Keppel DC REIT Price Today: Is It Cheap or Expensive? (2026 Guide)

Current valuation, P/NAV analysis & what Singapore investors need to know

Keppel DC REIT (SGX: AJBU) is Singapore’s largest pure-play data centre REIT, with a portfolio spanning 23 data centres across 11 countries. As at June 2026, the REIT trades at approximately S$1.90–S$2.10 per unit on the Singapore Exchange. After a sharp correction in 2024–2025, the current Keppel DC REIT price looks attractive on a price-to-NAV basis — but rising debt costs and lease renewal risks mean it’s not a slam dunk. Here’s a complete breakdown to help you decide.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

- Keppel DC REIT price as at June 2026: ~S$1.90–S$2.10/unit — about 15–20% below its 2021 peak of S$3.00+

- Current P/NAV ratio of ~0.9x suggests moderate undervaluation vs. global data centre peers trading at 1.2–1.5x

- Annualised distribution yield sits around 5.5–6.5% — attractive for a high-growth sector

Table of Contents

Contents

- Keppel DC REIT Current Price (June 2026)

- Price History: From Peak to Present

- Is Keppel DC REIT Cheap? Valuation Analysis

- Dividend Yield at Current Price

- Key Financial Metrics Snapshot

- Price Catalysts: What Could Move the Price

- Risks to the Current Price

- How to Buy Keppel DC REIT in Singapore

- Frequently Asked Questions

Keppel DC REIT Current Price (June 2026)

As at June 2026, Keppel DC REIT (SGX ticker: AJBU) trades in the range of S$1.90 to S$2.10 per unit. The exact price fluctuates with daily market sentiment, interest rate expectations, and data centre sector news.

For the most current price, check the SGX website or your brokerage app. The REIT trades under the ticker AJBU on the Singapore Exchange (SGX) mainboard.

Lot size: 100 units minimum. At S$2.00/unit, one lot costs S$200 — making this one of the more accessible blue-chip REITs for retail investors.

| Metric | Value (Jun 2026 Est.) |

|---|---|

| Unit price | ~S$1.90–S$2.10 |

| 52-week high | ~S$2.25 |

| 52-week low | ~S$1.55 |

| Market capitalisation | ~S$3.6–S$3.9 billion |

| Average daily volume | ~10–15 million units |

Source: SGX, Bloomberg estimates, June 2026. Verify current price on your brokerage before transacting.

Price History: From Peak to Present

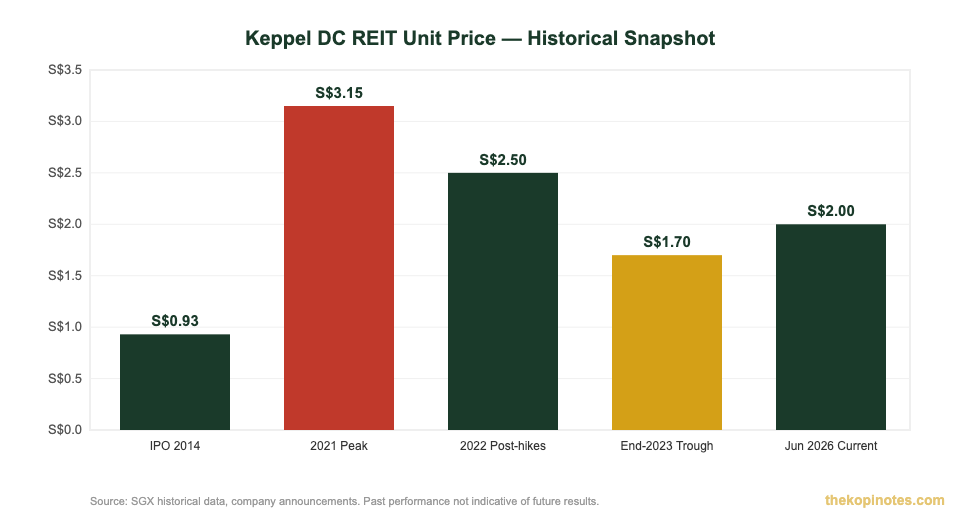

Keppel DC REIT listed on SGX in December 2014 at S$0.93 per unit. It was one of Asia’s first listed data centre REITs — and early investors were generously rewarded.

The REIT surged to an all-time high of over S$3.00 per unit in early 2021, driven by explosive cloud and remote-work demand during the pandemic. At that peak, the yield had compressed to under 3%, and the P/NAV ratio ballooned to 2x+.

The correction since then has been significant:

| Period | Approx. Price | Key Driver |

|---|---|---|

| IPO (Dec 2014) | S$0.93 | First-mover DC REIT listing |

| Peak (Jan 2021) | ~S$3.15 | Covid cloud/remote-work demand |

| Mid-2022 | ~S$2.50 | Rate hike cycle began |

| End-2023 | ~S$1.70 | High rates compress REIT valuations |

| June 2026 | ~S$1.90–S$2.10 | Partial recovery, AI tailwinds |

Source: SGX historical data, company announcements. Past performance is not indicative of future results.

The key takeaway: at S$2.00, you’re buying at about 35% below the 2021 peak. Whether that’s a bargain depends entirely on whether the REIT’s earnings can grow into the next cycle — and that’s what the valuation section below explores.

Is Keppel DC REIT Cheap? Valuation Analysis

Price alone tells you nothing. You need to compare it against what the REIT actually owns. The two key valuation metrics for REITs are Price-to-NAV (P/NAV) and dividend yield.

Price-to-NAV Ratio

Net Asset Value (NAV) per unit represents the underlying book value of the REIT’s properties after liabilities. Keppel DC REIT’s NAV per unit stands at approximately S$2.20–S$2.30 as at the latest financial results (Q1 2026).

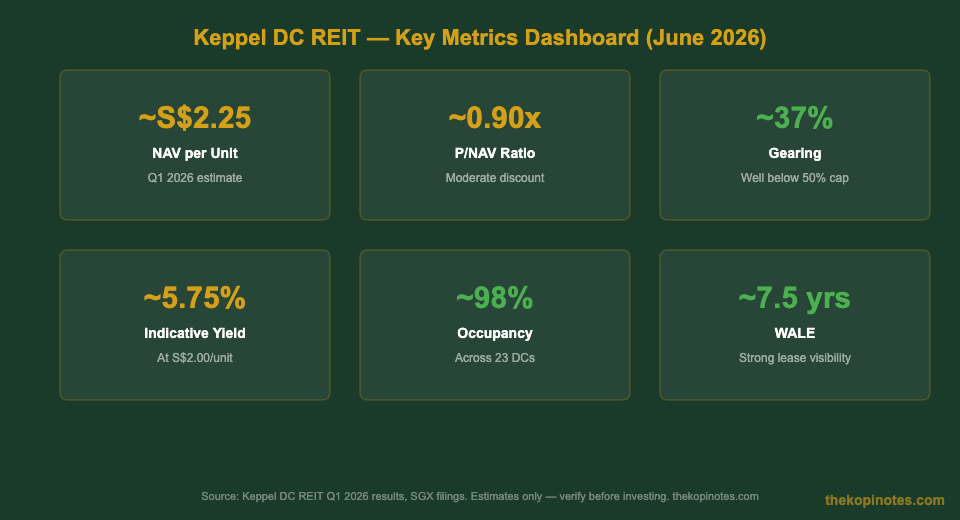

At a unit price of S$2.00, that puts the P/NAV ratio at roughly 0.87–0.91x. You’re buying S$1 of property assets for roughly S$0.89.

| Period | P/NAV | Interpretation |

|---|---|---|

| 2021 Peak | ~2.1x | Significantly overvalued |

| 2022 (post-rate hikes) | ~1.3x | Moderately premium |

| End-2023 (trough) | ~0.75x | Attractive value entry point |

| June 2026 (current) | ~0.87–0.91x | Moderate discount — fair to attractive |

Source: Keppel DC REIT financial results, SGX, analyst estimates. June 2026.

The 2023 trough at 0.75x NAV was arguably the deepest entry point of the decade. Today’s 0.9x isn’t screaming cheap — but it’s far more reasonable than the 2021 euphoria.

For Singapore investors hunting passive income in Singapore, the current price offers a combination of moderate undervaluation and a decent yield — which we’ll explore next.

Dividend Yield at Current Price

Keppel DC REIT pays distributions semi-annually (twice a year). Distribution Per Unit (DPU) — basically how much cash each unit pays you — has been in the range of S$0.10–S$0.12 per unit annually in recent years.

At a unit price of S$2.00 and a DPU of ~S$0.115:

This is a meaningful improvement from the 2021 peak yield of under 3%. However, note that Keppel DC REIT’s DPU growth has moderated. The REIT grew DPU by double digits in 2019–2021, but higher borrowing costs have squeezed distributions more recently.

| Entry Price (S$) | DPU (est. S$0.115) | Indicative Yield |

|---|---|---|

| S$1.70 | S$0.115 | 6.76% |

| S$1.90 | S$0.115 | 6.05% |

| S$2.00 | S$0.115 | 5.75% |

| S$2.10 | S$0.115 | 5.48% |

| S$2.25 | S$0.115 | 5.11% |

Source: Keppel DC REIT distribution history; DPU is illustrative based on recent annualised figures. Verify actual DPU from company announcements before investing.

Compare this against the best S-REITs in Singapore 2026 to see how Keppel DC REIT’s yield stacks up against the broader REIT universe.

Key Financial Metrics Snapshot

Before buying any REIT, you want to check the financial health — not just the yield. For Keppel DC REIT, here’s the dashboard you should review:

| Metric | FY2025 / Q1 2026 Est. | Commentary |

|---|---|---|

| NAV per unit | ~S$2.20–S$2.30 | Stable; FX hedging limits volatility |

| Gearing ratio | ~35–38% | Comfortable; MAS limit is 50% |

| Interest coverage ratio | ~4.5–5.5x | Healthy — well above 2.5x minimum |

| Weighted avg. debt cost | ~3.5–4.2% | Higher than 2021; limits DPU growth |

| Occupancy rate | ~98% | Excellent; DC demand remains robust |

| WALE (lease expiry) | ~7–8 years | Long leases provide income visibility |

| No. of properties | 23 DCs across 11 countries | Well-diversified geographically |

Source: Keppel DC REIT Q1 2026 business update, company filings. Figures are estimates; verify against latest SGX announcements.

The balance sheet looks solid. A gearing ratio of ~37% gives the REIT meaningful debt headroom before hitting the MAS 50% cap. The 98% occupancy is exceptional and reflects the structural tailwind behind data centres: AI model training, cloud computing, and edge infrastructure are all driving demand for colocation space.

Price Catalysts: What Could Move the Price Higher

If you’re considering buying at the current Keppel DC REIT price, here are the key drivers that could push the unit price higher over the next 12–24 months:

1. Interest Rate Cuts

REITs are rate-sensitive. As global central banks (Fed, ECB, MAS) cut rates, borrowing costs fall. This does two things: it directly increases distributable income (DPU rises as interest expenses drop), and it makes REIT yields more attractive relative to bonds — pushing unit prices up.

2. AI-Driven Data Centre Demand

Artificial intelligence infrastructure requires massive compute power. Hyperscalers like Microsoft, Google, and Amazon are expanding data centre footprints globally. Keppel DC REIT benefits directly from this trend — its facilities host colocation clients who serve these hyperscalers. A surge in AI capex spending means higher demand for KDCREIT’s buildings.

3. Accretive Acquisitions

Keppel DC REIT has a strong acquisition pipeline through its Sponsor (Keppel Ltd). If the REIT acquires new data centres at yields above its cost of capital, DPU grows — and the unit price typically re-rates higher. Watch for SGX announcements on new asset purchases.

4. Positive Rental Reversions

When leases renew at higher rental rates (positive reversion), income per property grows. With current data centre rents rising across Singapore, Germany, and Australia — three key KDCREIT markets — the next lease cycle could be meaningfully accretive.

For context on how KDCREIT compares to other data centre plays, see the broader S-REIT comparison guide for 2026.

Risks to the Current Price

No investment is risk-free. Here are the key risks that could keep the Keppel DC REIT price under pressure or push it lower:

1. Rates Stay Higher for Longer

If the Fed delays rate cuts — or reverses course and hikes again — REIT valuations will face renewed compression. Higher rates mean higher refinancing costs for Keppel DC REIT and a narrower spread between REIT yield and bond yield, reducing investor demand for REIT units.

2. Tenant Concentration Risk

A small number of large hyperscaler clients make up a significant portion of revenue. If a major tenant downsizes, non-renews, or shifts to self-build (building their own DCs), it could create material income disruption. Monitor the WALE and tenant list in each quarterly update.

3. FX Headwinds

Keppel DC REIT earns in multiple currencies (EUR, AUD, GBP, USD, JPY) and distributes in SGD. A strengthening SGD reduces the SGD-equivalent income from overseas assets. While the REIT hedges some FX exposure, residual currency risk remains.

4. Power Constraints & Regulatory Risks

Singapore has been selective about new data centre approvals due to power and land scarcity. While this limits new supply (good for existing assets), policy changes could restrict further growth in the Singapore portfolio. European markets also face increasing environmental scrutiny on power-hungry DCs.

Investing in S-REITs for the long term? Compare your options at the Singapore retirement calculator to model how REIT income fits into your overall plan.

How to Buy Keppel DC REIT in Singapore

Keppel DC REIT (AJBU) trades on the SGX mainboard. You can buy it through any SGX-linked brokerage. Here’s how:

Step 1: Open a Brokerage Account

You need a CDP-linked brokerage account to hold Singapore-listed REITs directly. Popular options include IBKR, Moomoo, Tiger Brokers, DBS Vickers, and UOB Kay Hian. For commission-free trading on many SGX counters, check the Syfe referral code and sign-up bonus for their Trade platform.

Step 2: Fund Your Account

Transfer SGD from your bank to your brokerage. Note: some brokerages require a minimum funding amount before you can place trades.

Step 3: Search for AJBU

On your brokerage platform, search for ticker AJBU or “Keppel DC REIT”. Confirm you’re looking at the correct counter (it trades on SGX mainboard in SGD).

Step 4: Place Your Order

SGX trades in lots of 100 units. At S$2.00/unit, one lot = S$200. You can place a limit order (specify a price) or market order (buy at the best available price). Brokerage commission: typically S$10–S$25 minimum or 0.08–0.28% per trade.

Alternative: Buy via a REIT ETF

If you want diversified S-REIT exposure without picking individual counters, consider the Singapore REIT ETF guide. The Lion-Phillip S-REIT ETF (CLR) and Nikko AM-Straits Trading S-REIT ETF both hold Keppel DC REIT as a top holding.

Want a platform built for Singapore dividend investors? The Endowus referral code (code: 2V343) gives you cash rewards when you invest your first S$10,000 — and Endowus offers CPF-approved REIT funds too.

Frequently Asked Questions

What is the current Keppel DC REIT price?

Is Keppel DC REIT undervalued in 2026?

What dividend yield does Keppel DC REIT offer at current prices?

What is the Keppel DC REIT ticker symbol on SGX?

Can I buy Keppel DC REIT using CPF?

What are the main risks of investing in Keppel DC REIT?

How does Keppel DC REIT compare to other S-REITs?

Disclaimer: This article is for educational purposes only and does not constitute financial advice. The Kopi Notes may earn referral fees when you use our referral codes — this does not affect our editorial objectivity. Always conduct your own due diligence or consult a licensed financial adviser before investing. Past performance of any REIT is not indicative of future results.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.