Tokio Marine Life Insurance Singapore 2026: Complete Review of Plans, Premiums & Is It Worth It?

TM Term Assure II, FlexiAssurance & FlexiCover compared — with real premium data and a plain-English verdict

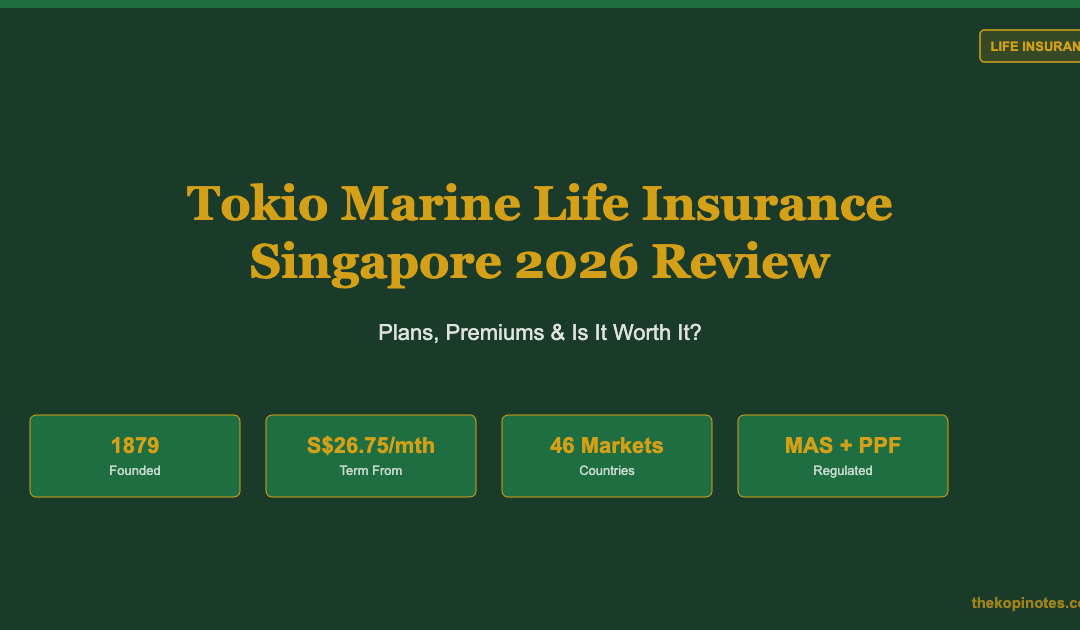

Tokio Marine Life Insurance Singapore (TMLS) is a MAS-licensed insurer with roots dating to 1879, now operating across 46 countries. In Singapore it offers four life insurance plans: TM Term Assure II (term), TM FlexiAssurance and TM FlexiCover (whole life ILP), and TM Basic Term (direct purchase with no agent). Term Assure II premiums start from S$26.75/month for a 30-year-old male non-smoker — one of the more affordable options for pure protection in Singapore.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

Table of Contents

Contents — Click to expand

- About Tokio Marine Life Insurance Singapore

- Tokio Marine Life Insurance Plans 2026

- Premiums by Age & Gender

- Pros and Cons of Tokio Marine Insurance

- Tokio Marine vs AIA vs FWD vs Singlife

- Who Should Buy Tokio Marine Life Insurance?

- How to Buy Tokio Marine Life Insurance

- Our Verdict: Is Tokio Marine Worth It?

- Frequently Asked Questions

About Tokio Marine Life Insurance Singapore

Tokio Marine Holdings Inc. is Japan’s oldest and largest non-life insurer, established in 1879 in Tokyo and listed on the Tokyo Stock Exchange as part of the Nikkei 225. Tokio Marine Life Insurance Singapore Pte. Ltd. (TMLS) is its Singapore life insurance subsidiary, regulated by the Monetary Authority of Singapore (MAS) as a Direct Insurer. TMLS is a full member of MAS’s Policy Owners’ Protection (PPF) scheme — your policy is protected up to S$500,000 in death/TPD benefits if the insurer exits the Singapore market.

Globally, Tokio Marine operates in 46 countries. In Singapore, TMLS is at Tokio Marine Centre, 20 McCallum Street #07-01, Singapore 069046, +65 6592 6100 (Mon–Fri, 8.45am–5.45pm). For those calculating their protection need, our Insurance Gap Calculator estimates your coverage shortfall in under two minutes.

Tokio Marine Life Insurance Plans 2026

Tokio Marine offers four life insurance products in Singapore spanning term and whole life categories:

1. TM Term Assure II

Tokio Marine’s flagship term life plan — pure protection paying a lump sum upon death, TPD, or Terminal Illness. No savings or investment component. Key features: coverage terms of 5-year renewable, 10-year, or 11 years up to age 85; convertible to whole life or endowment without re-underwriting; optional CI/ECI and waiver of premium riders; entry age 18–65; premiums from S$26.75/month (30M non-smoker, S$500k). The convertibility feature is valuable — if your needs change later, you can upgrade without a new health assessment.

2. TM Basic Term (Direct Purchase Insurance)

Buy directly without an adviser — no agent commission. Covers death, TPD, Terminal Illness as a lump sum. Term options: 5-year renewable, 20-year fixed, or up to age 65. Optional CI rider. MAS DPI cap: S$400,000 death + S$400,000 TPD. No savings component. Ideal for digitally-savvy buyers who know exactly what they need.

3. TM FlexiAssurance (Whole Life ILP)

A whole life investment-linked plan combining permanent life coverage with sub-fund investments. Premiums from S$125/month. Cash value accumulates and can be partially withdrawn. Important: ILP returns are not guaranteed — they depend on sub-fund performance. Always compare term life + separate investment portfolio before committing. Use our Retirement Planning Calculator to model both scenarios.

4. TM FlexiCover (Whole Life ILP)

Similar to FlexiAssurance but focused more on maximising investment returns alongside death coverage. From S$125/month. Features a unique Quit Smoking Discount — smokers who quit can apply to reduce premiums, a rare incentive in Singapore’s market. Protection/investment mix is adjustable over time.

Premiums by Age & Gender — TM Term Assure II

Indicative monthly premiums for TM Term Assure II (non-smoker, S$500,000 sum assured, 20-year level term). Actual premiums depend on health underwriting, coverage term, and any riders selected.

| Age at Entry | Male (Non-Smoker) | Female (Non-Smoker) | Male (Smoker) ~est. |

|---|---|---|---|

| 25 | ~S$22–26/mth | ~S$17–21/mth | ~S$42–50/mth |

| 30 | From S$26.75/mth | ~S$21–25/mth | ~S$52–60/mth |

| 35 | ~S$35–42/mth | ~S$28–34/mth | ~S$72–88/mth |

| 40 | ~S$55–68/mth | ~S$44–55/mth | ~S$115–138/mth |

| 45 | ~S$90–110/mth | ~S$72–88/mth | ~S$185–220/mth |

Source: Tokio Marine / MoneySmart indicative data, June 2026. Approximate for S$500k sum assured, 20-year level term. Subject to underwriting. Get a personalised quote.

Pros and Cons of Tokio Marine Life Insurance Singapore

| ✅ Pros | ❌ Cons |

|---|---|

| 137-year global track record; Japan’s oldest insurer | Smaller product range vs AIA/Prudential/Great Eastern |

| Competitive term premiums from S$26.75/mth (age 30M) | Fewer online self-service tools vs FWD/Singlife |

| DPI option (TM Basic Term) — no commission, buy direct | CI/ECI coverage available as riders only, not standalone |

| Convertibility: Term Assure II → whole life, no re-underwriting | ILP returns not guaranteed; market risk exposure |

| Quit Smoking Discount on FlexiCover — rare in Singapore | Advised plans require agent; no full online purchase |

| MAS-licensed + PPF member (death/TPD up to S$500k protected) | No Integrated Shield Plan (IP) for hospitalisation coverage |

Source: The Kopi Notes analysis, June 2026. Based on publicly available Tokio Marine product information.

Tokio Marine vs AIA vs FWD vs Singlife — Term Life Comparison

How TM Term Assure II compares to Singapore’s leading term life insurers for a 35-year-old male non-smoker, S$500,000 sum assured, 20-year term (approximate monthly premiums):

| Insurer | Plan | ~Monthly Premium | Convertible? | CI Rider? |

|---|---|---|---|---|

| Tokio Marine | TM Term Assure II | ~S$35–42 | ✅ Yes | ✅ Yes |

| FWD | FWD Term Life Plus | ~S$30–38 | ✅ Yes | ✅ Yes |

| Singlife | Singlife Term Life | ~S$32–40 | ✅ Yes | ✅ Yes |

| AIA | AIA Secure Flexi Term | ~S$38–48 | ✅ Yes | ✅ Yes |

| Manulife | ManuProtect Term | ~S$36–45 | ✅ Yes | ✅ Yes |

Source: The Kopi Notes comparative analysis, June 2026. Approximate premiums, age 35M non-smoker, S$500k, 20-year term. Get personalised quotes before purchasing.

Tokio Marine sits mid-range on pricing — slightly pricier than FWD and Singlife, competitive with AIA and Manulife. Its differentiator is convertibility and 137-year global brand heritage.

Who Should Buy Tokio Marine Life Insurance?

| Buyer Profile | Recommended Plan | Why |

|---|---|---|

| Young professional (25–35), budget-conscious, high coverage needed | TM Term Assure II or TM Basic Term | Low premiums, large sum assured, convertible later |

| DIY buyer, no agent preferred | TM Basic Term (DPI) | No commission, simpler structure, buy direct |

| Smoker planning to quit within 1–3 years | TM FlexiCover | Quit Smoking Discount reduces premiums once declared smoke-free |

| Mid-career (35–50), wants lifelong coverage + cash value | TM FlexiAssurance | Whole life + investment; cash value accessible in retirement |

Source: The Kopi Notes, June 2026. Illustrative only — consult a licensed financial adviser for personalised recommendations.

Who should look elsewhere: Need standalone multi-stage CI? Look at AIA, Manulife, or Singlife. Need an Integrated Shield Plan for hospitalisation? TMLS does not offer IP plans — consider NTUC Income, AIA HealthShield, or Prudential PruShield. Run our Insurance Gap Calculator first — LIA SG data shows the average protection gap is 3.5× annual income.

How to Buy Tokio Marine Life Insurance in Singapore

Route 1: Via a Financial Adviser (Term Assure II, FlexiAssurance, FlexiCover)

- Request a quote: Call +65 6592 6100 or visit tokiomarine.com agents page

- Financial Needs Analysis (FNA): Mandatory under MAS regulations — adviser assesses your income, dependants, existing coverage

- Plan recommendation: Adviser recommends appropriate plan and sum assured based on your FNA

- Health declaration: Complete application with medical history; severe pre-existing conditions may require full underwriting

- Policy issuance: Typically 1–2 weeks; premium payments begin on issuance date

- 14-day free look period: Cancel for a full refund within 14 days (MAS requirement)

Route 2: TM Basic Term Direct (DPI — no adviser)

- Visit the Tokio Marine life insurance page

- Select TM Basic Term under Direct Purchase Insurance

- Choose coverage amount (MAS DPI cap: S$400,000 death + S$400,000 TPD)

- Complete health declaration online and pay via credit card or GIRO

Once your protection is in place, grow your savings alongside it. Endowus (code: 2V343) gives CPF OA/SRS access to institutional funds; Syfe (code: SRPRFFFCD) offers flexible portfolio management including S-REITs and fixed income. Both complement a term life insurance strategy by building assets to close your protection gap over time.

Our Verdict: Is Tokio Marine Life Insurance Worth It in 2026?

Tokio Marine Life Insurance Singapore is a solid, reliable choice — especially for term life buyers who value global brand heritage, competitive premiums, and long-term convertibility flexibility.

TM Term Assure II — ✅ Recommended. Premiums from S$26.75/mth (age 30M), PPF-protected up to S$500k, convertible to whole life without re-underwriting. Worth getting alongside FWD and Singlife quotes.

TM Basic Term (DPI) — ✅ Recommended for experienced buyers. No commission keeps costs down; MAS DPI caps prevent over-buying. Ideal if you already know your coverage need.

TM FlexiAssurance/FlexiCover (ILP) — ⚠️ Situational. ILP returns are not guaranteed. We generally recommend comparing term + separate investments first. Use our Term Life Insurance Singapore guide to model both approaches before committing.

Overall, Tokio Marine deserves a shortlist spot when shopping for life insurance in Singapore. Always compare at least three quotes and consult a licensed financial adviser.

Not sure how much life insurance you need?

Use our free Insurance Gap Calculator — takes under 2 minutes to find your exact coverage shortfall.

Frequently Asked Questions

Is Tokio Marine a good insurance company in Singapore?

Yes. Tokio Marine Life Insurance Singapore (TMLS) is regulated by MAS as a Direct Insurer and is a member of MAS’s Policy Owners’ Protection (PPF) scheme, protecting policyholders up to S$500,000 in death/TPD benefits. The parent company was founded in 1879 and is Japan’s largest insurer, operating in 46 countries. Its long track record, financial strength, and MAS compliance make it a reliable choice for Singapore policyholders.

How much does Tokio Marine life insurance cost in Singapore?

TM Term Assure II starts from approximately S$26.75/month for a 30-year-old male non-smoker with S$500,000 coverage (20-year term). Whole life ILP plans (FlexiAssurance/FlexiCover) start from S$125/month. Actual premiums depend on age, gender, health status, smoking status, sum assured, coverage term, and riders. Request a personalised quote from a Tokio Marine adviser or via MoneySmart.

What is TM Term Assure II?

TM Term Assure II is Tokio Marine’s flagship term life insurance plan in Singapore. It pays a lump sum upon death, Total and Permanent Disability (TPD), or Terminal Illness — with no savings or investment component. Key features: flexible coverage terms (5-year, 10-year, or 11 years up to age 85), optional CI/ECI riders, and convertibility to whole life or endowment without fresh medical underwriting.

What is the difference between TM FlexiAssurance and TM FlexiCover?

Both are whole life investment-linked plans (ILPs) starting at S$125/month. FlexiAssurance balances life coverage with investment growth. FlexiCover focuses more on maximising investment returns, and uniquely offers a Quit Smoking Discount — smokers who quit can apply to reduce premiums. Both allow flexible adjustment of the protection/investment mix over time.

Can I buy Tokio Marine insurance without an agent in Singapore?

Yes. TM Basic Term is a Direct Purchase Insurance (DPI) plan — buy it without a financial adviser or agent commission. MAS DPI cap: S$400,000 death + S$400,000 TPD. Covers death, TPD, Terminal Illness with optional CI rider. Suits buyers who already know their coverage needs and want no-commission simplicity.

Does Tokio Marine offer critical illness insurance in Singapore?

Tokio Marine offers CI and early CI (ECI) as add-on riders to its life insurance plans — not standalone policies. For comprehensive standalone multi-stage CI coverage, consider AIA, Manulife, or Singlife. See our Best Critical Illness Insurance Singapore 2026 guide for a full comparison.

Is Tokio Marine covered by the PPF scheme in Singapore?

Yes. TMLS is a PPF scheme member — if it exits the Singapore market, SDIC protects your policy: up to S$500,000 in death/TPD benefits, and 100% of the first S$100,000 in surrender value plus 90% of any excess above that.

How do I contact Tokio Marine Singapore for life insurance?

Phone: +65 6592 6100 (Mon–Fri, 8.45am–5.45pm). Address: Tokio Marine Centre, 20 McCallum Street #07-01, Singapore 069046. Online: policyholders log in at mypolicy.tokiomarine-life.sg using SingPass. Find agents at tokiomarine.com/sg/en/life/agents.html.

Should I choose Tokio Marine, FWD, or Singlife for term life insurance?

All three are strong choices. FWD and Singlife typically price slightly lower and have excellent digital experiences. Tokio Marine’s advantages: 137-year global track record, convertibility to whole life without re-underwriting, and MAS PPF-backed stability. Get quotes from all three plus one more insurer, then compare against your coverage needs, budget, and goals. Always consult a licensed financial adviser for a proper Financial Needs Analysis.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Life insurance products involve complex terms — always read the product summary and speak to a licensed financial adviser before purchasing. The Kopi Notes may earn referral fees from platforms linked above. All data as at June 2026.

Related reads: Term Life Insurance Singapore 2026 | Best Critical Illness Insurance 2026 | Disability Income Insurance Guide | Insurance Gap Calculator

Get Free Insurance Advice

Speak with a licensed insurance advisor. No obligation, no cost.

By submitting this form, you agree to our Privacy Policy.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.