Passive Income Singapore 2026: 8 Proven Strategies to Earn While You Sleep

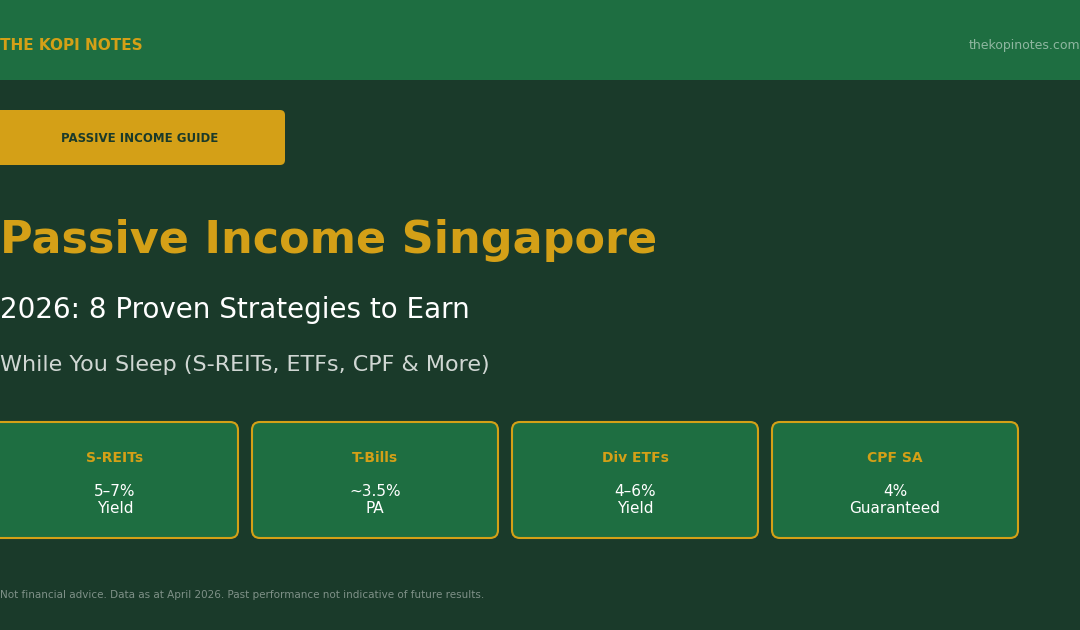

Passive income in Singapore is more achievable today than ever — with S-REITs yielding 5–7%, T-Bills paying ~3.5% p.a., and CPF guaranteeing 4% on your Special/Retirement Account, there are multiple ways to build income streams that work even when you’re not. This guide breaks down the 8 best passive income strategies for Singapore residents in 2026, with real yield data, minimum investment amounts, and practical tips to get started. Not financial advice — please do your own research.

Table of Contents

Contents — Click to expand

- What Is Passive Income in Singapore?

- Strategy 1: Singapore REITs (S-REITs)

- Strategy 2: Dividend ETFs

- Strategy 3: T-Bills and Singapore Savings Bonds

- Strategy 4: Maximise CPF Interest

- Strategy 5: Robo-Advisors and Dividend Portfolios

- Strategy 6: SRS Investment Income

- Strategy 7: Rental Property Income

- Strategy 8: Blue-Chip Dividend Stocks

- 2026 Passive Income Comparison Table

- How to Start Building Passive Income in Singapore

- Frequently Asked Questions

What Is Passive Income in Singapore?

Passive income is money earned with minimal ongoing effort — think dividends, rental income, interest payments, or distributions from investment vehicles. In Singapore, several factors make passive income especially attractive: no capital gains tax, no dividend tax for individuals, and a robust financial ecosystem including SGX-listed REITs, government-backed savings instruments, and CPF interest rates that beat most bank deposits.

In 2026, with the rising cost of living and Singapore’s official retirement age moving to 64 (and re-employment age to 69 from 1 July 2026), building passive income streams has become less a luxury and more a financial necessity. Whether you’re aiming for financial independence or simply want to supplement your salary, this guide covers the most reliable and tested strategies available to Singapore investors today.

The key principle: passive income compounds over time. A $100,000 portfolio earning 6% annually generates $6,000 in the first year — but $9,600 by year 10 if reinvested. Starting early and diversifying across several income streams is the proven path to building meaningful passive income in Singapore.

Strategy 1: Singapore REITs (S-REITs) — 5–7% Yield

S-REITs are the backbone of passive income investing in Singapore. Listed on SGX, Singapore REITs are legally required to distribute at least 90% of their taxable income to unitholders — which means regular quarterly or semi-annual distributions (similar to dividends). As at April 2026, the average S-REIT yield stands at approximately 6.2%, with individual REITs ranging from 4.5% to over 8% depending on sector and risk profile.

Why S-REITs work for passive income: Unlike stocks where dividends are discretionary, REIT distributions are structurally mandated. You buy units via your CDP/SRS/CPF Investment Scheme account through any brokerage — Tiger Brokers, Moomoo, FSMOne — and receive distributions automatically. The minimum investment is typically $200–$1,000 for a small lot of units.

Top S-REIT sectors for passive income in 2026:

- Industrial REITs (e.g. Mapletree Logistics Trust, AIMS APAC REIT) — 6–8% yield, stable demand from e-commerce logistics

- Retail REITs (e.g. Frasers Centrepoint Trust, Mapletree Pan Asia Commercial Trust) — 5–7% yield, Singapore suburban mall resilience

- Data Centre REITs (e.g. Keppel DC REIT) — 4.5–6% yield, AI/cloud tailwinds but premium valuations

- Hospitality REITs (e.g. Far East Hospitality Trust) — 6–7% yield, Singapore tourism recovery

Tax advantage: S-REIT distributions to Singapore individual investors are generally tax-exempt at the personal level. This makes the gross yield effectively equal to the net yield — a significant advantage over many other passive income vehicles.

👉 For a comprehensive comparison, see our Best S-REITs Singapore 2026 guide with full yield tables and gearing analysis.

Strategy 2: Dividend ETFs — 4–6% Yield, Low Effort

If picking individual S-REITs feels daunting, dividend-focused ETFs offer instant diversification with a single purchase. ETFs automatically rebalance and collect distributions from dozens of underlying holdings — your only job is to hold and collect.

Singapore-accessible dividend ETFs worth considering in 2026:

- Nikko AM STI ETF (SGX: G3B) — tracks Straits Times Index, ~3.5–4% yield, ultra-low cost, SGD-denominated

- Lion-Phillip S-REIT ETF (SGX: CLR) — pure S-REIT basket, ~5.5–6.5% yield, quarterly distributions

- SPDR S&P 500 ETF (SGX: S27) — USD-denominated, ~1.5% yield but strong capital appreciation track record

- iShares Asia Pacific Dividend ETF — broader Asia-Pacific dividend payers, ~4–5% yield

ETFs listed on SGX can be bought through CPF Investment Scheme (CPFIS) for qualifying funds, meaning you can use OA funds earning only 2.5% to potentially capture 4–6% dividend yields. However, CPFIS investing carries market risk — your capital is not guaranteed.

👉 See our Singapore REIT ETF Guide for a full breakdown of S-REIT ETF options, fees, and how to invest via CPF.

Strategy 3: Singapore T-Bills & Savings Bonds — Risk-Free ~3.5% p.a.

For risk-averse investors, Singapore government-issued fixed income instruments offer competitive passive income with full capital protection. Unlike S-REITs where unit prices fluctuate, T-Bills and SSBs are backed by the Singapore government (AAA-rated) — your capital is never at risk.

6-Month T-Bills: Cut-off yield in Q1 2026 auctions has hovered around 3.4–3.6% p.a. T-Bills are sold at a discount and redeemed at face value after 6 months, with the difference representing your “interest.” Minimum bid: $1,000. Apply via internet banking (DBS, OCBC, UOB) or CPF OA funds.

Singapore Savings Bonds (SSB): Step-up coupon structure — the longer you hold (up to 10 years), the higher your average annual return. April 2026 SSB offered a first-year rate of approximately 2.95% and a 10-year average of ~3.2% p.a. Maximum: $200,000 per person. Fully liquid — redeem any time with 1 business day notice, no penalty.

Fixed Deposits: MariBank (GXS Bank subsidiary) has offered promotional rates of 3.3–3.6% p.a. for 6-month fixed deposits, accessible via the GXS app. Traditional banks (DBS, OCBC, UOB) typically offer 2.5–3.0% for comparable tenors.

These instruments are ideal for the “safe” portion of your passive income portfolio — hold them alongside higher-yielding REITs/ETFs to balance risk and return.

Strategy 4: Maximise CPF Interest — 4% Guaranteed on RA/SA

CPF interest is often overlooked as a passive income strategy, but the numbers are compelling. In 2026, your CPF Retirement Account (RA) earns 4.0% p.a. — guaranteed by the Singapore government and completely risk-free. Your Special Account (SA, for those below 55) also earns 4.0%, while the Ordinary Account earns 2.5%.

How to maximise CPF passive “income”:

- Voluntary CPF top-ups (Section 7C): Top up your SA/RA with cash and earn 4% on funds you’d otherwise park in a bank at 0.05–3%. Tax relief of up to $8,000 per year applies for self top-ups.

- CPF LIFE: The CPF LIFE annuity scheme converts your RA balance into a monthly income stream from age 65 — effectively a government-guaranteed pension. At the Full Retirement Sum ($213,000 for 2026), monthly payouts start at approximately $1,540–$1,650 under the Standard Plan.

- Retirement Sum Topping Up Scheme: Top up a family member’s RA to help them maximise their CPF LIFE payout, while claiming tax relief yourself.

CPF interest is credited annually on 1 January — it doesn’t appear as monthly cash flow, but it compounds powerfully over decades. A $200,000 RA balance growing at 4% p.a. becomes $296,000 after 10 years without any additional contributions.

👉 Use our CPF LIFE Payout Calculator to estimate your monthly retirement income from CPF LIFE.

Strategy 5: Robo-Advisors & Dividend Portfolios — Hands-Off Investing

Robo-advisors automate portfolio management, rebalancing, and in some cases, regular distributions. For Singaporeans who want passive income without the complexity of picking stocks or REITs, robo-advisors offer a compelling low-effort solution.

Key robo-advisors for income-focused investing in Singapore:

- Endowus Income Portfolio: Targets 4–6% annual distribution, invests across income-focused funds from Dimensional, PIMCO, and BlackRock. Accepts CPF OA/SA and SRS funds. All-in fees: ~0.6% p.a. 👉 Get S$20 off fees with our Endowus referral code

- Syfe Income+: A curated portfolio of S-REITs, bonds, and dividend ETFs with target yield of ~5–6% p.a. Regular monthly distributions. Minimum: $500. 👉 Claim your Syfe referral code bonus

- FSMOne AutoWealth: Lower-cost option (~0.4% p.a.) focused on global ETFs. Less income-focused but suitable for long-term growth with reinvestment. 👉 FSMOne referral code for bonus cashback

Robo-advisors are particularly useful for investors who want to invest their CPF OA funds (which otherwise earn only 2.5%) into diversified income portfolios with historically higher returns — though note that investment returns are not guaranteed and past performance doesn’t predict future results.

Strategy 6: SRS Investment Income — Tax-Advantaged Passive Income

The Supplementary Retirement Scheme (SRS) is a government-initiated voluntary savings scheme that lets you contribute up to $15,300 per year (Singapore citizens and PRs) with a dollar-for-dollar tax deduction. Critically, SRS funds can be invested in a wide range of instruments including S-REITs, ETFs, unit trusts, and single stocks — generating passive income that grows tax-deferred.

Why SRS turbocharges passive income:

- Tax deduction on contribution: For someone in the 11.5% tax bracket (chargeable income $80,001–$120,000), a $15,300 SRS contribution saves $1,759.50 in taxes immediately.

- Tax-deferred growth: S-REIT distributions and dividends earned within SRS are not taxed until withdrawal.

- Concessionary withdrawal tax: From statutory retirement age (63 in 2026), only 50% of SRS withdrawals are taxable — and spread over 10 years, most retirees pay zero or minimal tax.

Investing $15,300/year in SRS into a diversified S-REIT portfolio earning 6% p.a. over 20 years could accumulate to over $560,000 — generating $33,600 in annual distributions before withdrawal. This is passive income at its most tax-efficient for Singapore residents.

👉 Use our SRS Tax Savings Calculator to see your exact annual tax savings from SRS contributions.

Strategy 7: Rental Property Income — 2.5–4% Gross Yield

Singapore residential property remains a classic passive income vehicle, though with important caveats. Rental yields in Singapore have compressed significantly over the past decade due to high property prices: the average gross rental yield on a private condominium in 2026 is approximately 2.8–3.5%, with HDB flat renting yielding 3–4% gross on market value.

Pros of rental income: Real asset with intrinsic value, potential for capital appreciation, leverage through mortgage financing amplifies equity returns.

Cons: High upfront capital ($400,000–$1.5M+), significant ABSD (Additional Buyer’s Stamp Duty) on second properties (20% for Singapore citizens), management effort (tenant sourcing, repairs), illiquid asset. Net yield after mortgage interest, property tax, maintenance, and agent fees often falls to 1–2% — below what T-Bills or S-REITs offer with far less capital.

For most Singapore investors without an existing investment property, REITs provide better risk-adjusted passive income than direct property. However, if you already own a second property or are buying for occupancy with rental upside, the leverage and capital appreciation potential of property remains compelling.

👉 Use our Rental Yield Calculator to calculate your property’s gross and net rental yield instantly.

Strategy 8: Blue-Chip Dividend Stocks — 3–6% Yield

SGX-listed blue-chip stocks — particularly Singapore banks, telcos, and infrastructure companies — have long been dividend stalwarts. Unlike REITs which must distribute 90% of income, dividend stocks offer discretionary dividends that can grow over time as company earnings increase.

Top dividend-paying SGX blue chips in 2026:

- DBS Group (D05): ~5.5% yield on 2025 full-year dividends (SGD $2.22/share). Singapore’s largest bank with strong capital ratios and consistent dividend track record.

- OCBC Bank (O39): ~5.2% yield. Steady dividend growth, conservative management, strong insurance income from Great Eastern.

- Singapore Telecommunications (Z74): ~4.8% yield. Telecom giant with regional exposure; dividends modestly recovered post-COVID restructuring.

- CapitaLand Integrated Commercial Trust (C38U): ~5.5% yield. Singapore’s largest REIT by market cap — classified as a REIT but worth mentioning for scale and liquidity.

Blue-chip dividends are not guaranteed — banks can and do cut dividends during crises (as seen during COVID-19 MAS guidance). However, over 5–10 year horizons, quality Singapore blue chips have delivered consistent and growing dividends that outpace inflation.

👉 See our full S-REIT and Dividend Stock comparison guide for more investment ideas.

2026 Passive Income Singapore: Strategy Comparison Table

| Strategy | Est. Yield (2026) | Min. Capital | Risk Level | Effort | CPF/SRS |

|---|---|---|---|---|---|

| S-REITs | 5–7% | ~$500 | Medium | Low-Med | ✅ Both |

| Dividend ETFs | 4–6% | ~$200 | Low-Med | Very Low | ✅ CPF OA |

| T-Bills / SSB | 3.2–3.6% | $1,000 | Risk-Free | Very Low | ✅ CPF OA |

| CPF Interest | 2.5–4% | Existing CPF | Risk-Free | None | N/A |

| Robo-Advisors | 4–6% | $500 | Low-Med | Very Low | ✅ Both |

| SRS Investments | Varies + tax savings | $1 | Low-Med | Low | ✅ SRS |

| Rental Property | 2.5–4% gross | $400,000+ | Medium | High | ❌ |

| Blue-Chip Stocks | 3–6% | ~$1,000 | Medium | Low-Med | ✅ CPF OA |

* Yields are estimates as at April 2026. Past performance is not indicative of future results. This is not financial advice.

How to Start Building Passive Income in Singapore

Building passive income doesn’t require a lump sum. Singapore’s financial system makes it accessible to start with as little as $500. Here’s a practical roadmap:

Step 1 — Emergency Fund First: Before investing, ensure 6 months of expenses sit in a high-yield savings account or MariBank savings (currently ~3% p.a. on balances up to $75,000). Use our Emergency Fund Calculator to find your target amount.

Step 2 — Maximise Risk-Free Returns: Top up CPF RA/SA if eligible (4% guaranteed), apply for T-Bills with CPF OA (3.5% vs 2.5% CPF OA rate), and contribute to SRS for the tax deduction.

Step 3 — Start with ETFs or Robo-Advisors: If you’re new to investing, begin with a diversified dividend ETF or robo-advisor. Dollar-cost average monthly — even $200/month invested at 5% p.a. grows to $83,000 after 20 years.

Step 4 — Add Individual S-REITs: As your knowledge grows, selectively add individual S-REITs for higher yield potential. Focus on REITs with low gearing (below 40%), stable sponsors (CapitaLand, Mapletree, Keppel), and resilient asset classes.

Step 5 — Review Annually: Passive income portfolios aren’t completely set-and-forget. Revisit once a year — check if any REIT distributions have been cut, rebalance towards your target allocation, and update your SRS contributions as your income grows.

👉 Use our free Retirement Planning Calculator to see how your passive income streams translate into a retirement timeline and whether you’re on track for financial independence.

Frequently Asked Questions: Passive Income Singapore

How much passive income can I earn from S-REITs in Singapore?

It depends on your invested capital. At a 6% average distribution yield, a $100,000 S-REIT portfolio generates approximately $6,000 per year ($500 per month) in passive income. Note that REIT unit prices fluctuate, so total returns include both distribution yield and capital gains/losses. To replace an average Singapore salary of $5,000/month entirely via S-REIT distributions, you’d need approximately $1,000,000 invested at 6% yield.

Is passive income taxable in Singapore?

For Singapore individual investors, most common forms of passive income are tax-exempt: S-REIT distributions are generally tax-exempt at the personal level, dividends from SGX-listed companies are tax-exempt (one-tier tax system), and capital gains are not taxed. Interest income from T-Bills, SSBs, and bank deposits is similarly not subject to personal income tax. The main exception is rental income — net rental income (rent minus allowable expenses) is taxable as personal income at your marginal rate. SRS withdrawals are taxable at 50% of the withdrawn amount but typically fall in low/zero tax brackets for retirees.

What is the best passive income investment in Singapore for beginners?

For beginners, Singapore Savings Bonds (SSBs) or T-Bills are the easiest starting point — risk-free, government-backed, and accessible via internet banking with $1,000 minimum. Once comfortable, a robo-advisor like Syfe or Endowus that offers diversified income portfolios is an excellent next step — they handle the selection and rebalancing automatically. As you grow your financial knowledge, individual S-REITs and dividend ETFs offer higher yields but require more research.

Can I use CPF to generate passive income?

Yes, in several ways. Your CPF SA/RA already earns 4% p.a. interest passively — this compounds automatically. CPF OA funds (earning 2.5%) can be invested via CPFIS into approved unit trusts, ETFs, and T-Bills for potentially higher returns. Endowus is particularly popular for investing CPF OA into income-focused funds. Additionally, CPF LIFE converts your RA balance into a guaranteed monthly income stream from age 65. Use our CPF LIFE Payout Calculator to estimate your monthly CPF LIFE income.

How much do I need to retire on passive income in Singapore?

Using the 4% safe withdrawal rule (a common retirement planning benchmark), you need 25x your annual expenses invested in a diversified portfolio. For a Singapore retiree spending $3,000/month ($36,000/year), that implies a $900,000 investment portfolio. However, CPF LIFE, rental income, and other income sources reduce the amount you need from investments. Our Retirement Planning Calculator lets you input CPF LIFE payouts, investment income, and expenses to calculate your personalised retirement number and savings trajectory.

Are S-REITs safe for passive income?

S-REITs are not risk-free — unit prices fall during market downturns (as seen during COVID-19 in 2020 and the interest rate hike cycle of 2022–2023), and distributions can be cut if rental income falls. However, Singapore-listed REITs are regulated by MAS, audited by major accounting firms, and their gearing ratios are capped at 50% by MAS regulation. Higher-quality S-REITs with strong sponsors (CapitaLand, Mapletree, Keppel) and diversified tenant bases have maintained or grown distributions over the long term. Diversifying across multiple REITs and sectors reduces concentration risk significantly.

Start Investing for Passive Income Today

Use our free tools to plan your passive income strategy, calculate CPF LIFE payouts, and work out how long your portfolio will last in retirement.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.