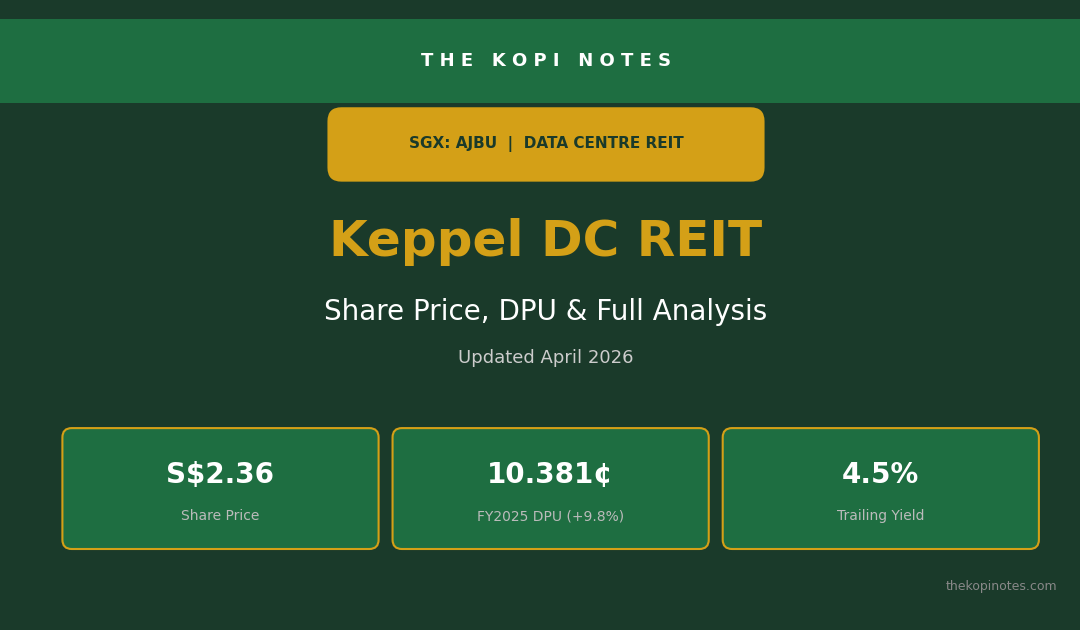

Keppel DC REIT (SGX: AJBU) Share Price 2026: 1Q26 DPU Surges 13%, Portfolio Hits S$6.3B

Keppel DC REIT is Singapore’s only pure-play data centre REIT — and 2026 is shaping up as its strongest year yet. With 1Q2026 DPU up 13.2% year-on-year, 95.6% occupancy, and S$6.3 billion in assets under management across 25 data centres in 10 countries, the AJBU share price is a key topic for every Singapore REIT investor this year.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. All data is sourced from Keppel DC REIT’s official filings and SGX announcements as at April 2026. Always do your own due diligence before investing.

Table of Contents

Contents — Click to expand

- Keppel DC REIT at a Glance — April 2026 Snapshot

- AJBU Share Price Analysis & Valuation

- DPU History: 7 Years of Consecutive Growth

- 1Q2026 Results Breakdown

- Portfolio Deep-Dive: 25 Data Centres, 10 Countries

- Financial Health: Gearing, ICR & Debt

- Peer Yield Comparison

- 2026 Outlook & Growth Catalysts

- How to Buy Keppel DC REIT in Singapore

- FAQ

1. Keppel DC REIT at a Glance — April 2026 Snapshot

Before we dive into the analysis, here are the numbers that matter most for Keppel DC REIT as at April 2026:

| Metric | Value |

|---|---|

| SGX Ticker | AJBU |

| Share Price (16 Apr 2026) | S$2.36 |

| Market Cap | ~S$5.6 billion |

| NAV per Unit | S$1.71 |

| P/NAV | 1.38× |

| FY2025 DPU | 10.381¢ (+9.8% YoY) |

| 1Q2026 DPU | 2.833¢ (+13.2% YoY) |

| Trailing Dividend Yield | ~4.5% |

| Gearing | 35.1% |

| ICR | 7.5× |

| Occupancy | 95.6% |

| WALE | 6.7 years |

| AUM | S$6.3 billion |

| Portfolio | 25 DCs, 10 countries |

Keppel DC REIT trades at a premium to NAV — a rarity in the S-REIT sector — reflecting the market’s confidence in secular data centre demand driven by AI, cloud computing, and digital transformation. The key question for investors is whether this premium is justified by the growth trajectory.

2. AJBU Share Price Analysis & Valuation

As at 16 April 2026, Keppel DC REIT’s unit price sits at S$2.36, well above its NAV of S$1.71 per unit. This gives it a P/NAV of 1.38× — the highest among all S-REITs.

For context, most S-REITs trade at a discount to book value (the sector average P/NAV is around 0.90×). Keppel DC REIT’s premium is driven by:

- Scarcity value: It is the only pure-play data centre REIT listed on the SGX.

- Structural demand: AI workloads, cloud migration, and 5G rollout are driving exponential data centre demand globally.

- DPU growth: Seven consecutive years of DPU increases — a track record few S-REITs can match.

- Singapore exposure: 62.7% of AUM is in Singapore, where data centre vacancy is below 1% and government moratoriums have restricted new supply.

The consensus analyst target price is S$2.533 (as at 16 April 2026), implying ~7.3% upside from the current level. Most brokerages maintain BUY or ADD recommendations.

For investors evaluating Keppel DC REIT, the trailing dividend yield of ~4.5% is lower than the S-REIT sector average of ~6.3%. However, the growth-adjusted return — factoring in 10-13% annual DPU growth — makes the effective total return comparable to or better than higher-yielding but lower-growth peers.

3. DPU History: 7 Years of Consecutive Growth

Keppel DC REIT has delivered DPU growth every single year since FY2019 — even through COVID-19 and the 2022-2023 rate hiking cycle. Here’s the full track record:

| Year | DPU (¢) | YoY Growth |

|---|---|---|

| FY2019 | 7.610 | — |

| FY2020 | 8.580 | +12.7% |

| FY2021 | 9.001 | +4.9% |

| FY2022 | 9.087 | +1.0% |

| FY2023 | 9.093 | +0.1% |

| FY2024 | 9.453 | +4.0% |

| FY2025 | 10.381 | +9.8% |

The FY2025 DPU of 10.381 cents was a record high, even after factoring in the enlarged unit base from the October 2025 preferential offering (180.6 million new units at 168.2% subscription rate). FY2025 distributable income surged 55.2% to S$268.1 million, driven by the acquisitions of Tokyo Data Centre 3 and the remaining interests in Keppel DC Singapore 3 and 4.

4. 1Q2026 Results Breakdown

Keppel DC REIT’s 1Q2026 business update (released mid-April 2026) showed acceleration across all key metrics:

| Metric | 1Q2026 | YoY Change |

|---|---|---|

| Gross Revenue | S$121.0M | +18.4% |

| Net Property Income | Est. ~S$90M+ | +19.4% |

| Distributable Income | S$74.6M | +20.7% |

| DPU | 2.833¢ | +13.2% |

| Occupancy | 95.6% | Stable |

| Rental Reversions | +51% | Up from +45% FY25 |

The 51% rental reversion rate is remarkable — it means tenants are renewing leases at rates 51% higher than expiring rents. This is driven by the extreme tightness in Singapore’s data centre market (vacancy below 1%) and strong demand from hyperscale cloud providers.

If annualised, the 1Q2026 DPU of 2.833¢ implies a full-year run rate of ~11.33¢, which would represent a further ~9% growth over FY2025. Analysts have revised FY2026 DPU estimates upward, forecasting a yield of 4.7-4.9% at the current share price.

Also notable: the divestment of Kelsterbach Data Centre (Germany) was completed in 1Q2026, which will help optimise the portfolio’s geographic mix toward higher-returning APAC markets.

5. Portfolio Deep-Dive: 25 Data Centres, 10 Countries

Keppel DC REIT owns and operates 25 data centres across 10 countries with total AUM of approximately S$6.3 billion (up 25.6% year-on-year). The portfolio spans key data centre hubs in Asia Pacific and Europe:

| Region | Countries | % of AUM |

|---|---|---|

| Singapore | Keppel DC Campus, Genting Lane, Serangoon | 62.7% |

| Australia | Sydney | 10.5% |

| Japan | Tokyo (incl. Tokyo DC 3) | 11.5% |

| Europe | Dublin, London, Amsterdam, Frankfurt, Milan | 15.3% |

| Southeast Asia | Jakarta, KL, Johor, Guangzhou, Huizhou | Included above |

Why Singapore dominance matters: Singapore’s data centre market has the tightest vacancy in APAC at less than 1%. A government moratorium on new data centre builds (now partially lifted for select green-certified facilities) has created a supply squeeze that directly benefits existing landlords like Keppel DC REIT — enabling those 51% rental reversions.

Hyperscaler tenants (Amazon Web Services, Google Cloud, Microsoft Azure, and similar tier-1 cloud providers) now account for 69.3% of gross rental income, up from 61.1% the prior year. This is a deliberate strategy: hyperscalers sign long leases, have investment-grade credit, and are less likely to churn. The WALE of 6.7 years is among the longest in the S-REIT sector.

6. Financial Health: Gearing, ICR & Debt Profile

Keppel DC REIT’s balance sheet is in solid shape despite the debt drawdowns for recent acquisitions:

- Aggregate Leverage: 35.1% (1Q2026), well below MAS’s 50% regulatory cap. Internal cap is 40%, leaving S$531 million of debt headroom for acquisitions.

- Interest Coverage Ratio: 7.5× — one of the highest in the S-REIT sector (most peers range from 2.0-4.0×). This means earnings cover interest expenses 7.5 times over.

- Average Cost of Debt: 2.8% (as at 4Q2025), benefiting from the SORA trough (~1.07%) and proactive hedging.

- Hedged Borrowings: 71.2% of total borrowings are hedged via interest rate swaps, providing protection against future rate rises.

- Weighted Average Debt Maturity: 3.3 years, with only 29.1% of debt maturing by end FY2027.

- Total Borrowings: S$2.4 billion.

The combination of low gearing, high ICR, and proactive hedging makes Keppel DC REIT one of the most financially resilient REITs on the SGX. An interest rate sensitivity analysis shows that a 25 basis point rate change impacts DPU by only ~0.6% — minimal for income investors.

For investors who want to stress-test REIT gearing ratios yourself, try our S-REIT Gearing Ratio Calculator.

7. Peer Yield Comparison

How does Keppel DC REIT’s yield compare with other major S-REITs? Here’s the picture as at April 2026:

| REIT | Trailing Yield | P/NAV | Gearing |

|---|---|---|---|

| Keppel DC REIT | 4.5% | 1.38× | 35.1% |

| CICT | 5.2% | 0.95× | 39.4% |

| CapitaLand Ascendas | 5.5% | 1.05× | 36.2% |

| Mapletree Industrial | 5.8% | 0.96× | 39.7% |

| Mapletree Logistics | 6.4% | 0.85× | 39.1% |

| Suntec REIT | 4.8% | 0.65× | 42.8% |

| ESR-LOGOS REIT | 9.4% | 0.91× | 38.5% |

Keppel DC REIT’s 4.5% yield is the lowest in this peer group — but that reflects its growth premium. If DPU continues growing at 10%+ annually, an investor buying at today’s price could see a yield-on-cost of 6.5-7%+ within 4-5 years. For a deeper dive into the best S-REITs across all sectors, see our Best S-REITs Singapore 2026 guide.

8. 2026 Outlook & Growth Catalysts

Several powerful tailwinds are converging for Keppel DC REIT in 2026:

1. AI-Driven Data Centre Demand

The explosion of generative AI workloads (large language models, inference computing, enterprise AI deployment) is driving unprecedented demand for high-density data centre capacity. McKinsey estimates global data centre demand will grow 26-36% annually through 2030. Keppel DC REIT’s hyperscaler tenant base (69.3% of income) positions it squarely in this megatrend.

2. Singapore Supply Squeeze

Singapore’s data centre moratorium (now partially lifted for green-certified builds only) means existing capacity is being repriced aggressively. The sub-1% vacancy rate in Singapore supports the 51% rental reversions we saw in 1Q2026. With 62.7% of AUM in Singapore, Keppel DC REIT is a primary beneficiary.

3. Falling Borrowing Costs

SORA has troughed at ~1.07% (down from the 3.03% peak), and Keppel DC REIT’s average cost of debt has already declined to 2.8%. With 71.2% of borrowings hedged, the REIT is positioned to benefit from lower refinancing costs as swaps roll off. For more on Singapore’s interest rate trajectory, see our SORA Rate Singapore 2026 analysis.

4. Acquisition Pipeline

With S$531 million of debt headroom (to 40% internal gearing cap) and strong sponsor support from Keppel Ltd, the REIT has ample capacity for accretive acquisitions. The focus is on hyperscale data centres in Singapore, Japan, South Korea, and Europe.

5. Keppel Data Centre Campus Expansion

The Keppel Data Centre Campus in Singapore (the REIT’s largest asset) recently secured a 10-year land lease extension, providing long-term visibility for the crown jewel of the portfolio.

Key Risks to Watch

- Tenant concentration: The top tenant accounts for 42.1% of monthly rent. A single non-renewal would materially impact DPU.

- P/NAV premium compression: If interest rates rise or data centre sentiment cools, the premium could narrow, pressuring unit prices.

- Currency risk: ~37% of AUM is outside Singapore, exposing the REIT to JPY, AUD, EUR, and GBP fluctuations.

- US-China tariff overhang: While data centres are not directly tariff-exposed, a global recession scenario would slow enterprise IT spending. See our Trump Tariffs Singapore REIT 2026 analysis for the broader macro context.

9. How to Buy Keppel DC REIT in Singapore

Keppel DC REIT (SGX: AJBU) trades on the Singapore Exchange in lots of 100 units. At the current price of S$2.36, one lot costs approximately S$236 — one of the most affordable entry points among blue-chip S-REITs.

Step-by-step:

- Open a CDP Securities Account with SGX (if you don’t already have one)

- Open a brokerage account — popular options include FSMOne, moomoo, Tiger Brokers, or IBKR

- Search for ticker AJBU on your broker’s platform

- Place a buy order (minimum 100 units)

CPF OA investors: Keppel DC REIT is CPFIS-approved, so you can purchase it using your CPF Ordinary Account via approved agents like FSMOne or DBS Vickers. See our CPF Investment Strategy guide for details.

SRS investors: You can also invest via your SRS account through most brokerages. Read our SRS Account Guide 2026 for the tax savings angle.

For tools to help you plan your REIT portfolio, try our REITs Dividend Yield Calculator or the Retirement Planning Calculator.

Frequently Asked Questions

What is Keppel DC REIT's share price today?

What is Keppel DC REIT's dividend yield?

Is Keppel DC REIT a good investment in 2026?

How many data centres does Keppel DC REIT own?

What is Keppel DC REIT's gearing ratio?

Can I buy Keppel DC REIT with CPF?

Who is Keppel DC REIT's largest tenant?

What is Keppel DC REIT's NAV per unit?

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.