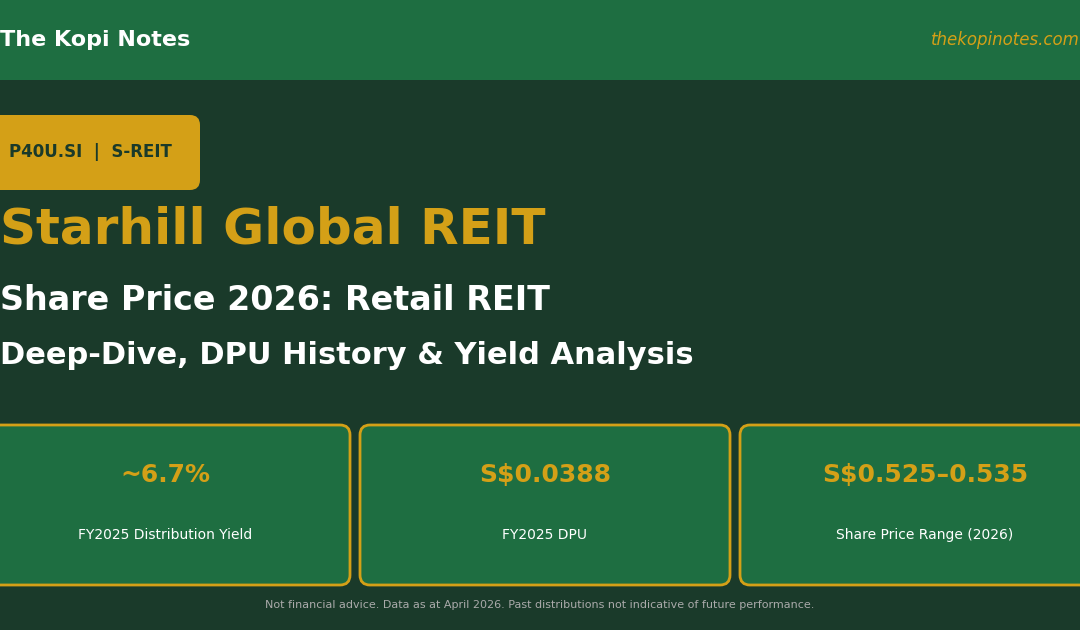

Starhill Global REIT Share Price 2026: DPU History, ~6.7% Yield & Deep-Dive Analysis

Starhill Global REIT (SGX: P40U) is one of Singapore’s longest-listed retail and office REITs, with a portfolio anchored by Wisma Atria and Ngee Ann City on Orchard Road. In this deep-dive, we examine its share price performance in 2026, full DPU history from FY2016 to FY2025, distribution yield versus retail REIT peers, portfolio fundamentals, and outlook for income investors. This article is for informational purposes only and does not constitute financial advice. Data as at April 2026.

Table of Contents

Contents — Click to expand

Starhill Global REIT — Quick Overview

Starhill Global REIT was listed on the SGX in September 2005 and is managed by YTL Starhill Global REIT Management Limited. Its portfolio spans Singapore, Malaysia, Australia, and Japan, with Singapore properties contributing the majority of net property income (NPI).

| Item | Detail |

|---|---|

| SGX Ticker | P40U.SI |

| Listed Since | September 2005 |

| Manager | YTL Starhill Global REIT Management Limited |

| Portfolio | Wisma Atria & Ngee Ann City (SG), The Starhill & Lot 10 (MY), Myer Centre Adelaide (AU), Daikanyama (JP) |

| FY2025 DPU | 3.88 SGD cents |

| FY2025 Distribution Yield | ~6.7% (at S$0.58 unit price) |

| Market Cap | ~S$1.1 billion |

| FY End | 30 June |

| Distribution Frequency | Half-yearly (June & December) |

| Gearing Ratio | ~35.8% (as at Dec 2025) |

Starhill Global REIT Share Price Performance 2026

As at April 2026, Starhill Global REIT units have been trading in the range of S$0.525–S$0.535, reflecting the broader pressures on S-REITs from elevated global interest rates and a cautious economic outlook for retail properties. The unit price is down roughly 8–10% from its 52-week high of ~S$0.585, set in mid-2025 when SORA rates began to fall.

| Period | Price Range (SGD) | Key Driver |

|---|---|---|

| Jan 2026 | S$0.545–S$0.560 | Post-FY2025 DPU announcement, yield-seeking inflows |

| Feb–Mar 2026 | S$0.535–S$0.555 | MAS tightening signals, US Fed hold at 3.50–3.75% |

| Apr 2026 | S$0.525–S$0.535 | Macro tariff uncertainty; cautious retail outlook |

At current prices, the implied forward yield is approximately 6.7–7.0%. Use our REITs Dividend Yield Calculator to model your personal entry-point yield.

Starhill Global REIT DPU History: FY2016–FY2025

One of the most important data points for any REIT investor is the distribution per unit (DPU) track record. For Starhill Global REIT, this tells a story of moderate compression during the pandemic years (FY2020–FY2022), followed by a gradual recovery as Orchard Road retail footfall recovered.

| Financial Year | DPU (SGD cents) | YoY Change |

|---|---|---|

| FY2025 (Jul 2024–Jun 2025) | 3.88 | +2.1% |

| FY2024 (Jul 2023–Jun 2024) | 3.80 | +2.2% |

| FY2023 (Jul 2022–Jun 2023) | 3.72 | +4.2% |

| FY2022 (Jul 2021–Jun 2022) | 3.57 | -1.9% |

| FY2021 (Jul 2020–Jun 2021) | 3.64 | -6.2% |

| FY2020 (Jul 2019–Jun 2020) | 3.88 | -17.8% |

| FY2019 (Jul 2018–Jun 2019) | 4.72 | -0.4% |

| FY2018 (Jul 2017–Jun 2018) | 4.74 | -5.2% |

| FY2017 (Jul 2016–Jun 2017) | 5.00 | -0.6% |

| FY2016 (Jul 2015–Jun 2016) | 5.03 | — |

The pandemic cut FY2020 DPU by nearly 18% as Singapore’s circuit breaker devastated footfall at Wisma Atria. The recovery since FY2023 has been steady but gradual — FY2025 DPU of 3.88 cents is still 23% below the FY2016 peak of 5.03 cents.

Distribution Yield Analysis

At an April 2026 unit price of approximately S$0.530, the trailing FY2025 yield is approximately 7.3% (3.88¢ ÷ 53.0¢). The forward yield based on expected FY2026 DPU of 3.90–4.00 cents implies approximately 7.4–7.5%.

Starhill’s higher yield over FCT (~5.9%) and CICT (~5.3%) reflects its smaller market cap, shorter WALE, and multi-geography execution risk. However, its gearing of 35.8% is the tightest among retail REIT peers, offering balance sheet headroom.

For CPF investors: Starhill Global REIT is eligible for the CPF Investment Scheme (CPFIS) using OA funds. See our CPF Investment Strategy Guide for how to structure REIT investments within CPF.

Portfolio Fundamentals: Wisma Atria, Ngee Ann City & Beyond

Singapore properties account for roughly 70% of total NPI. Wisma Atria on Orchard Road is the flagship asset — approximately 235,000 sq ft of net lettable area with ~100 retail units. The Ngee Ann City retail podium (Starhill’s portion) features luxury tenants including Takashimaya.

| Segment | NPI Contribution | Committed Occupancy | WALE (years) |

|---|---|---|---|

| Singapore (Wisma Atria + Ngee Ann City) | ~70% | 97.4% | 2.6 |

| Malaysia (Starhill Gallery, Lot 10) | ~12% | 85.2% | 2.1 |

| Australia (Myer Centre Adelaide) | ~11% | 93.1% | 3.4 |

| Japan (Daikanyama) | ~7% | 100% | Long-term |

The Singapore portfolio’s near-full occupancy (97.4%) reflects Orchard Road luxury retail resilience, particularly with the return of international tourists. For a broader view of S-REIT landscape comparisons, see our Best S-REITs Singapore 2026 guide.

Gearing & Financial Health

As at December 2025, Starhill Global REIT’s aggregate leverage stood at approximately 35.8%, well within MAS’s 50% statutory limit. The REIT’s interest coverage ratio (ICR) is estimated at approximately 3.0x, and approximately 78% of borrowings are on fixed rates — limiting near-term floating-rate refinancing risk.

| Financial Metric | Value | MAS Limit / Benchmark |

|---|---|---|

| Aggregate Leverage (Gearing) | ~35.8% | ≤50% (MAS limit) |

| Interest Coverage Ratio (ICR) | ~3.0x | ≥1.5x (MAS threshold) |

| NAV per unit | ~S$0.75 | — |

| Price-to-NAV ratio | ~0.71x (at S$0.530) | Below 1.0x = potential discount |

| % Fixed-rate debt | ~78% | Higher = less floating rate risk |

The price-to-NAV of ~0.71x means unitholders are acquiring assets at a ~29% discount to book value. Use our S-REIT Gearing Ratio & ICR Calculator to model various gearing scenarios.

Peer Comparison: Singapore Retail/Commercial REITs

| REIT | SGX Ticker | Yield (Apr 2026) | Gearing | WALE | Market Cap |

|---|---|---|---|---|---|

| Starhill Global REIT | P40U.SI | ~6.7–7.3% | 35.8% | 2.6y | ~S$1.1B |

| Frasers Centrepoint Trust | J69U.SI | ~5.9% | 38.5% | 4.1y | ~S$3.8B |

| CapitaLand Integrated Commercial Trust (CICT) | C38U.SI | ~5.3% | 40.2% | 3.8y | ~S$14.5B |

| Lendlease Global Commercial REIT | JYEU.SI | ~8.2% | 41.0% | 2.2y | ~S$1.4B |

| Mapletree Pan Asia Commercial Trust | N2IU.SI | ~7.1% | 39.7% | 3.5y | ~S$7.1B |

Starhill’s yield premium over FCT and CICT compensates investors for its smaller market cap and shorter WALE. Its gearing of 35.8% is the tightest among peers. For more on the S-REIT yield vs bond spread, use our S-REIT Yield vs SGS Bond Spread Calculator.

Outlook 2026 & Key Risks

Positive catalysts: Orchard Road luxury retail recovery driven by international tourist arrivals; SORA falling from 3.03% peak to ~1.07% improving refinancing economics; conservative gearing providing balance sheet headroom; 0.71x price-to-NAV discount offering margin of safety.

Key risks: Malaysia occupancy stuck at ~85%; AUD and JPY currency drag on reported NPI; global trade tariff uncertainty dampening luxury retail spending; lease expiry cliff with WALE of only 2.6 years; limited DPU growth visibility compared to industrial/logistics REITs.

For context on how the current interest rate environment is affecting Singapore REITs broadly, read our Fed Rate Hold 2026: What Singapore REIT Investors Need to Know.

Should You Invest in Starhill Global REIT?

Starhill Global REIT suits investors who value Orchard Road retail exposure with a higher yield (6.7–7.3%), conservative gearing, and are comfortable with moderate multi-geography risk. It is less suitable for those who want larger-cap, more liquid REITs or higher DPU growth potential from industrial/logistics assets.

For a structured approach to building a REIT income portfolio, see our Dividend Portfolio Yield Calculator. To understand how CPF funds can be deployed into REITs like Starhill, refer to our CPF Investment Strategy Guide.

If you are setting up a brokerage account to invest in SGX-listed REITs, consider using Syfe for their low-cost REIT ETF exposure, or FSMOne for direct REIT investing.

FAQ — Starhill Global REIT

What is the Starhill Global REIT share price today?

As at April 2026, Starhill Global REIT (SGX: P40U) is trading in the range of S$0.525–S$0.535. For the latest live price, check SGX’s market data or your brokerage platform.

What is Starhill Global REIT's DPU and yield for FY2025?

Starhill Global REIT declared a full-year DPU of 3.88 SGD cents for FY2025 (financial year ending 30 June 2025). At a unit price of S$0.530, this translates to a trailing yield of approximately 7.3%. Forward FY2026 yield is estimated at 7.4–7.5% based on consensus DPU estimates of 3.90–4.00 cents.

Is Starhill Global REIT a good buy in 2026?

Starhill Global REIT offers a higher yield (6.7–7.3%) than larger retail REITs like CICT or FCT, with conservative gearing (~35.8%) and Orchard Road luxury retail exposure. However, the ongoing Malaysia occupancy drag, shorter WALE, and multi-currency risk mean it suits investors comfortable with these trade-offs. This is not financial advice — do your own due diligence before investing.

Can I invest in Starhill Global REIT using CPF?

Yes. Starhill Global REIT is listed on SGX and is eligible for the CPF Investment Scheme (CPFIS) using CPF Ordinary Account (OA) funds. See our CPF Investment Strategy Guide for full details on the S$20,000 minimum OA balance requirement.

What properties does Starhill Global REIT own?

Key assets include Wisma Atria (Orchard Road, Singapore), a portion of the Ngee Ann City retail podium (Orchard Road, Singapore), The Starhill and Lot 10 (Kuala Lumpur, Malaysia), Myer Centre Adelaide (Australia), and Daikanyama (Tokyo, Japan). Singapore assets contribute approximately 70% of net property income.

How often does Starhill Global REIT pay distributions?

Starhill Global REIT distributes twice a year — typically in September (for July–December) and in March (for January–June). The financial year ends on 30 June. A scrip distribution alternative (DRIP) is offered, allowing unitholders to receive new units instead of cash.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.