CPF LIFE Singapore 2026: Complete Guide to Plans, Payouts & How to Maximise Your Retirement Income

Your CPF LIFE plan determines how much you receive every month — for the rest of your life. Here’s everything you need to know.

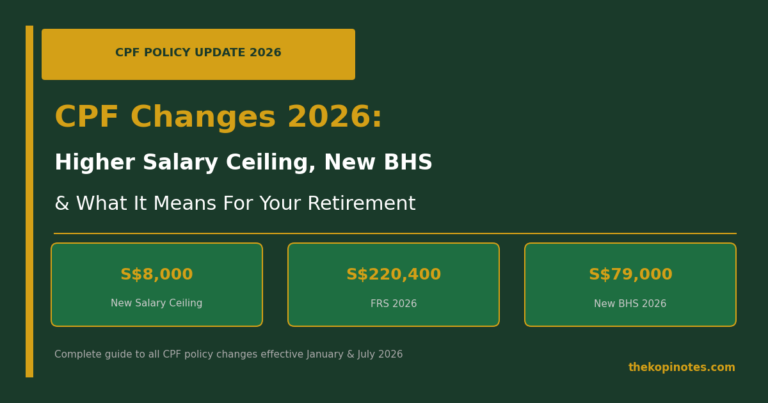

CPF LIFE (Lifelong Income For the Elderly) is Singapore’s national longevity annuity scheme that pays you a guaranteed monthly income from age 65 until you die. Introduced in 2009 and mandatory for members who turn 55 with at least S$60,000 in their Retirement Account, CPF LIFE offers three plans — Standard, Basic, and Escalating — each with different payout levels and bequest amounts. Under the 2026 Enhanced Retirement Sum (ERS) of S$426,000, a member who tops up to the ERS on the Standard Plan can receive approximately S$3,330–S$3,570 per month from age 65.

Not financial advice. All figures are for educational reference only. CPF payout estimates are based on CPF Board projections as at May 2026 and may vary based on actual interest credited. Always verify at cpf.gov.sg.

What Is CPF LIFE?

CPF LIFE stands for Lifelong Income For the Elderly. It is Singapore’s mandatory national longevity annuity scheme, administered by the CPF Board. Unlike the old CPF Retirement Sum Scheme (RSS) — which paid out a fixed amount over a defined period and risked outliving your savings — CPF LIFE guarantees monthly payouts for as long as you live, no matter how long that is.

CPF LIFE was introduced in 2009 and became the default scheme for members turning 55 from 2013 onwards. Today, any CPF member who reaches 55 with at least S$60,000 in their combined CPF accounts is automatically enrolled. Those with less may be placed under the older RSS, though they can opt into LIFE voluntarily.

How Does CPF LIFE Work?

Here’s the simplified flow:

- At age 55: A Retirement Account (RA) is created. CPF transfers money from your Special Account (SA) and Ordinary Account (OA) to fill it up to the applicable retirement sum level.

- From 55 to 65: Your RA continues to earn 4% per annum interest (with an extra 1% on the first S$30,000 and extra 2% on the first S$30,000 for members aged 55–65). The balance compounds.

- At age 65 (or up to 70 if you defer): CPF LIFE payouts begin. Your RA premium is transferred to the CPF LIFE annuity pool, and you receive a fixed monthly income.

- For life: Payouts continue every month until death. The longevity risk is pooled across all members — those who live shorter lives subsidise those who live longer ones.

The key insight: CPF LIFE is longevity insurance. It protects against the risk of outliving your savings. For a Singapore woman who retires at 65 today, median life expectancy is approximately 89 — meaning the average woman will draw CPF LIFE for 24 years. At S$1,500/month, that’s S$432,000 in total payouts from a premium of perhaps S$166,000 (Basic Retirement Sum). The pooling mechanism makes this work.

The Three CPF LIFE Plans Compared

CPF LIFE offers three plans. All provide lifelong income — they differ in how much you receive monthly and how much is left for your beneficiaries when you pass away.

| Feature | Standard Plan | Basic Plan | Escalating Plan |

|---|---|---|---|

| Monthly Payout Level | Highest fixed payout | Lower fixed payout | Starts low, rises 2%/yr |

| Bequest (Death Benefit) | Lower bequest | Higher bequest | Lower bequest |

| Best For | Max monthly income, less concern for legacy | Leaving more for heirs | Inflation hedge; younger retirees |

| Inflation Protection | None (fixed nominal) | None (fixed nominal) | Yes — 2% annual increase |

| Default? | Yes — default plan | Must opt in | Must opt in |

Source: CPF Board, May 2026

Standard Plan — The Most Popular Choice

The Standard Plan is the default and the most widely chosen. It converts the bulk of your Retirement Account premium into the LIFE annuity pool, giving you the highest monthly payout. The trade-off: less money remains in your RA for bequest purposes. If you die early (before drawing down the full premium), only the unused RA balance is returned to your estate — not the full premium transferred to the pool.

For most Singaporeans who prioritise income in retirement over leaving a legacy, the Standard Plan is the right choice.

Basic Plan — Higher Bequest, Lower Monthly Income

The Basic Plan keeps more of your RA premium in a ring-fenced balance that forms the bequest. Your monthly payout is lower — roughly S$100–S$200 less per month at Full Retirement Sum level — but more is preserved for your beneficiaries if you die early. The Basic Plan suits members with dependants who want to ensure a meaningful legacy, or those who have other income sources (rental, dividends) and value the estate component more than the marginal payout difference.

Escalating Plan — Built-In Inflation Protection

The Escalating Plan starts with a payout roughly 20% lower than the Standard Plan, but increases 2% each year. After approximately 10 years, it overtakes the Standard Plan in cumulative value, assuming equal premiums. This plan suits members who:

- Retire early (age 65) and expect to live into their 80s or 90s

- Are concerned about the long-term erosion of purchasing power from inflation

- Have other assets (CPF OA, SRS, investments) to bridge the lower payouts in early retirement years

The Escalating Plan is underused in Singapore but mathematically superior for longevity-optimised planning if you can afford the lower initial payout.

CPF LIFE Payout Amounts 2026

CPF LIFE payout amounts depend on: (1) your RA balance at age 55, (2) the plan you choose, (3) when you start payouts (65–70), and (4) interest credited from 55 to payout start. The figures below are CPF Board estimates for members who turn 55 in 2026 with the stated RA balance at age 55, starting payouts at age 65 on the Standard Plan.

| RA Balance at 55 | Retirement Sum Level | Standard Plan (from 65) | Basic Plan (from 65) | Escalating Plan (from 65) |

|---|---|---|---|---|

| S$106,500 | Basic (BRS) | ~S$850–S$910/mo | ~S$730–S$790/mo | ~S$680–S$730/mo |

| S$213,000 | Full (FRS) | ~S$1,650–S$1,750/mo | ~S$1,430–S$1,520/mo | ~S$1,320–S$1,400/mo |

| S$426,000 | Enhanced (ERS) | ~S$3,330–S$3,570/mo | ~S$2,860–S$3,050/mo | ~S$2,660–S$2,850/mo |

Source: CPF Board CPF LIFE estimates, May 2026. Figures are illustrative ranges based on interest rate scenarios of 3.5%–4.5% p.a. Actual payouts may differ. BRS = S$106,500; FRS = S$213,000; ERS = S$426,000 (2026 figures).

A useful way to think about it: every S$100,000 in your RA at 55 translates to roughly S$770–S$840 per month under the Standard Plan from age 65, assuming 4% interest over 10 years. This ratio is a handy mental shortcut for planning.

To get a personalised estimate, use our CPF LIFE payout calculator Singapore — it runs the same calculation methodology as the CPF Board’s estimator with 2026 retirement sum figures.

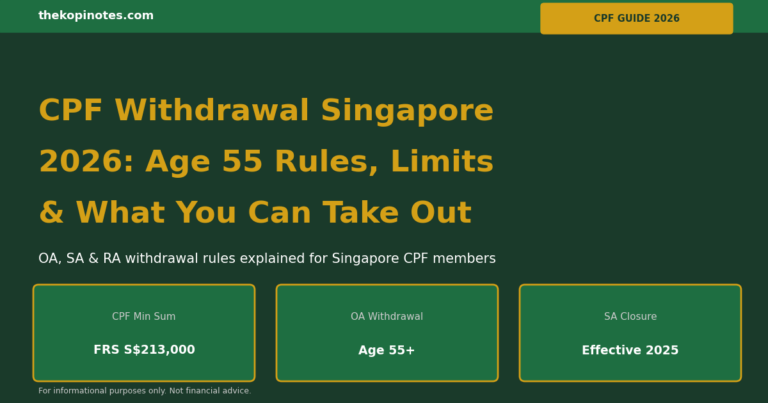

Retirement Sums 2026: BRS, FRS & ERS Explained

The CPF Board sets three retirement sum benchmarks annually. These determine how much you need in your RA to qualify for different payout tiers:

| Retirement Sum | 2026 Amount | vs 2025 | Monthly Payout Range (Standard, from 65) |

|---|---|---|---|

| Basic Retirement Sum (BRS) | S$106,500 | +3.4% (↑ S$3,500) | ~S$850–S$910/mo |

| Full Retirement Sum (FRS) | S$213,000 | = 2× BRS | ~S$1,650–S$1,750/mo |

| Enhanced Retirement Sum (ERS) | S$426,000 | = 4× BRS (raised from 3× in 2025) | ~S$3,330–S$3,570/mo |

Source: CPF Board, Singapore Budget 2025/2026 announcements. The ERS was raised from 3× BRS to 4× BRS effective January 2025 to allow higher voluntary top-ups for members seeking larger payouts.

The ERS increase from 3× to 4× BRS (announced in Budget 2024 and effective 2025) is one of the biggest CPF changes in recent years. Members who were previously capped at 3× BRS can now top up a further ~S$107,000 to unlock the 4× ERS payout tier. For a 55-year-old who can afford to top up, this translates to an additional ~S$1,680–S$1,820 per month for life — a remarkable annuity rate that private insurers cannot match. See our full guide to CPF changes 2026 for the complete salary ceiling and BHS updates.

Understanding these figures also helps with your broader CPF investment strategy — knowing how much your RA will generate at retirement lets you plan how much supplementary income you need from dividends, REITs, or an SRS drawdown.

How to Maximise Your CPF LIFE Payout

There are four proven strategies to increase your monthly CPF LIFE payout:

Strategy 1: Top Up Your Retirement Account (RA Cash Top-Up)

You can make voluntary cash top-ups to your RA under the Retirement Sum Topping-Up (RSTU) scheme. Every dollar topped up before 55 earns 4% p.a. in your SA (which transfers to RA at 55), and every dollar in your RA earns 4% p.a. until payouts begin. A top-up of S$10,000 at age 45 (20 years before payouts at 65) compounds to approximately S$21,900 by age 65 — translating to roughly S$169/month in additional lifetime income.

Cash top-ups under the RSTU scheme also attract tax relief of up to S$8,000 per year (S$8,000 for self, S$8,000 for family members). This makes RA top-ups one of the most tax-efficient ways to grow your retirement nest egg. Use our CPF cash top-up tax relief calculator to see your exact tax savings.

Strategy 2: Defer Your Payout Start Age (Up to 70)

You do not have to start CPF LIFE payouts at 65. You can defer up to age 70. For every year you defer, your monthly payout increases by approximately 6–7%. Deferring from 65 to 70 (5 years) boosts your monthly payout by roughly 35%. This is equivalent to an annuity uplift that is essentially impossible to replicate with any private investment.

The maths for a S$213,000 FRS holder on the Standard Plan:

- Start at 65: ~S$1,700/month

- Defer to 67: ~S$1,930/month (+14%)

- Defer to 70: ~S$2,300/month (+35%)

Deferral suits members who have other income (SRS withdrawals, dividends from an income-generating portfolio, or part-time work) to bridge the 65–70 gap.

Strategy 3: Top Up to the Enhanced Retirement Sum (ERS)

The ERS is now S$426,000 — 4× the BRS. Members who top up from FRS to ERS unlock the highest available CPF LIFE payout bracket. For someone turning 55 in 2026 with exactly S$213,000 FRS who tops up an additional S$213,000 in cash to reach ERS, the monthly payout under the Standard Plan roughly doubles — from ~S$1,700 to ~S$3,400/month at age 65.

This is only feasible for members with significant liquid savings or those inheriting assets. But for those who qualify, it offers a risk-free, government-guaranteed annuity at a rate that vastly exceeds comparable commercial products.

Strategy 4: Choose the Right Plan for Your Situation

Most members default to the Standard Plan — and for most, that’s correct. But if you:

- Have dependants you want to provide for → consider Basic Plan

- Retire at 65, are in good health, and fear inflation → consider Escalating Plan

- Have other assets providing income → deferring + Escalating Plan is a powerful combination

You can check CPF LIFE estimates and switch plans using the CPF Board’s digital services at cpf.gov.sg before your payout start date.

CPF LIFE vs Private Annuities

Singapore’s insurance market offers private life annuities from insurers like Great Eastern, Manulife, NTUC Income, and AIA. How does CPF LIFE compare?

| Factor | CPF LIFE | Private Annuity |

|---|---|---|

| Payout Rate | ~7–8% of premium/year (at FRS) | ~4–6% of premium/year |

| Government Guarantee | Yes — backed by Singapore Government | No (SDIC covers up to S$500k) |

| Inflation Option | Escalating Plan (+2%/yr) | Some products offer CPI-linked payouts |

| Flexibility | Limited (plan choice, deferral) | Higher (riders, joint life options) |

| Tax Treatment | Top-up eligible for tax relief | SRS withdrawals taxed at concessionary rate |

| Verdict | Better value for most Singaporeans | Useful complement for joint-life needs |

Source: MAS Moneyowl annuity comparisons, insurer product sheets, May 2026. Payout rates are indicative based on a 65-year-old male, S$200,000 premium.

The verdict is clear: CPF LIFE offers significantly better payout rates than private annuities for a given premium, with the added security of a government guarantee. The recommended approach for most Singaporeans is to maximise CPF LIFE first, then supplement with SRS investments in income funds or S-REITs via platforms like Endowus or Syfe for additional retirement income.

Should You Defer CPF LIFE Payouts?

Deferring your CPF LIFE payout start date is one of the most impactful decisions you can make in retirement planning. Here’s a worked example for a member with S$213,000 (FRS) in their RA at age 55 on the Standard Plan:

- Start at 65: Estimated ~S$1,700/month. If they live to 85 (20 years), total payouts ≈ S$408,000

- Defer to 70: Estimated ~S$2,300/month. If they live to 85 (15 years), total payouts ≈ S$414,000 — but with S$600/month more in the higher-cost later years

- Defer to 70 and live to 90: Total payouts ≈ S$552,000 vs S$510,000 starting at 65 — S$42,000 more, and more money when healthcare costs peak

The break-even age for deferral (65 to 70) is approximately 80–82 years old. Given Singapore’s median life expectancy of 84 (male) and 87 (female), the odds strongly favour deferring for most members — especially women and those in good health.

The caveat: deferring only makes sense if you can fund living expenses from 65–70 without drawing down the CPF LIFE payout. Members with SRS balances can use SRS withdrawals during this window — at a tax-advantaged rate. Planning this bridge requires a holistic view of your retirement assets, which our Singapore retirement planning calculator can help model.

Tools & Resources

Use these TKN tools to model your CPF LIFE retirement income:

- CPF LIFE Payout Calculator Singapore — estimate your monthly payout at BRS, FRS, or ERS levels

- Retirement Planning Calculator Singapore — model your total retirement income from CPF LIFE + investments

- CPF Retirement Sum Calculator — check how much you’ll have in your RA at 55 based on current balances

- CPF Cash Top-Up Tax Relief Calculator — calculate your tax savings from RA top-ups

- SRS Tax Savings Calculator — plan your SRS contributions alongside CPF LIFE deferral

For official CPF LIFE estimates, log in to cpf.gov.sg and use the CPF LIFE Estimator under “My Retirement” dashboard.

Frequently Asked Questions About CPF LIFE

”What

”How

”Can

”What

”Should

”Is

”What

Ready to Plan Your CPF LIFE Strategy?

CPF LIFE is the foundation of retirement income for most Singaporeans. Maximise it first — then layer in investments for supplementary income. For a managed, low-cost approach to growing your SRS and cash savings alongside CPF LIFE, explore Endowus and Syfe — two of Singapore’s top robo-advisors for retirement planning.

CPF LIFE monthly payout estimates by plan and retirement sum level. Source: CPF Board, May 2026.

Deferring CPF LIFE payouts from 65 to 70 boosts monthly income by ~35% for FRS holders. Source: CPF Board estimates, May 2026.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.