Singapore REIT Tariff Impact 2026: Which Sectors Are Most Resilient?

A comprehensive analysis of how US tariffs affect S-REITs by sector — with yield comparison tables, resilience scores, and key picks for Singapore investors.

The return of US tariffs in 2025–2026 has rattled global equity markets — but Singapore REITs (S-REITs) have largely held steady. As a property-based asset class, S-REITs are structurally insulated from direct trade disruption. But that doesn’t mean all S-REITs are equally resilient. Logistics REITs with China exposure, overseas commercial REITs, and hospitality trusts face different risk profiles compared to domestic retail and data centre REITs.

This guide breaks down the Singapore REIT tariff impact by sub-sector, provides a yield comparison table (as at April 2026), and helps you identify which S-REITs offer the best risk-adjusted income in today’s macro environment. This is not financial advice.

Table of Contents

Contents — Click to expand

- Why S-REITs Are Structurally Resilient to Tariffs

- Tariff Impact by S-REIT Sub-Sector

- S-REIT Yield Comparison Table (April 2026)

- Data Centre REITs: Lowest Tariff Risk, Strong Growth

- Industrial & Logistics REITs: Moderate Risk, High Yield

- Retail REITs: Defensive Domestic Income

- Office REITs: Improving but Selective

- Hospitality REITs: Most Cyclical, Watch Closely

- Overseas Commercial REITs: Higher Yield, Higher Risk

- Investor Strategy: How to Position Your S-REIT Portfolio

- Frequently Asked Questions

Why S-REITs Are Structurally Resilient to Tariffs

Unlike manufacturing companies or exporters, S-REITs earn income from lease rentals on physical properties — not from selling goods across borders. This means US tariffs have no direct impact on S-REIT revenue. A logistics REIT’s rental income doesn’t shrink because a tariff is imposed on goods moving through its warehouse; it only feels secondary pressure if tenants reduce their warehouse footprint in response to slower trade volumes.

Singapore also holds a structural advantage: the US applied a 10% tariff on Singapore imports — the lowest effective rate within the ASEAN-6 bloc (vs. 24–46% for Malaysia, Indonesia, Thailand, Vietnam, and the Philippines). This makes Singapore a relatively attractive base for regional manufacturers and logistics operators, potentially benefiting industrial and logistics REITs over the medium term.

Key resilience factors for S-REITs in a tariff environment:

- Long lease structures — Most S-REIT leases run 3–5 years with built-in rental escalation clauses, providing income visibility regardless of short-term macro noise.

- Strong Singapore dollar — SGD stability reduces currency risk for S-REITs with predominantly local assets.

- CPF-eligible investments — Many S-REITs are CPF-OA investible, giving them a captive domestic investor base that stabilises unit prices.

- MAS-regulated framework — MAS caps gearing at 50% (with ICR requirements), limiting the leverage risk that amplified losses in other REIT markets.

As at April 2026, the S-REIT sector trades at approximately 0.87x Price-to-NAV with an average forward distribution yield of ~5.4%, representing a spread of approximately 215 basis points over the 10-year Singapore Government Securities (SGS) bond yield. This spread is above historical averages, suggesting the market is pricing in risk that may be overstated for domestically-anchored REITs.

Tariff Impact by S-REIT Sub-Sector

Not all S-REITs are equal when it comes to tariff resilience. Here is a sector-by-sector breakdown of how US trade policy affects each sub-sector’s income, occupancy, and growth outlook.

| Sub-Sector | Tariff Risk | Approx. Yield | Key Driver |

|---|---|---|---|

| Data Centre | LOW | ~5–6% | AI demand drives record rental reversions; no trade dependency |

| Retail (Singapore) | LOW | ~5.5–6.5% | Suburban malls with necessity tenants; high occupancy costs coverage |

| Industrial (SG-anchored) | LOW–MED | ~6–7% | Supply chain reconfiguration benefits SG; some China exposure risk |

| Office (CBD) | LOW | ~5–6% | Leasing activity picking up; vacancy near peak; financial tenants stable |

| Logistics (cross-border) | MEDIUM | ~6.5–7.5% | China-linked trade volumes at risk; e-commerce provides buffer |

| Hospitality | MEDIUM | ~6–7% | Tourism sentiment-driven; most cyclical sub-sector; master leases help |

| Overseas Commercial | HIGH | ~8–10% | Currency and geopolitical risk; high yield compensates but priced-in risk |

S-REIT sector yield comparison and tariff risk rating — April 2026. Not financial advice.

S-REIT Yield Comparison Table (April 2026)

The table below compares the approximate forward distribution yields for major S-REITs as at April 2026. Yields are calculated based on trailing DPU and prevailing unit prices — they change daily and are not guaranteed. Always verify with the latest SGX filings before investing.

| REIT (SGX) | Sub-Sector | Approx. Yield | Gearing | Tariff Risk |

|---|---|---|---|---|

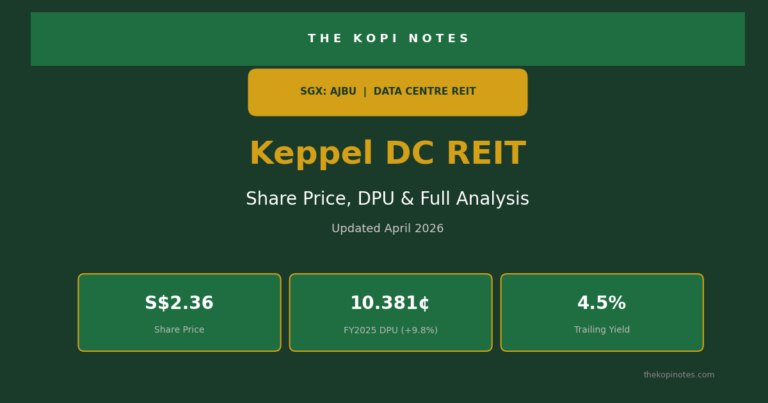

| Keppel DC REIT (AJBU) | Data Centre | ~5.2% | ~37% | LOW |

| CapitaLand Ascendas REIT (A17U) | Industrial/DC | ~6.2% | ~38% | LOW |

| Mapletree Industrial Trust (ME8U) | Industrial/DC | ~6.5% | ~40% | LOW |

| Frasers Centrepoint Trust (J69U) | Retail (SG) | ~5.8% | ~39% | LOW |

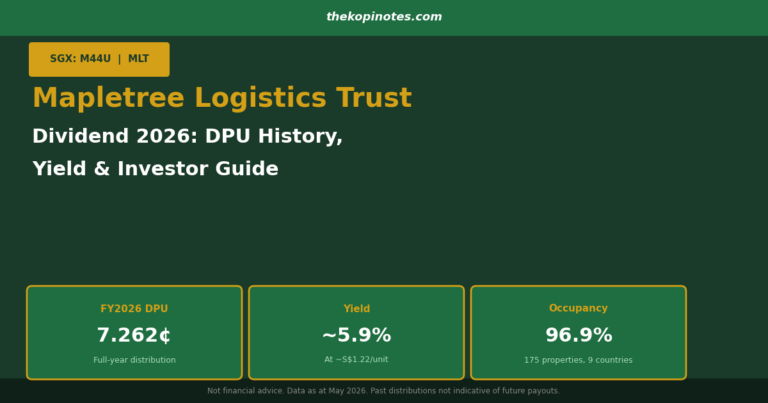

| Mapletree Logistics Trust (M44U) | Logistics | ~6.8% | ~43% | MEDIUM |

| Suntec REIT (T82U) | Office/Retail | ~5.5% | ~42% | LOW |

| Mapletree Pan Asia Commercial Trust (N2IU) | Office/Retail | ~7.2% | ~40% | MEDIUM |

| Starhill Global REIT (P40U) | Retail/Office | ~6.8% | ~35% | MEDIUM |

| AIMS APAC REIT (O5RU) | Industrial | ~7.8% | ~33% | LOW–MED |

| Elite Commercial REIT (MXNU) | Overseas Office | ~8.5% | ~45% | HIGH |

Data as at April 2026. Yields are approximate and based on trailing DPU / prevailing unit price. Not financial advice. Always verify with SGX or the REIT’s official investor relations page.

S-REIT tariff resilience score vs forward yield — April 2026. Not financial advice.

Data Centre REITs: Lowest Tariff Risk, Strongest Growth

Data centre REITs are the standout performers in a tariff environment. AI-driven demand for compute capacity has sent rental reversions surging — Keppel DC REIT (AJBU) reported FY2025 DPU growth of 9.8% year-on-year to 10.381 Singapore cents, with rental reversions jumping 45%. This type of structural demand is entirely decoupled from US-China trade tensions.

Key points for data centre REITs:

- Hyperscalers (AWS, Google, Microsoft) are locking in long-term leases, providing 5–10 year income visibility.

- Singapore remains a preferred data centre hub in Asia due to political stability, connectivity, and MAS fintech regulation.

- Power and cooling constraints limit new supply, supporting rental growth.

- A17U (CapitaLand Ascendas REIT) has significant exposure to North American and European data centres in addition to Singapore assets, diversifying its income base further.

Verdict: Data centre REITs offer the best combination of low tariff risk and income growth. Premium pricing (lower yield) is justified by the growth profile. Look for dips to accumulate.

Industrial & Logistics REITs: Moderate Risk, High Yield

Singapore’s industrial REITs occupy an interesting middle ground. For assets anchored in Singapore — high-spec factories, business parks, and light industrial — the structural tailwinds are strong. Global supply chain reconfiguration is pushing manufacturers to establish “China plus one” bases in Southeast Asia, and Singapore remains the preferred hub for high-value manufacturing (semiconductors, pharmaceuticals, biomedical).

Mapletree Industrial Trust (MIT, ME8U) trades at approximately 6.5% yield with over 40% of its portfolio in Singapore industrial and data centre assets. It recovered from tariff-induced share price declines in early 2026, supported by strong occupancy and rent reversions in its Singapore high-spec segment.

The risk lies in logistics REITs with significant China exposure. Mapletree Logistics Trust (MLT, M44U) has roughly 27% of its portfolio in China. If Chinese manufacturers reduce exports in response to US tariffs, warehouse demand in China-based logistics parks could soften. MLT compensates with higher yield (~6.8%) and a diversified 9-country portfolio, but investors should model this risk into their expectations.

Verdict: Industrial REITs with Singapore-anchored assets are buys on weakness. Logistics REITs with China exposure offer higher yield but require careful monitoring of occupancy and rental renewal rates.

Retail REITs: Defensive Domestic Income

Singapore’s suburban retail REITs are among the most defensive S-REIT sub-sectors in a tariff environment. Their tenants — supermarkets, F&B, healthcare, personal services — are largely necessity-driven and insulated from both tariff impacts and e-commerce disruption. Frasers Centrepoint Trust (FCT, J69U) is the poster child here, with a portfolio of suburban malls (Causeway Point, Northpoint City, Waterway Point) reporting robust tenant sales and high occupancy consistently above 98%.

FCT’s FY2025 DPU edged up 0.6% to S$0.12113, supported by gross revenue growth of 10.8% year-on-year. For income investors seeking stability, suburban retail REITs offer predictable distributions backed by Singapore’s resilient domestic consumption.

Orchard Road-focused retail assets face a slightly higher risk from any slowdown in tourist spending if global travel sentiment is dented by geopolitical uncertainty — but even this risk is modest given Singapore’s position as a regional hub.

Verdict: Suburban retail REITs are core holdings for income stability. Low tariff risk, high occupancy, and necessity-based tenants make them reliable income generators.

Office REITs: Improving but Selective

Singapore CBD office REITs have faced headwinds from hybrid work, with vacancy rates elevated through 2024–2025. However, leasing activity is recovering, with vacancy rates expected to peak in late 2025 to early 2026 before gradually tightening. Financial sector tenants — banks, asset managers, wealth management firms — remain Singapore’s core office demand drivers, and these are not directly impacted by US tariff policy.

Suntec REIT (T82U) reported NPI growth of 6.9% year-on-year in its latest results, though DPU slipped slightly due to a higher unit base following its Marina Bay Financial Centre Tower 3 acquisition. The acquisition significantly strengthens Suntec’s CBD presence and positions it well for the office recovery cycle.

Verdict: Office REITs are improving but require selectivity. Pure Singapore CBD office exposure is relatively safe; REITs with significant overseas office portfolios in markets like Australia or the UK face additional currency and demand risks.

Hospitality REITs: Most Cyclical, Watch Closely

Hospitality REITs are the most cyclical S-REIT sub-sector and the most sensitive to global sentiment shifts. US tariff uncertainty can dampen business travel, corporate event bookings, and tourist arrivals — all of which flow directly into hotel RevPAR (Revenue per Available Room).

That said, Singapore’s hospitality REITs benefit from several protective structures. Many operate under master lease arrangements where the hotel operator pays a fixed base rent plus variable component, providing downside protection for the REIT’s income. Far East Hospitality Trust, for example, derives a significant portion of its income from fixed master leases.

OCBC Research rates hospitality as the most cyclical sub-sector and last in order of preference after retail, industrial, and office. For investors prioritising income stability, we agree — hospitality REITs should be a satellite allocation, not a core position, in a tariff-uncertainty environment.

Verdict: Suitable for yield hunters willing to accept cyclicality. Hold if master lease income provides adequate floor; trim if exposure to variable RevPAR components is high.

Overseas Commercial REITs: Higher Yield, Higher Risk

Overseas-focused commercial REITs — those with significant exposure to European offices, UK government properties, or US assets — offer the highest yields in the S-REIT universe (8–10%), but come with elevated risks: currency volatility, local property market cycles, and geopolitical considerations.

In a tariff environment, overseas REITs with assets in tariff-affected economies face compound risk: their properties may see softer tenant demand if local economies slow, and their Singapore-dollar distributions may be reduced by unfavourable currency movements.

REITs like Elite Commercial REIT (UK government-leased offices) or Manulife US REIT offer high yields with specific risk profiles. These are appropriate for experienced investors with a clear view on the underlying market dynamics, not for passive income investors seeking stability.

Verdict: High-yield, high-risk. Appropriate as a small satellite allocation for yield enhancement, not as core holdings. Conduct thorough due diligence on currency, lease expiry profiles, and local vacancy before investing.

Investor Strategy: How to Position Your S-REIT Portfolio in 2026

Given the tariff backdrop, here is how we would think about S-REIT portfolio construction for a Singapore retail investor in 2026:

Core (60–70%): Low tariff-risk, stable income

- Data centre REITs (Keppel DC REIT, CapitaLand Ascendas REIT) — for income growth and structural demand

- Suburban retail REITs (Frasers Centrepoint Trust) — for stability and domestic consumption exposure

- Singapore-anchored industrial REITs (Mapletree Industrial Trust) — for higher yield with manageable risk

Satellite (20–30%): Higher yield, moderate risk

- Logistics REITs (Mapletree Logistics Trust) — yield pickup with diversified geography; monitor China portfolio

- Office REITs (Suntec REIT) — positioned for recovery cycle; accept short-term DPU softness

- AIMS APAC REIT — high yield (~7.8%) with conservative gearing (~33%) and SG-anchored industrial assets

Tactical (0–10%): High yield, high risk

- Overseas commercial or hospitality REITs — only for experienced investors with specific thesis

Use our S-REIT Dividend Yield Calculator to model your expected income from different REIT allocations. For a broader view of your passive income portfolio, check out the Dividend Portfolio Yield Calculator.

Investors using CPF OA funds should also note that many S-REITs are CPF-investible — check the CPF investment strategy guide for how to incorporate S-REITs into your CPF portfolio.

If you prefer managed REIT exposure, platforms like Syfe (Syfe REIT+) and Endowus offer diversified S-REIT portfolios that rebalance automatically — useful for hands-off investors.

For ETF investors, the Singapore REIT ETF guide covers the NikkoAM-StraitsTrading Asia ex Japan REIT ETF (CFA) and Lion-Phillip S-REIT ETF (CLR) as passive alternatives.

Frequently Asked Questions

Do US tariffs directly affect Singapore REITs?

Which S-REIT sub-sector is most resilient to tariffs?

Which S-REIT sub-sector is most exposed to tariff risk?

What is the average S-REIT yield in April 2026?

Is the S-REIT sector trading at a discount to NAV?

Can I use CPF OA to invest in S-REITs?

What is a good gearing ratio for an S-REIT?

Start Building Your S-REIT Income Portfolio

Use our free tools to model your S-REIT income and compare yields across your portfolio.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.