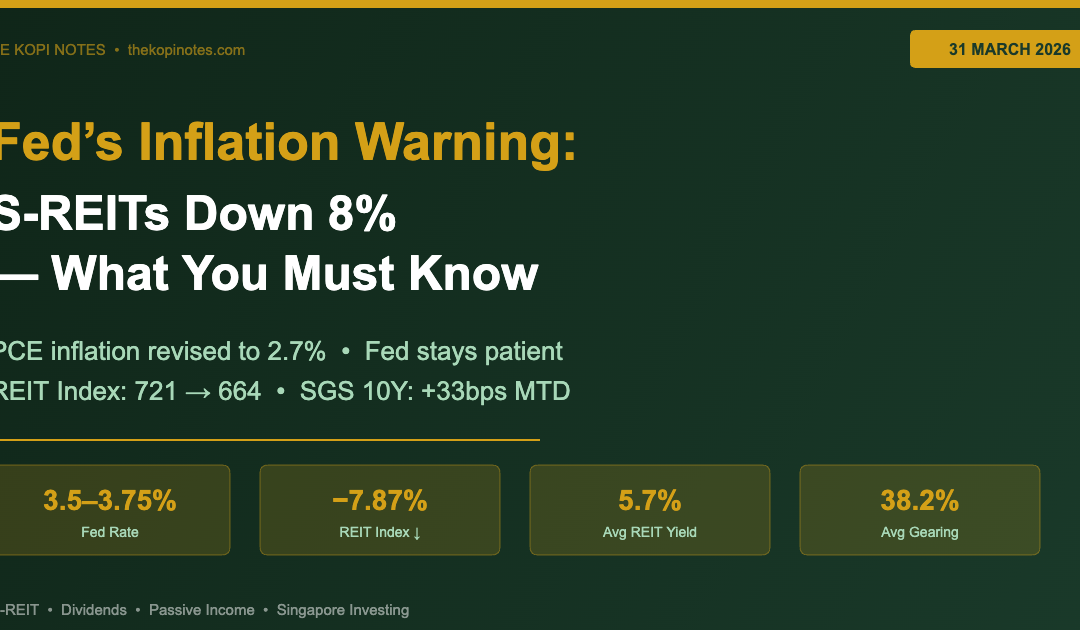

The US Federal Reserve held interest rates steady at 3.5–3.75% at its March 2026 meeting — but the headline wasn’t the hold. It was the inflation upgrade. The Fed now sees PCE inflation hitting 2.7% in 2026, up from 2.4% in December 2025. For Singapore dividend stocks and S-REIT investors, this “higher for longer” signal just got louder.

The FTSE ST All-Share REIT Index has fallen nearly 8% over the past two months. If you’re holding S-REITs or building a passive income portfolio in Singapore, here’s exactly what’s happening — and what to do about it.

What Happened

At its 19 March 2026 meeting, the Federal Open Market Committee (FOMC) kept the federal funds rate unchanged at 3.5–3.75% — the second consecutive hold after three rate cuts in 2025. But buried in the updated Summary of Economic Projections was a critical revision: the Fed now expects headline PCE inflation at 2.7% for 2026, up 0.3 percentage points from December’s forecast of 2.4%. Core PCE inflation was also revised up 0.2 percentage points to 2.7%.

Fed Chair Powell struck a patient tone, signalling no rush to cut further. Markets read the message clearly. The US 10-year Treasury yield climbed to around 4.34% by 26 March 2026, while Singapore’s 10-year government bond yield rose 33 basis points month-to-date to 2.29%.

The FTSE ST All-Share REIT Index fell from 721.34 to 664.56 — a drop of nearly 8% in two months — while the broader Straits Times Index fell only around 2% in the same period. Singapore dividend stocks in the REIT sector bore the brunt.

Sources: FRED Blog – FOMC SEP March 2026; Growbeansprout – S-REITs March 2026 Update

What It Means for S-REIT and Singapore Dividend Investors

The Interest Rate Sensitivity Problem

S-REITs are fundamentally rate-sensitive instruments. They borrow to acquire properties, and higher rates mean two things: borrowing costs go up, and fixed-income alternatives (like Singapore Savings Bonds or T-bills) become more competitive. When the 10-year Singapore government bond yields 2.29% — and looks set to push higher — a REIT needs to offer a meaningfully larger yield to attract capital.

Currently, Singapore dividend stocks in the REIT space offer an average market cap-weighted yield of approximately 5.7%. That’s a spread of roughly 3.4% over the 10-year SGS bond. Historically, a healthy spread is 3–5%. We’re still within range, but the direction is uncomfortable: if bond yields rise another 30–50 basis points, REIT prices will need to fall further to maintain the spread.

Gearing: The Number That Matters

The average gearing ratio across S-REITs is approximately 38.2% — well below the MAS regulatory cap of 50%. This is a structural safety net: most REITs are not in danger of forced asset sales or distribution cuts from gearing alone. However, gearing matters at renewal. REITs with large chunks of debt maturing in 2026 and 2027 will refinance at higher rates than their current hedged positions.

The key metric to watch is the Interest Coverage Ratio (ICR). MAS requires S-REITs to maintain an ICR of at least 1.5x to gear above 45%. As borrowing costs rise, ICR compresses — limiting management’s flexibility. REITs with ICRs below 2.5x are at higher risk of distribution per unit (DPU) cuts if rates remain elevated.

Sector Breakdown: Who Benefits, Who Suffers

Industrial & Logistics REITs — Relatively resilient. Leases are often on 3–5 year fixed terms with built-in CPI-linked rental escalation clauses, which actually benefit from higher inflation. Data centre demand remains structurally strong due to AI infrastructure buildout. Key names: Mapletree Industrial Trust (MIT), Mapletree Logistics Trust (MLT), Keppel DC REIT.

Retail REITs — Mixed. Singapore retail fundamentals remain solid — Orchard Road occupancy is above 95% — but higher consumer borrowing costs may dampen discretionary spending over the medium term. Key names: Frasers Centrepoint Trust (FCT), CapitaLand Integrated Commercial Trust (CICT).

Office REITs — Under most pressure. Hybrid work has reduced office demand in key Western markets, and Singapore Grade A office rents have plateaued. Higher refinancing costs compound the issue on long-duration assets. Key names: Keppel REIT, OUE REIT. Both face headwinds from rising interest costs and refinancing pressure.

Hospitality REITs — Near-term resilient, long-term dependent on global travel trends. RevPAR remains healthy post-COVID recovery, but these are cyclical assets with floating-rate debt exposure. Key names: CDL Hospitality Trusts, Far East Hospitality Trust.

For a full comparison of the best S-REITs by yield and gearing, see our deep-dive: Best S-REITs in Singapore 2026. Prefer a diversified approach? Our Singapore REIT ETF Guide compares the top passive options.

What About CPF?

If you’re invested in S-REITs through the CPF Investment Scheme (CPFIS), the rising rate environment has a silver lining: the CPF Ordinary Account (OA) rate currently sits at 2.5% per annum (floor rate), and the Special Account (SA) earns 4% per annum. With S-REITs underperforming, the safe harbour of leaving CPF funds in the OA or SA looks more attractive in the short term.

That said, if you have a long investment horizon (10+ years), temporarily lower REIT prices can represent a better entry point for CPFIS-eligible S-REITs. The key is to select REITs with low gearing, strong ICR, and long weighted average debt expiry (WADE) — these are best positioned to weather the rate cycle. For a full breakdown of how to optimise your CPF for investments, read our CPF Investment Strategy guide.

Our Take

The Fed’s inflation upgrade is a real headwind for S-REITs — but not a crisis. The sector’s average gearing of 38% and the MAS 50% regulatory cap provide meaningful cushion. The real risk is for REITs with debt maturing in the next 12–18 months at low hedged rates: watch for DPU revisions in mid-2026 results announcements.

For long-term Singapore dividend investors, the current pullback is creating selective entry opportunities — especially in industrial and logistics REITs with CPI-linked leases and data centre exposure. We’d be cautious on pure office plays until there’s clearer visibility on refinancing costs.

If you’re building a passive income portfolio in Singapore, platforms like Endowus offer cost-efficient access to diversified REIT and income funds — worth considering as part of a barbell strategy combining individual S-REIT picks with broader exposure.

Frequently Asked Questions

Why are S-REITs falling even though the Fed didn’t raise rates?

Which S-REITs are most vulnerable to higher interest rates?

Should I buy S-REITs now or wait for a better price?

What is the current average S-REIT yield in Singapore?

How do US tariffs on Singapore affect S-REITs?

Conclusion

The Fed’s March 2026 inflation revision has reset rate cut expectations and pushed bond yields higher globally — including in Singapore. S-REITs have absorbed most of the blow, falling nearly 8% over two months. For Singapore dividend investors, the short-term pain is real, but the long-term income thesis for quality S-REITs remains intact.

Focus on REITs with low gearing, long debt maturity profiles, and resilient sector fundamentals — particularly industrial, logistics, and data centre plays. Stay cautious on pure office exposure until the refinancing cycle clears.

Explore further: Best S-REITs Singapore 2026 | REIT ETF Guide Singapore | CPF Investment Strategy

Disclaimer: This is not financial advice. Data as at 31 March 2026. Please consult a licensed financial adviser before making any investment decisions. Past performance is not indicative of future results.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.