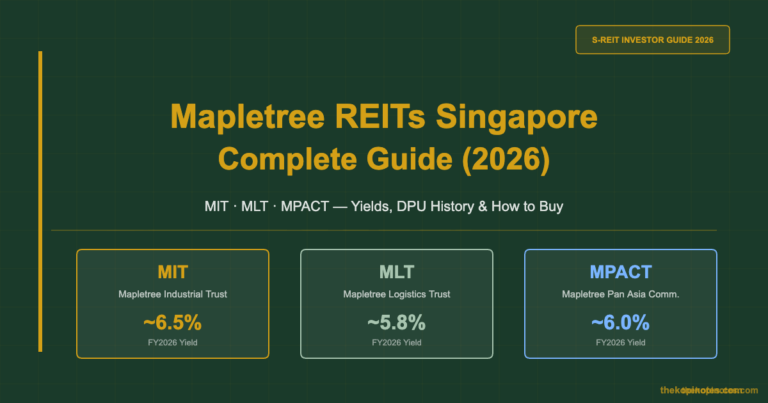

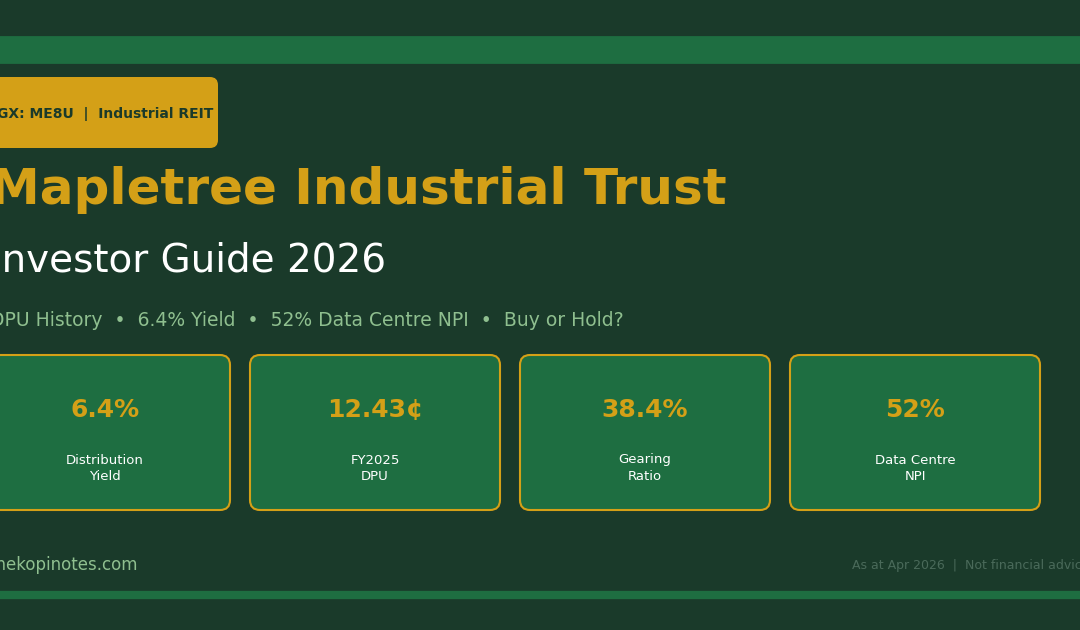

Mapletree Industrial Trust (ME8U) Investor Guide 2026

DPU History, 6.4% Yield, Data Centre Deep-Dive & Buy or Hold Analysis for Singapore Investors

Mapletree Industrial Trust (SGX: ME8U) is Singapore’s largest industrial S-REIT by market capitalisation, and one of the few Singapore-listed REITs with over half its net property income (NPI) generated by data centres. As at April 2026, ME8U offers a distribution yield of approximately 6.4% on a trailing basis — attractive relative to benchmark SGS 10-year bond yields of around 2.9%, giving a yield spread of roughly 350 basis points.

This is not financial advice. All data referenced is as at April 2026. Always conduct your own due diligence before investing.

Table of Contents

Contents — Click to expand

- What Is Mapletree Industrial Trust?

- Portfolio Breakdown: Data Centres, Factories & Hi-Tech Buildings

- DPU History FY2020–FY2025

- Distribution Yield & Peer Comparison

- Gearing Ratio & Interest Coverage

- The Data Centre Thesis: Why MIT Stands Out

- Key Risks for MIT Investors

- Buy, Hold or Wait? Investment Analysis 2026

- How to Invest in MIT via Syfe or Endowus

- FAQ: Frequently Asked Questions

What Is Mapletree Industrial Trust?

Mapletree Industrial Trust (MIT) was listed on the SGX mainboard in October 2010 and is managed by Mapletree Industrial Trust Management Ltd, a wholly-owned subsidiary of Mapletree Investments (a Temasek-backed group). The REIT owns and invests in a diversified portfolio of industrial real estate assets in Singapore and the United States.

Unlike traditional flatted-factory industrial REITs, MIT has undergone a structural transformation over the past decade — shifting its portfolio mix aggressively towards data centres, which now account for over 50% of NPI. This positions MIT as a hybrid industrial-and-digital-infrastructure play, appealing to investors seeking both yield stability and exposure to AI/cloud demand tailwinds.

Key Facts at a Glance (as at April 2026)

| Metric | Value |

|---|---|

| SGX Ticker | ME8U |

| Market Cap | ~S$6.1 billion |

| Unit Price (Apr 2026) | ~S$2.00–2.10 |

| FY2025 DPU | 12.43 Singapore cents |

| Distribution Yield | ~6.4% (trailing) |

| Number of Properties | 141 properties (SG + US) |

| Total AUM | ~S$9.0 billion |

| Gearing Ratio | 38.4% |

| Data Centre NPI Share | ~52% |

| Distribution Frequency | Semi-annual (March & September) |

| Sponsor | Mapletree Investments Pte Ltd |

Portfolio Breakdown: Data Centres, Factories & Hi-Tech Buildings

MIT’s portfolio spans 141 properties across Singapore and the United States. The portfolio is broadly classified into five asset types:

| Asset Type | No. of Properties | Share of NPI | Key Locations |

|---|---|---|---|

| Data Centres (SG) | 5 | ~24% | Tukang Innovation Drive, Seng Kang |

| Data Centres (US) | 59 | ~28% | Northern Virginia, Texas, Oregon |

| Hi-Tech Buildings | 6 | ~16% | 1 Tuas Avenue 1, 18 Tai Seng |

| Business Park Buildings | 5 | ~8% | Mapletree Business City (MBC) |

| Flatted Factories & Stack-up | 66 | ~24% | Woodlands, Tuas, Ubi |

The 59 US data centres (acquired from Equinix in 2020 and expanded subsequently) are the most significant growth driver. These colocation facilities serve hyperscale cloud tenants and benefit from long weighted average lease expiry (WALE) — typically 5–9 years — providing reliable recurring income.

MIT’s WALE for its overall portfolio stands at approximately 5.6 years as at FY2025, which is above-average for Singapore industrial REITs and signals lower near-term renewal risk.

DPU History FY2020–FY2025

MIT distributes income on a semi-annual basis. Its distribution per unit (DPU) grew steadily from FY2020 through FY2023 as the US data centre portfolio was integrated, before moderating in FY2024 and FY2025 due to the higher interest rate environment and Singapore dollar appreciation against the USD.

| Financial Year | Total DPU (S¢) | YoY Change | Key Driver |

|---|---|---|---|

| FY2020 | 11.67¢ | — | Pandemic base; SG factories stable |

| FY2021 | 12.15¢ | +4.1% | US data centre contribution ramps |

| FY2022 | 13.60¢ | +11.9% | Full year of 59 US DC income |

| FY2023 | 13.80¢ | +1.5% | Occupancy gains; rate headwinds start |

| FY2024 | 13.40¢ | -2.9% | Higher borrowing costs; USD/SGD drag |

| FY2025 | 12.43¢ | -7.2% | Refinancing at higher rates; asset recycling |

The FY2025 DPU of 12.43 cents represents a decline from the FY2023 peak. However, with Singapore SORA rates declining from their 3.0%+ peak towards current levels (~1.1%), MIT’s floating-rate borrowings are beginning to reprice downward — a tailwind for DPU recovery in FY2026 and beyond. For more context on how rate movements affect REITs, see our SORA rate and S-REIT guide.

Distribution Yield & Peer Comparison

At a unit price of approximately S$2.05 and trailing DPU of 12.43 cents, MIT offers a distribution yield of ~6.4% as at April 2026. This sits in the middle of the industrial S-REIT peer group:

| REIT | SGX Code | Trailing Yield | Asset Focus | Gearing |

|---|---|---|---|---|

| Keppel DC REIT | AJBU | 4.9% | Pure data centres | 35% |

| Mapletree Industrial Trust | ME8U | 6.4% | Industrial + Data Centres | 38.4% |

| CapitaLand Ascendas REIT | A17U | 5.7% | Diversified industrial | 37% |

| AIMS APAC REIT | O5RU | 7.6% | Industrial (SG+AU) | 33% |

| Sabana Industrial REIT | M1GU | 8.1% | Industrial (SG) | 29% |

MIT’s yield premium over Keppel DC REIT (~150 bps) reflects MIT’s broader risk profile (legacy flatted factories, higher gearing vs KDCREIT) and its larger size. Relative to CapitaLand Ascendas REIT, MIT offers ~70 bps additional yield with comparable asset quality — arguably representing fair-to-attractive value. You can use our S-REIT dividend yield calculator to model your own entry scenarios.

For context on how yield spreads work, see the distribution yield vs dividend yield glossary page.

Gearing Ratio & Interest Coverage

MIT’s aggregate leverage ratio (gearing) stood at 38.4% as at FY2025 — comfortably below the MAS regulatory limit of 50%, and with a 15% equity fundraising headroom before hitting 45% (the level at which the 10% ICR requirement applies). This provides management with meaningful debt capacity for future acquisitions or development projects.

The interest coverage ratio (ICR) was approximately 3.6x for FY2025 — above the MAS minimum of 1.5x for the 50% leverage limit, though it has compressed from the 4.5x+ levels seen during the low-rate era of FY2021–FY2022. As SORA rates decline, refinancing at lower rates should support ICR recovery over FY2026–FY2027. See our S-REIT gearing ratio & ICR calculator for your own scenario modelling.

| Metric | FY2023 | FY2024 | FY2025 | Commentary |

|---|---|---|---|---|

| Gearing Ratio | 37.1% | 38.0% | 38.4% | Gradual uptick; still comfortable |

| ICR | 4.2x | 3.9x | 3.6x | Rate pressure; recovery expected FY26 |

| All-in Debt Cost | 2.8% | 3.4% | 3.6% | Higher rates on refinanced tranches |

| Fixed-Rate Debt % | 74% | 72% | 70% | Slight increase in floating exposure |

| Debt Maturity (WADE) | 4.1 yrs | 3.8 yrs | 3.5 yrs | Well-laddered; no near-term cliff risk |

With ~70% of debt on fixed rates, MIT has limited short-term sensitivity to rate fluctuations. The remaining 30% floating-rate exposure does benefit from the SORA decline cycle underway since late 2024.

The Data Centre Thesis: Why MIT Stands Out

MIT’s most differentiating characteristic among Singapore industrial REITs is its ~52% NPI exposure to data centres — the highest of any SGX-listed industrial REIT. This is a structural advantage in an environment where AI workloads, cloud migration and digital infrastructure investment are accelerating globally.

The 59 US data centres (located across hyperscale corridors in Northern Virginia, Silicon Valley, Dallas/Fort Worth, Chicago and Seattle) benefit from:

- Long-term triple-net leases with investment-grade tenants (hyperscalers, colocation providers)

- Inflation-linked rent escalation of 1–3% per annum embedded in most leases

- High barriers to entry — power constraints, permitting delays and specialised fit-outs create natural moats

- Low capex burden on the REIT — tenants are responsible for fit-out and equipment maintenance

In Singapore, MIT’s five data centres at locations including Tukang Innovation Drive and Seng Kang are fully occupied and serve local enterprise and government clients. Singapore’s data sovereignty push (Infocomm Media Development Authority’s data residency requirements) provides structural occupancy support.

Compare this with Keppel DC REIT, which is a pure-play data centre REIT but trades at a lower yield (4.9%) and higher valuation multiple — suggesting the market ascribes a premium to pure-plays. MIT’s hybrid model offers data centre upside at an industrial REIT valuation, which many long-term investors consider a structural discount opportunity.

For a broader view of data centre exposure in Singapore REITs, see our data centre ETF Singapore guide and best S-REITs Singapore 2026 comparison article.

Key Risks for MIT Investors

Like all S-REITs, Mapletree Industrial Trust carries specific risks that investors should understand before committing capital.

1. USD/SGD Currency Risk

With ~52% of NPI derived from US-based data centres, MIT has significant USD income exposure. When the SGD strengthens against the USD, DPU in Singapore cents is eroded. MIT hedges a portion of this exposure but does not hedge it entirely. In FY2024 and FY2025, USD weakness contributed to DPU compression. Investors should factor their own SGD/USD view into their assessment.

2. Interest Rate Sensitivity

While 70% of debt is on fixed rates, the remaining 30% floats. Moreover, maturing fixed-rate debt must be refinanced — at current market rates that are still higher than the rates locked in during 2019–2021. All-in debt costs will likely remain above 3.5% for FY2026, constraining free cash flow for distributions. The trajectory of SORA and US Fed Funds rate matters significantly for MIT’s DPU outlook.

3. Flatted Factory Vacancy

MIT’s legacy Singapore flatted factories and stack-up buildings face headwinds from industrial-to-residential rezoning and tenant upgrading. While these assets contribute less than 25% of NPI, vacancy spikes in individual estates can create headline noise. Occupancy across the SG industrial portfolio was ~91% as at FY2025 — adequate, but worth monitoring quarterly.

4. US Tariff & Trade Policy Risk

US-based data centres are denominated in USD and serve predominantly US-based hyperscale tenants — so direct tariff impact is minimal. However, broader trade tensions affecting US tech sector capex could slow the pace of data centre expansions and reduce leasing velocity. For more on this, see our Singapore REIT tariff impact guide.

5. Concentration in Data Centre Tenants

MIT’s top 5 US data centre tenants likely account for a significant proportion of DC income. While these are investment-grade counterparties, concentration risk means any strategic shift by a major tenant (e.g., build-to-own) could disrupt occupancy at affected campuses. Diversification across 59 properties mitigates this but does not eliminate it.

Buy, Hold or Wait? Investment Analysis 2026

MIT’s investment case in 2026 rests on three key dynamics: (1) data centre structural growth, (2) rate cycle turning in its favour, and (3) unit price still trading at a discount to book value (P/B ~0.9x as at April 2026 — well below the sector average of 1.0–1.1x for large-cap industrial REITs).

Bull Case: MIT Is a Rate-Cycle & AI Recovery Play

If SORA continues its decline trajectory and stabilises below 1.5% through 2026, MIT’s DPU should recover towards 12.8–13.2 cents by FY2027, implying a forward yield of 6.2–6.4% at current prices — while the unit price itself could re-rate toward book value (~S$2.25), providing 7–10% capital appreciation on top of the dividend. Total return potential: 13–17% over 18 months on a base case.

Bear Case: Continued USD Weakness Erodes DPU

If the USD weakens materially against SGD (e.g., SGD/USD moves from 0.74 to 0.70), combined with higher-for-longer US rates causing debt cost pressure, MIT’s DPU could drift towards 11.5–12.0 cents — compressing the yield below 6% at current prices and potentially prompting a re-rating downward. Downside scenario: unit price at S$1.85–1.90 (-7 to -10%).

Verdict

For long-term Singapore income investors, MIT at ~6.4% yield and 0.9x P/B offers a reasonable risk-reward entry point in April 2026. The data centre transformation is largely complete; the remaining catalyst is the rate environment. Investors who want dedicated data centre exposure at MIT’s discount valuation should consider accumulating on weakness toward S$1.95–2.00 support levels. Those who prefer purer exposure might compare with Keppel DC REIT. For a broader yield comparison across S-REITs, see our best S-REITs 2026 guide.

Use our S-REIT yield vs bond spread calculator to model your own entry price scenarios.

How to Invest in MIT via Syfe or Endowus

Singapore retail investors can buy MIT (ME8U) directly through SGX-connected brokerages such as DBS Vickers, OCBC Securities, UOB Kay Hian, or moomoo Singapore. For investors who prefer managed REIT exposure, the following platforms offer S-REIT portfolio solutions:

- Syfe REIT+ — a curated S-REIT portfolio that typically includes MIT, CapitaLand Ascendas REIT, Keppel DC REIT and other top-10 S-REITs by market cap. Minimum investment: S$1. Use our Syfe referral code for fee rebates.

- Endowus Income Portfolio — includes S-REITs as part of a diversified income strategy via CPF, SRS or cash. Use our Endowus referral code for S$20 off advisory fees.

- FSMOne — allows regular savings plans and lump-sum purchases in S-REITs including ME8U. See our FSMOne referral guide.

If you’re investing via CPF-OA, MIT is on the CPF Investment Scheme (CPFIS) approved list, making it accessible with CPF savings. See our CPF investment strategy guide for how to approach CPFIS S-REIT investing.

FAQ: Frequently Asked Questions About Mapletree Industrial Trust

What does Mapletree Industrial Trust invest in?

Mapletree Industrial Trust (SGX: ME8U) invests in industrial real estate in Singapore and the United States. Its portfolio includes flatted factories, hi-tech buildings, business park buildings, and — most significantly — data centres. As at FY2025, data centres account for approximately 52% of the REIT’s net property income (NPI), making MIT a hybrid industrial-and-digital-infrastructure play.

What is MIT's distribution yield in 2026?

As at April 2026, Mapletree Industrial Trust offers a trailing distribution yield of approximately 6.4%, based on an FY2025 DPU of 12.43 Singapore cents and a unit price of around S$2.05. Distributions are paid semi-annually, typically in March and September each year. Yield will vary with unit price movements.

Is MIT a safe dividend REIT to invest in?

MIT is one of Singapore’s largest and most established industrial REITs, backed by the Temasek-linked Mapletree Investments sponsor. It has a well-diversified portfolio of 141 properties and a comfortable gearing ratio of 38.4% — well below the MAS 50% regulatory cap. That said, all REITs carry risks including interest rate sensitivity, currency risk (USD/SGD for US data centres), and occupancy fluctuations. This is not financial advice; investors should assess their own risk tolerance.

How does MIT compare to Keppel DC REIT?

Both MIT and Keppel DC REIT have significant data centre exposure, but they differ in key ways. Keppel DC REIT is a pure-play data centre REIT (100% data centres) and trades at a lower yield (~4.9%) and higher price-to-book (~1.1x). MIT is a hybrid industrial + data centre REIT, offering a higher yield (~6.4%) but also carrying legacy flatted factory assets and greater USD/SGD currency exposure. Investors seeking the purest data centre play pay a premium with KDCREIT; those comfortable with the hybrid model may find MIT’s discount valuation attractive.

Can I invest in MIT via CPF?

Yes. Mapletree Industrial Trust (ME8U) is on the CPF Investment Scheme (CPFIS) Included List, which means Singapore investors can use their CPF Ordinary Account (OA) savings to buy MIT units through approved CPFIS operators such as DBS Vickers, OCBC Securities or UOB Kay Hian. Note that CPF interest rate (currently 2.5% for OA) is the opportunity cost — only invest CPF if you believe MIT will return more than 2.5% per annum over your investment horizon. See our CPF investment strategy guide.

What is Mapletree Business City?

Mapletree Business City (MBC) is a large integrated business park development in the Pasir Panjang area of Singapore, owned by Mapletree Investments. MBC I and MBC II are business park buildings within MIT’s portfolio, contributing to approximately 8% of the REIT’s NPI. Notable tenants include major multinational corporations and tech firms. MBC is distinct from Mapletree Pan Asia Commercial Trust (MPACT), which owns VivoCity and office assets.

When does MIT pay dividends?

Mapletree Industrial Trust distributes income semi-annually. Distributions are typically declared after the results for the six-month periods ending September 30 and March 31. Payment is usually made approximately one month after the record date. Check the SGX announcements page or MIT’s investor relations website for the latest distribution schedule and record dates.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. All data is as at April 2026 unless stated otherwise. Past DPU is not indicative of future distributions. Always conduct your own due diligence and consult a licensed financial adviser before making investment decisions. thekopinotes.com is not affiliated with Mapletree Investments or any of the companies mentioned.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.