-month DPS and current share price.

Banks differ from S-REITs in one important respect: there is no mandatory payout ratio. Bank boards decide dividends based on earnings, capital requirements, and MAS guidance. This makes bank dividends less predictable than S-REIT distributions, though in practice DBS, OCBC, and UOB have been growing their dividends steadily since 2020. For a balanced passive income Singapore strategy, many investors combine 60–70% S-REITs with 30–40% bank stocks for sector diversification.

Dividend ETFs for Instant Diversification

If picking individual S-REITs or stocks feels too complex, dividend ETFs provide instant diversification in a single trade. Two standout options for Singapore investors in 2026:

Lion-Phillip S-REIT ETF (CLR) — Listed on SGX, this ETF tracks the Morningstar Singapore REIT Index, holding 20+ S-REITs weighted by market cap. The indicative yield as at June 2026 is approximately 5.5%, with quarterly distributions. TER is 0.60% p.a. It is Singapore’s flagship S-REIT ETF, CPF-OA investable (subject to broker eligibility), and available on most SG brokers. It is the simplest way to get broad S-REIT exposure without analysing individual REITs.

Nikko AM Singapore STI ETF (G3B) — Tracks the Straits Times Index (STI), Singapore’s benchmark 30-stock index. The yield is lower (approximately 3.5%) because the STI includes growth companies with low payout ratios, but it provides diversification across banks, REITs, and industrials. Suitable as a satellite holding rather than a core dividend play.

For a deeper comparison of dividend ETF options, see our Singapore REIT ETF guide.

Full Comparison Table: Top Dividend Stocks Singapore 2026

The table below summarises the key metrics for the top dividend stocks in Singapore as at June 2026. Use this as a starting-point checklist — always verify current yield and DPU data from company investor relations pages before investing.

| Name | Type | Ticker | Indicative Yield | Payout | CPF-OA? |

|---|---|---|---|---|---|

| CapLand Ascendas REIT | Industrial REIT | A17U | ~6.1% | Semi-annual | Yes (CPFIS) |

| Mapletree Industrial Trust | Industrial/DC REIT | ME8U | ~6.4% | Quarterly | Yes (CPFIS) |

| Frasers Centrepoint Trust | Retail REIT | J69U | ~5.8% | Semi-annual | Yes (CPFIS) |

| ParkwayLife REIT | Healthcare REIT | C2PU | ~4.8% | Quarterly | Yes (CPFIS) |

| Keppel DC REIT | Data Centre REIT | AJBU | ~5.2% | Semi-annual | Yes (CPFIS) |

| DBS Group | Bank | D05 | ~5.5% | Quarterly | Yes (CPFIS) |

| OCBC Bank | Bank | O39 | ~5.2% | Semi-annual | Yes (CPFIS) |

| Lion-Phillip S-REIT ETF | ETF | CLR | ~5.5% | Quarterly | Yes (CPFIS-OA) |

| Nikko AM STI ETF | ETF | G3B | ~3.5% | Semi-annual | Yes (CPFIS-OA) |

Source: SGX, company investor relations, Morningstar, June 2026. Yields are trailing 12-month — not a forecast. Always check the latest DPU data before investing.

SGD Income Scenarios by Portfolio Size

How much monthly passive income can a dividend portfolio realistically generate in Singapore? The table below models annual and monthly income at a blended 5.5% yield — a conservative average for a diversified S-REIT and blue-chip dividend portfolio as at June 2026. Use our Singapore retirement calculator to model how a growing dividend portfolio contributes to your retirement target.

| Portfolio Size (SGD) | Annual Dividend (5.5%) | Monthly Income | Comment |

|---|---|---|---|

| SGD 10,000 | SGD 550 | ~SGD 46 | Good starting point for beginners |

| SGD 50,000 | SGD 2,750 | ~SGD 229 | Covers basic utilities and groceries |

| SGD 100,000 | SGD 5,500 | ~SGD 458 | Meaningful supplementary income |

| SGD 200,000 | SGD 11,000 | ~SGD 917 | Close to covering average HDB household expenses |

| SGD 500,000 | SGD 27,500 | ~SGD 2,292 | Financial independence milestone for many Singaporeans |

| SGD 1,000,000 | SGD 55,000 | ~SGD 4,583 | Full retirement income replacement for most households |

Illustrative only. Assumes a constant 5.5% yield — actual yields vary by stock and change over time. Does not account for dividend reinvestment or capital changes. Not financial advice.

The key insight here is compounding. A SGD 50,000 portfolio reinvesting all dividends at 5.5% grows to approximately SGD 85,000 after 10 years — and its annual dividend output doubles alongside. This is why dividend investing rewards patience: the longer you hold and reinvest, the faster your income stream grows without adding new capital.

How to Buy Dividend Stocks in Singapore

Buying Singapore dividend stocks is straightforward once you have a brokerage account and a CDP (Central Depository) account. Here is a step-by-step overview:

Step 1: Open a Brokerage Account

For Singapore-listed stocks (all S-REITs and the three banks), you need a broker that connects to SGX. Options include:

- Syfe Trade — Simple interface, competitive commissions, no minimum account balance. Use the Syfe referral code for a sign-up bonus. Good for beginners and those wanting to start small.

- FSMOne — Commission-free for ETFs via their Regular Savings Plan (RSP), good for the Lion-Phillip S-REIT ETF. Use the FSMOne referral code when signing up.

- Interactive Brokers (IBKR) — Most cost-effective for larger portfolios (SGD 100k+), lowest commissions but more complex interface.

- Endowus — Best for CPF and SRS investing in funds; use the Endowus referral code for fee credits on your first investment.

Step 2: Open a CDP Account (for SGX stocks)

Most Singapore brokers require a CDP (Central Depository Pte Ltd) account for SGX-listed securities. Apply online via the CDP website with your SingPass. Approval typically takes 3–5 business days. ETF platforms like Syfe’s managed portfolios and Endowus hold securities in their own custody, so no CDP account is needed for those.

Step 3: Fund Your Account and Place Your Order

Singapore stocks trade in lots of 100 shares. With most S-REITs priced between SGD 1.50 and SGD 4.00 per unit, one lot costs SGD 150–400. Blue chips like DBS are priced higher (approximately SGD 33–38 per share), so one lot of DBS costs approximately SGD 3,300–3,800. ETFs like the Lion-Phillip S-REIT ETF trade from approximately SGD 0.80–1.00 per unit, making entry very accessible.

For those with CPF Ordinary Account (OA) savings, many S-REITs and the Lion-Phillip S-REIT ETF are CPFIS-approved, allowing you to invest CPF funds directly. This is a powerful feature unique to Singapore — your CPF savings can generate 5–6% dividend yield instead of the standard 2.5% OA interest rate. See our CPF investment strategy guide for details.

Taxation of Dividend Income in Singapore

Singapore’s tax treatment of dividend income is one of the most favourable in the world:

- Singapore-listed dividends (S-REITs, banks, ETFs): No dividend withholding tax for individual Singapore resident investors. Distributions from S-REITs are tax-exempt at the individual level when paid out of tax-transparent income.

- Foreign dividends: Remitted foreign dividend income is generally exempt from Singapore income tax for individuals (though this depends on the source country and treaty arrangements).

- Capital gains: Singapore has no capital gains tax. Profits from selling dividend stocks are not taxable for individual investors who are not deemed to be trading.

In short, a SGD 11,000 annual dividend income from a SGD 200,000 S-REIT portfolio is received tax-free in Singapore — a significant advantage compared to countries like the UK (20% dividend tax above £500 allowance) or Australia (dividend imputation credits needed). This tax advantage is one reason dividend investing is such a powerful wealth-building tool in Singapore.

Risks to Consider

Dividend investing is not risk-free. Key risks for Singapore dividend investors include:

- Interest rate risk: S-REITs are highly sensitive to interest rate movements. When rates rise, REIT unit prices typically fall as investors compare the yield against risk-free alternatives like Singapore T-bills (currently ~3.0–3.5% as at June 2026). Check our Singapore T-bills 2026 guide for current rates.

- DPU cuts: S-REIT distributions can be cut if occupancy falls, tenants default, or debt costs rise. The COVID-19 period (2020–2021) saw several S-REITs cut DPU by 20–40%.

- Gearing risk: S-REITs typically carry gearing (debt-to-assets) of 30–45%. MAS caps gearing at 50% — REITs approaching this limit have less financial flexibility.

- Concentration risk: Holding only 2–3 S-REITs concentrates your exposure to a single sector or geography. Diversify across industrial, retail, healthcare, and commercial sub-sectors.

- Currency risk: Some S-REITs (Mapletree Logistics Trust, Keppel DC REIT) hold significant overseas assets with income in foreign currencies. A strong SGD can reduce reported distributions.

The standard mitigation is diversification: spread holdings across 5–8 S-REITs from different sub-sectors, add blue-chip banks for sector balance, and use a dividend ETF as a diversified core holding. Never allocate more than 10–15% of your total portfolio to any single stock.

Disclaimer: The information in this article is for educational purposes only and does not constitute financial advice. Dividend yields quoted are indicative and based on publicly available data as at June 2026. Always conduct your own due diligence or consult a licensed financial adviser before making investment decisions.

Frequently Asked Questions

What are the top dividend stocks in Singapore in 2026?

The top dividend stocks in Singapore in 2026 are primarily S-REITs (Singapore Real Estate Investment Trusts), which are mandated to distribute at least 90% of taxable income. Leading picks include CapitaLand Ascendas REIT (~6.1% yield), Mapletree Industrial Trust (~6.4%), Frasers Centrepoint Trust (~5.8%), and Keppel DC REIT (~5.2%). Among blue chips, DBS Group offers approximately 5.5% yield with quarterly payouts. For diversified exposure, the Lion-Phillip S-REIT ETF provides a blended ~5.5% yield with quarterly distributions.

Are dividends from Singapore stocks tax-free?

Yes — for Singapore resident individual investors, dividends from Singapore-listed stocks (including S-REITs and the three local banks) are tax-exempt at the personal level. S-REIT distributions paid out of tax-transparent income carry no withholding tax. Singapore also has no capital gains tax, meaning profits from selling dividend stocks are not taxable for non-traders. This tax-free treatment makes Singapore one of the most attractive jurisdictions in the world for dividend investing.

Can I buy Singapore dividend stocks with CPF?

Yes. Many S-REITs and SGX-listed ETFs (including the Lion-Phillip S-REIT ETF) are approved under the CPF Investment Scheme (CPFIS-OA), allowing you to invest your CPF Ordinary Account savings in them. You can invest CPF-OA funds that exceed SGD 20,000 (the CPF-OA minimum balance that must be kept in the account). This allows your CPF savings to potentially earn 5–6% dividend yield — significantly above the standard 2.5% OA interest rate. Note: you cannot invest CPF Special Account (SA) funds in individual stocks or REITs.

How much money do I need to start dividend investing in Singapore?

You can start with as little as SGD 100–200 if you use a Regular Savings Plan (RSP) through FSMOne or a similar platform. For direct SGX stock purchases, the minimum lot size is 100 shares — for most S-REITs priced between SGD 1.50 and SGD 4.00, that means a minimum of SGD 150–400 per stock. A well-diversified portfolio of 5–6 S-REITs would require approximately SGD 2,000–5,000 to start. The dividend income at that scale is small, but the goal is to build the portfolio over time through regular contributions and dividend reinvestment.

What is the difference between dividend yield and DPU for S-REITs?

DPU (Distribution Per Unit) is the actual cash amount distributed per unit of REIT per payout period, expressed in Singapore cents. Dividend yield is the annualised DPU expressed as a percentage of the current unit price. For example, if a REIT pays a DPU of 3 cents twice a year (6 cents annualised) and its unit price is SGD 1.00, the yield is 6%. When unit prices fall, the yield rises — which is why S-REIT yields were elevated in 2023–2024 when prices were depressed by rising interest rates. Always check both figures: a high yield may reflect a falling unit price rather than a growing DPU.

Is it better to invest in individual S-REITs or the Lion-Phillip S-REIT ETF?

It depends on your time, knowledge, and portfolio size. Individual S-REITs allow you to pick higher-yielding names and avoid weaker ones, but require ongoing monitoring of DPU reports, gearing levels, and occupancy data. The Lion-Phillip S-REIT ETF (CLR) gives you instant diversification across 20+ S-REITs with a single trade — ideal for beginners or investors who prefer a hands-off approach. The ETF charges a TER of 0.60% p.a., which slightly reduces your net yield, but the diversification benefit typically justifies this for portfolios under SGD 100,000. For larger portfolios, building a curated basket of 6–8 individual S-REITs may deliver slightly better yields.

Start Building Your Dividend Portfolio Today

Open a brokerage account and buy your first Singapore dividend stock. Use our referral links for exclusive sign-up bonuses.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.