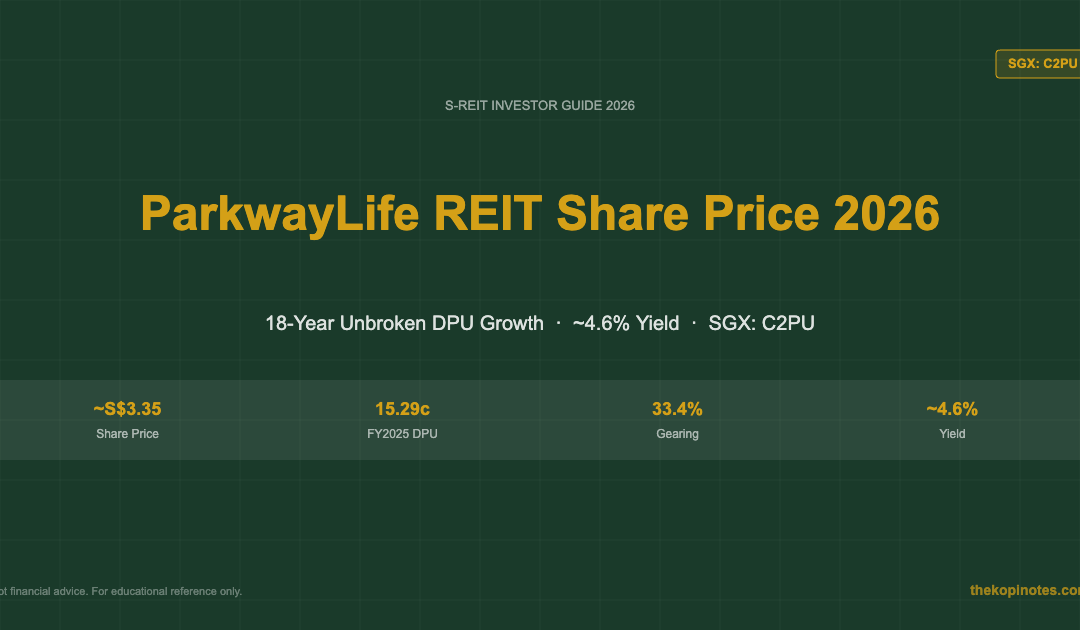

ParkwayLife REIT Share Price 2026 (SGX: C2PU): DPU History, ~4.6% Yield & Investor Guide

ParkwayLife REIT (SGX: C2PU) is Singapore’s largest listed healthcare REIT, trading at around S$3.35 in June 2026 with an indicated yield of ~4.6%. It owns 75 properties across Singapore, Japan and France — including three of Singapore’s largest private hospitals — and has delivered 18 consecutive years of DPU growth, making it one of the most defensive income investments on the SGX.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

What Is ParkwayLife REIT?

ParkwayLife REIT (SGX: C2PU) was listed on 23 August 2007 as Singapore’s first and largest listed healthcare REIT. It is sponsored by IHH Healthcare Berhad, one of Asia’s largest private healthcare groups, and focuses on income-producing healthcare and healthcare-related assets across Asia-Pacific and Europe.

As at June 2026, ParkwayLife REIT holds a portfolio of 75 properties with a total asset value of approximately S$2.3 billion, spread across three segments: three Singapore private hospitals (Mount Elizabeth, Gleneagles, Parkway East) all master-leased to Parkway Hospitals Singapore (IHH Healthcare); 71 Japanese nursing homes across Greater Tokyo, Osaka, Nagoya and other regions; and one French rehabilitation centre in Rémy acquired in November 2022.

What makes ParkwayLife REIT stand out among the best S-REITs in Singapore 2026 is its remarkable track record: it has never cut its distribution per unit (DPU) in 18 consecutive financial years since IPO, growing DPU from 6.36¢ in FY2007 to 15.29¢ in FY2025.

ParkwayLife REIT Share Price History 2019–2026

The ParkwayLife REIT share price (SGX: C2PU) has traded in a wide range over the past seven years, reflecting both the healthcare REIT premium and broader interest rate cycles.

| Period | Approx. High | Approx. Low | Year-End / Current |

|---|---|---|---|

| 2019 | S$3.84 | S$2.85 | S$3.75 |

| 2020 | S$4.60 | S$3.20 | S$4.30 |

| 2021 | S$5.04 | S$4.10 | S$4.82 |

| 2022 | S$4.82 | S$3.80 | S$4.02 |

| 2023 | S$4.20 | S$3.55 | S$3.72 |

| 2024 | S$3.98 | S$3.25 | S$3.50 |

| 2025 | S$3.70 | S$3.15 | S$3.32 |

| Jun 2026 | — | — | ~S$3.35 |

Source: SGX, Bloomberg, approximated. Past performance is not indicative of future results.

The share price decline from S$5.04 (2021 peak) to ~S$3.35 (June 2026) reflects the significant rate normalisation cycle. However, ParkwayLife REIT’s DPU has continued to grow throughout this period — meaning the underlying income strengthened even as the market price fell, resulting in a more attractive current yield for new investors.

ParkwayLife REIT DPU History & Distribution Schedule

ParkwayLife REIT pays distributions twice a year: an interim distribution (typically in August for the first half) and a final distribution (typically in March for the full year). The financial year runs from 1 January to 31 December.

The REIT’s DPU is underpinned by a unique CPI-linked rent review mechanism on its Singapore hospital master leases. Singapore rent is reviewed annually based on the greater of CPI inflation (subject to a cap) and a fixed step-up, ensuring income from Singapore properties grows in line with or above inflation. This structural protection has been the primary driver of 18 consecutive years of DPU growth — including through COVID-19 when many other REITs cut distributions.

| Financial Year | Total DPU (¢) | YoY Change | Yield @ S$3.35 |

|---|---|---|---|

| FY2019 | 13.27 | +5.9% | 4.0% |

| FY2020 | 13.94 | +5.0% | 4.2% |

| FY2021 | 14.07 | +0.9% | 4.2% |

| FY2022 | 14.39 | +2.3% | 4.3% |

| FY2023 | 14.84 | +3.1% | 4.4% |

| FY2024 | 14.92 | +0.5% | 4.5% |

| FY2025 | 15.29 | +2.5% | 4.6% |

| 1Q2026 interim | 4.42 | +15.1% | — |

Source: ParkwayLife REIT Annual Reports & SGX announcements. Yield based on ~S$3.35.

The standout metric is the 1Q2026 interim DPU of 4.42¢ (+15.1% YoY) — driven by stronger Singapore CPI-linked rent uplift and favourable JPY hedging. If sustained, FY2026 full-year DPU could reach 15.5–16.0¢, implying a forward yield of 4.6–4.8%. For income-focused investors seeking passive income in Singapore, this consistent growing income stream backed by defensive healthcare leases is the core thesis.

Portfolio Overview: Singapore, Japan & France

ParkwayLife REIT’s portfolio is concentrated in non-cyclical, needs-based healthcare assets that generate income regardless of economic conditions. The Singapore hospitals (3 properties, ~56% of gross revenue) are on master leases with Parkway Hospitals Singapore (IHH Healthcare) until at least 2042, with annual CPI-linked rent reviews. Japan (71 nursing homes, ~42%) features long-term 20–25 year triple-net leases with annual escalation clauses — positioned to benefit from Japan’s ageing demographics as the 65+ population exceeds 30% by 2030. France (1 rehabilitation centre, ~2%) diversifies into European healthcare with a 12-year lease secured at acquisition in November 2022.

Key Financial Metrics: Yield, Gearing & ICR

| Metric | Value (June 2026) | Commentary |

|---|---|---|

| Share Price | ~S$3.35 | SGX: C2PU |

| Market Cap | ~S$1.98B | ~591M units |

| FY2025 DPU | 15.29¢ | 18th consecutive year of growth |

| Trailing Yield | ~4.6% | FY2025 DPU ÷ S$3.35 |

| Aggregate Leverage | 33.4% | Well below MAS 50% cap |

| Interest Cover (ICR) | 4.9× | Above MAS 1.5× minimum |

| P/NAV | ~0.95× | Rare discount to book value |

| % Fixed-Rate Debt | ~78% | Limits interest rate sensitivity |

| Portfolio Occupancy | 99.8% | Near-full — master lease structure |

Source: ParkwayLife REIT FY2025 Annual Report, 1Q2026 business update, SGX disclosures.

At just 33.4% gearing — among the lowest of any large-cap S-REIT — ParkwayLife REIT has ~S$700M of additional debt capacity before the MAS regulatory limit. The current P/NAV of ~0.95× is unusual for a REIT that historically traded at 1.2–1.6× book, representing a rare entry opportunity for long-term investors. You can model the income compounding potential using the Singapore retirement calculator.

ParkwayLife REIT vs Peer Singapore REITs

In the context of the broader S-REIT sector in Singapore, ParkwayLife REIT occupies a unique position: lower yield but highest income quality, strongest DPU growth record, and the most defensive balance sheet.

| REIT | Code | Yield | Gearing | Sector |

|---|---|---|---|---|

| ParkwayLife REIT | C2PU | 4.6% | 33.4% | Healthcare |

| First REIT | AW9U | 7.8% | 35.5% | Healthcare (Indo) |

| CapitaLand Ascendas | A17U | 5.7% | 37.5% | Industrial |

| Mapletree Industrial | ME8U | 6.5% | 34.0% | Industrial/DC |

| Mapletree Logistics | M44U | 6.2% | 40.7% | Logistics |

| AIMS APAC REIT | O5RU | 6.9% | 26.8% | Industrial |

| Starhill Global REIT | P40U | 6.8% | 35.5% | Retail/Office |

Source: SGX, company announcements, June 2026. Yields are trailing DPU-based.

ParkwayLife REIT’s ~4.6% yield is the lowest here — but that is the price of quality. DPU has never been cut in 18 years. A Singapore investor holding S$50,000 in PLife at ~S$3.35 receives approximately S$2,300 per year in distributions — paid semi-annually, Singapore income-tax exempt.

How to Buy ParkwayLife REIT — CPF, SRS & Cash

ParkwayLife REIT is listed on the SGX Main Board and is CPFIS-OA approved. You can buy it through any SGX-authorised broker including FSMOne (referral code P0544985), Syfe Trade (code SRPRFFFCD), IBKR, or DBS Vickers. For CPF OA investing, see the CPF investment strategy guide. SRS investors can invest through FSMOne, Syfe or DBS Vickers — the SRS tax deduction effectively boosts your net yield. New to robo-advisor investing? The Endowus referral code 2V343 gives you fee credits when opening an account for SRS-eligible S-REIT access.

ParkwayLife REIT 2026 Outlook & Buy/Hold/Sell Verdict

Bull Case

Rate normalisation tailwind: Singapore T-bill yields have fallen from 3.7% (2023) to ~1.44% (June 2026). As risk-free rates fall, high-quality REITs like PLife typically see P/NAV re-rate upward. CPI-linked rent uplift: Singapore core CPI at ~2.5% in 2026 ensures another year of hospital rent growth, supporting continued DPU growth into FY2026. Japan acquisition pipeline: Management has identified additional aged-care facilities in Tier 2 Japan cities at 5–6% cap rates, immediately accretive to DPU. Rare below-NAV entry: P/NAV ~0.95× has historically been a strong entry signal for PLife investors.

Bear Case

JPY/SGD currency risk: ~42% of revenue comes from Japan. If the yen weakens further vs SGD, Japan distributions translate at lower SGD values. Management hedges ~85% of Japan income annually, but unhedged exposure remains. IHH concentration: Three Singapore hospitals (~56% of gross revenue) leased to a single IHH Healthcare subsidiary. While IHH is financially strong, concentration is a key risk factor. Lower yield trade-off: At 4.6%, PLife yields less than most peers. If rate expectations shift hawkish, the yield spread narrows again.

Verdict: BUY (Long-Term Income Investors)

For long-term income investors with a 5–10 year horizon, ParkwayLife REIT at ~S$3.35 represents compelling value. Analyst consensus (DBS, UOB Kay Hian, OCBC, Maybank) is broadly BUY with 12-month price targets of S$3.70–S$4.10, implying 10–22% total return potential from current levels including yield. The combination of 18-year unbroken DPU growth, sub-1× P/NAV, lowest-quartile gearing, and Japan demographic tailwinds makes this one of the highest-quality income assets on the SGX. This is not financial advice. Always do your own research or consult a licensed financial adviser before investing.

Start Investing in S-REITs Today

Use these platforms to buy ParkwayLife REIT or access diversified S-REIT income portfolios:

Frequently Asked Questions

What is the ParkwayLife REIT share price today?

As at June 2026, ParkwayLife REIT (SGX: C2PU) is trading at approximately S$3.35, implying a trailing yield of ~4.6% based on FY2025 DPU of 15.29¢. Check the live price on the SGX website or your brokerage app.

What is ParkwayLife REIT's DPU for FY2025?

ParkwayLife REIT distributed a total of 15.29 Singapore cents per unit for FY2025 (+2.5% over FY2024). This marks the 18th consecutive year of DPU growth since IPO in 2007. The 1Q2026 interim DPU was 4.42¢ (+15.1% YoY).

Can I buy ParkwayLife REIT using CPF?

Yes. ParkwayLife REIT is on the CPFIS Ordinary Account (OA) approved list. You can invest through CPFIS-approved brokers such as FSMOne, DBS Vickers, OCBC Securities or UOB Kay Hian. Up to 35% of your CPF investible savings (OA balance above S$20,000) can be deployed into S-REITs.

What is ParkwayLife REIT's gearing ratio?

ParkwayLife REIT’s aggregate leverage is approximately 33.4%, well below the MAS maximum of 50% and among the lowest gearing of any large-cap S-REIT. This provides ~S$700M of additional debt headroom for future acquisitions.

Is ParkwayLife REIT a good investment in 2026?

ParkwayLife REIT is widely regarded as one of the highest-quality S-REITs: 18-year unbroken DPU growth, 33.4% gearing, CPI-linked Singapore hospital leases, and a rare P/NAV of ~0.95×. Analyst consensus is broadly BUY (targets S$3.70–S$4.10). The trade-off is a lower yield (~4.6%) vs higher-yielding S-REITs. Not financial advice — do your own due diligence.

What is the difference between ParkwayLife REIT and First REIT?

Both are healthcare REITs on the SGX but very different in risk profile. PLife focuses on Singapore’s top three private hospitals and Japanese aged-care homes (developed markets, high stability, ~4.6% yield). First REIT (AW9U) focuses on Indonesian hospitals (emerging market, higher risk, ~7.8% yield). For retirement-focused investors, PLife is generally the more appropriate core holding.

How often does ParkwayLife REIT pay distributions?

ParkwayLife REIT pays distributions twice per year: an interim distribution (typically August/September) and a final distribution (typically March/April). You must hold units on the books on the record date to receive each distribution.

How does the CPI-linked rent work?

Under the master lease with Parkway Hospitals Singapore (IHH Healthcare), the annual base rent for the three Singapore hospitals is adjusted upward each year by the greater of: (1) Singapore CPI inflation for the preceding year (subject to a cap), or (2) a fixed minimum step-up. This inflation-linked structure is the primary reason PLife has grown DPU in all 18 years since IPO.

What does P/NAV below 1 mean for ParkwayLife REIT?

A P/NAV below 1.0× means the market price is lower than the accounting net asset value per unit. PLife historically traded at 1.2–1.6× NAV, so the current ~0.95× is unusually low and has historically been a strong long-term entry signal. However, NAV can change with property valuations, and a discount is not a guaranteed return trigger.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.