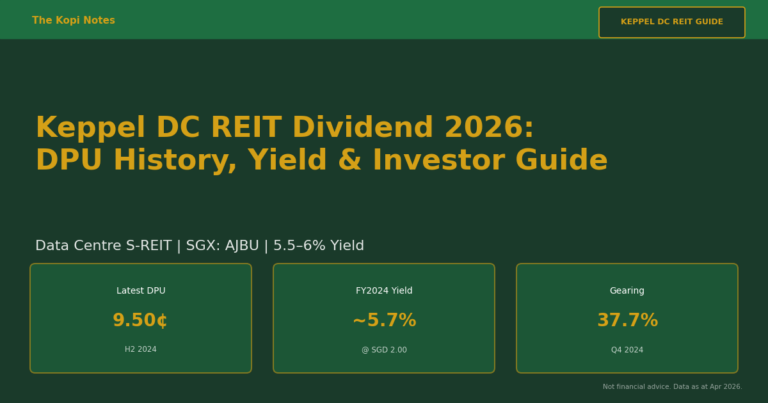

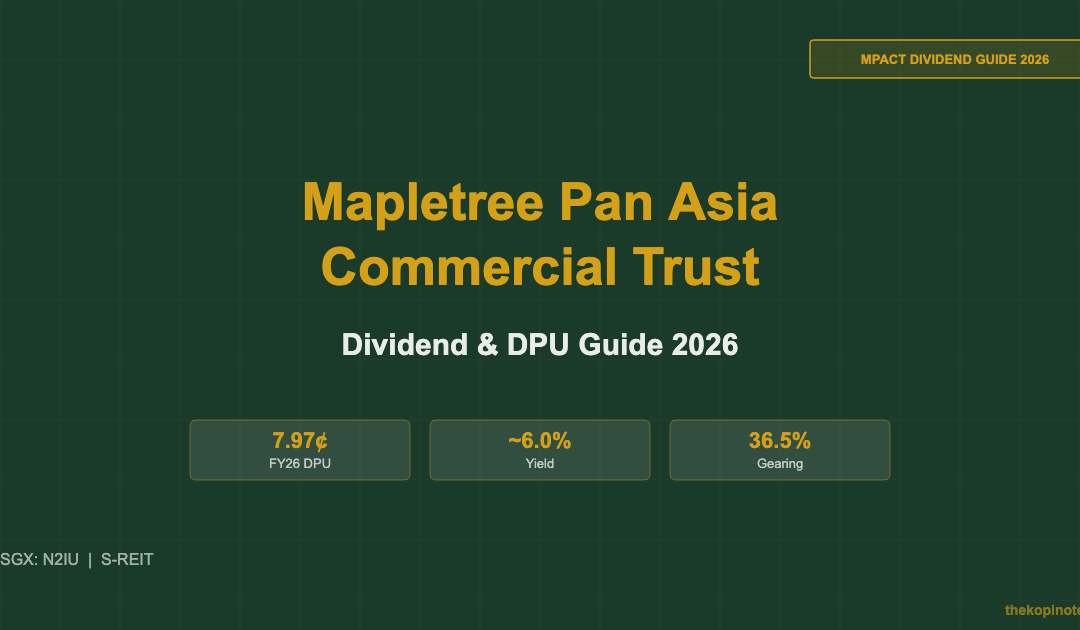

Mapletree Pan Asia Commercial Trust Dividend & DPU Guide 2026 (SGX: N2IU)

7.97¢ FY2026 DPU | ~6.0% Yield | Gearing 36.5% | VivoCity Anchor

Mapletree Pan Asia Commercial Trust (MPACT, SGX: N2IU) paid a full-year FY2025/26 DPU of 7.97 Singapore cents, a distribution yield of approximately 6.0% at the current share price of S$1.33. Singapore’s largest diversified commercial REIT, anchored by VivoCity mall and Mapletree Business City, manages S$15.2 billion in assets across five Asian gateway markets. Dividend income is paid quarterly, making MPACT a popular choice for income-seeking investors using CPF or SRS funds.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

Table of Contents

Table of Contents

- What Is MPACT and What Does It Own?

- MPACT DPU History FY2019-FY2026

- FY2025/26 Full-Year Results Deep-Dive

- VivoCity: The Crown Jewel Driving Distributions

- Is MPACT Dividend Sustainable?

- MPACT vs S-REIT Peers: Yield and Gearing

- How to Buy MPACT: CPF, SRS and Broker Guide

- Analyst Target Prices and Verdict

- Frequently Asked Questions

What Is MPACT and What Does It Own?

Mapletree Pan Asia Commercial Trust (MPACT) is a Singapore-listed REIT owning 15 commercial properties across Singapore, Hong Kong, China, Japan, and South Korea. Formed in 2022 through the merger of Mapletree Commercial Trust and Mapletree North Asia Commercial Trust, it is one of the largest diversified commercial REITs in Asia by asset value with AUM of S$15.2 billion. Singapore now comprises 61% of AUM and 66% of NPI following strategic divestments.

| Property | Type | GFA (sq ft) | Occupancy (FY26) |

|---|---|---|---|

| VivoCity | Retail | 1,075,700 | 99.7% |

| Mapletree Business City | Office/Business Park | 2,700,000 | 94.6% |

| mTower | Office | 483,500 | 93.2% |

| Mapletree Anson | Office | 311,200 | 93.8% |

Source: MPACT FY2025/26 Annual Results Presentation, April 2026

MPACT divested three non-core overseas assets in FY2025/26 (Festival Walk Tower, TSI, ASY), raising S$328.1 million applied entirely to debt reduction. The Festival Walk retail mall (100% committed, 588,890 sq ft) is retained.

MPACT DPU History FY2019-FY2026

MPACT was formed in November 2022 through the merger of Mapletree Commercial Trust (MCT) and Mapletree North Asia Commercial Trust (MNACT). Pre-merger figures below reflect MCT for continuity.

| Financial Year | DPU (¢) | YoY Change | Key Driver |

|---|---|---|---|

| FY2019 (MCT) | 9.04¢ | – | Steady VivoCity and MBC growth |

| FY2020 (MCT) | 8.97¢ | -0.8% | COVID-19 rental relief |

| FY2021 (MCT) | 8.77¢ | -2.2% | Extended COVID restrictions |

| FY2022 (MCT) | 9.32¢ | +6.3% | Post-COVID reopening |

| FY2023 (MPACT) | 9.61¢ (peak) | +3.1% | First full merged year; strong SG |

| FY2024 | 8.91¢ | -7.3% | Rising finance costs; overseas weakness |

| FY2025 | 8.02¢ | -10.0% | Higher borrowing costs; HK/CN/JP headwinds |

| FY2026 | 7.97¢ | -0.6% | One-off S$8.3M tax charge (FW Tower); underlying stable |

Source: MPACT/MCT Annual Reports, SGX Announcements. FY2019-FY2022 reflect Mapletree Commercial Trust (pre-merger) for continuity.

The FY2026 DPU dip is explained by a one-off S$8.3 million tax charge from the Festival Walk Tower divestment. Excluding this, underlying distributable income was marginally higher YoY. Finance expenses also fell sharply (-15.3% to S$186.8M), reflecting debt paydown from divestment proceeds and lower benchmark rates.

FY2025/26 Full-Year Results Deep-Dive

| Metric | FY2025/26 | FY2024/25 | YoY |

|---|---|---|---|

| Gross Revenue | S$867.3M | S$908.8M | -4.6% |

| Net Property Income | S$654.4M | S$683.5M | -4.3% |

| Finance Expenses | S$186.8M | S$220.4M | -15.3% |

| Distributable Income | S$421.4M | S$423.0M | -0.4% |

| Full-Year DPU | 7.97¢ | 8.02¢ | -0.6% |

| Aggregate Leverage | 36.5% | ~38.5% | Improved |

| Cost of Debt | 3.16% p.a. | ~3.60% p.a. | Improved |

| ICR | 3.2x | 2.8x | +0.4x |

| NAV per Unit | S$1.73 | S$1.78 | -2.8% |

| Portfolio Occupancy | 89.4% | ~89.0% | Stable |

Source: MPACT FY2025/26 Results Announcement, 28 April 2026.

The standout improvement is the 15.3% fall in finance expenses to S$186.8M, a direct result of repaying debt with divestment proceeds. The ICR improvement from 2.8x to 3.2x provides a meaningful buffer above the MAS minimum of 1.5x. For income investors, balance sheet improvement matters more than the modest DPU headline decline.

VivoCity: The Crown Jewel Driving Distributions

VivoCity is Singapore largest suburban mall by GFA and the most important asset in MPACT portfolio. In FY2025/26, VivoCity delivered a 7.6% increase in full-year NPI and a 14.1% rental uplift on renewed leases – the strongest performance among all MPACT properties. Committed occupancy remained near-full at 99.7%.

The manager has proactively undertaken asset enhancement initiatives (AEIs) at VivoCity, consistently adding experiential dining, fitness, and entertainment tenants that attract Singapore growing tourism footfall. The Harbourfront MRT integration (Circle Line) provides captive commuter traffic that many suburban malls cannot replicate.

For MPACT dividend story, VivoCity sustained outperformance means the Singapore portfolio can absorb shocks from overseas assets. Singapore now contributes 66% of NPI and this weighting is expected to increase further. Mapletree Business City (MBC) also demonstrated resilience with 94.6% occupancy, well above Singapore CBD office vacancy rates of around 10-12% cited by CBRE and JLL for H1 2026.

Is MPACT Dividend Sustainable in 2026?

Three key factors drive the DPU outlook. First, Finance Cost Tailwind (Positive): cost of debt fell to 3.16% in FY2026, down from peak of around 3.8%. Every S$10M reduction in annual interest cost adds approximately 0.20c to DPU. Second, Overseas Portfolio Drag (Risk): remaining overseas assets face HKD/JPY/KRW/RMB translation losses against SGD and softer local property markets. Third, Singapore Rental Reversion (Positive): MPACT achieved portfolio rental reversions of +5.9% in FY2026, led by VivoCity +14.1%. With Singapore resident employment near record highs (MOM, mid-2026), positive reversions should continue into FY2027.

| Scenario | Est. FY2027 DPU | Yield @ S$1.33 | Key Assumption |

|---|---|---|---|

| Bear | 7.50¢ | 5.6% | Further overseas weakness; SG flat |

| Base | 8.10¢ | 6.1% | Finance savings offset overseas drag; VivoCity steady |

| Bull | 8.50¢ | 6.4% | Finance costs fall sharply; VivoCity +10% NPI; HKD stabilises |

Illustrative scenarios for educational purposes only. TKN analysis based on MPACT FY2026 results, June 2026.

MPACT vs S-REIT Peers: Yield, Gearing and Dividend Coverage 2026

MPACT ~6.0% yield sits in the middle of the Singapore commercial REIT pack – higher than CICT and FCT, but below highly leveraged or offshore-exposed peers like Keppel REIT or OUE REIT. At 36.5% gearing, MPACT has one of the lowest leverage ratios among its peers.

| REIT | SGX | Type | Yield | Gearing | ICR |

|---|---|---|---|---|---|

| MPACT | N2IU | Commercial/Retail | 6.0% | 36.5% | 3.2x |

| CICT | C38U | Retail/Office | 5.5% | 39.6% | 3.3x |

| Frasers Centrepoint Trust | J69U | Retail (SG) | 5.9% | 38.8% | 3.5x |

| Keppel REIT | K71U | Office | 7.1% | 40.2% | 2.9x |

| OUE REIT | TS0U | Commercial/Hosp. | 7.2% | 35.5% | 2.8x |

| Suntec REIT | T82U | Office/Retail/Conv. | 6.8% | 42.0% | 2.5x |

| Starhill Global REIT | P40U | Retail (SG/Overseas) | 6.8% | 35.5% | 3.0x |

Source: Company reports, SGX disclosures, analyst estimates, June 2026. ICR figures are approximate. Not investment advice.

For a full sector comparison, see best S-REITs in Singapore 2026. Use the Singapore retirement calculator to model MPACT quarterly distributions in your income plan. For S-REIT fund exposure, explore the Singapore REIT ETF guide covering the Lion-Phillip CLR ETF which holds MPACT as a top constituent.

How to Buy MPACT in Singapore: CPF, SRS and Broker Guide

MPACT (N2IU) is listed on the SGX Mainboard and is CPFIS-OA eligible. CPF members can invest up to 35% of investible CPF OA savings (balance above S$20,000) in MPACT. For a Singapore investor with S$100,000 in investible CPF OA funds, allocating S$30,000 to MPACT at S$1.33 (approximately 22,500 units) generates around S$1,800 in annual distribution income at 7.97c DPU – significantly above the 2.5% CPF OA floor rate.

| Broker | Commission | CPF/SRS | Min. Fee | Referral Code |

|---|---|---|---|---|

| FSMOne | 0.08% | Yes (CPF and SRS) | S$10 | P0544985 |

| Endowus | Fund-based | Yes (CPF and SRS) | 0.25% p.a. | 2V343 |

| Syfe | From 0% | SRS only | Nil | SRPRFFFCD |

| IBKR | S$1.50 flat | Cash only | S$1.50 | jianxiong368 |

Source: Broker fee schedules, June 2026. Rates subject to change. TKN may earn referral fees.

For passive income planning, see passive income in Singapore 2026. Optimise your CPF strategy at the CPF investment strategy guide.

Analyst Target Prices and Verdict 2026

Analyst consensus target price for MPACT as at June 2026 is approximately S$1.56-S$1.57, implying ~17-18% upside from S$1.33. MPACT trades at a P/NAV of approximately 0.77x (price S$1.33 vs NAV S$1.73) – among the widest discounts in blue-chip Singapore commercial REITs.

| Broker | Rating | Target Price | Upside |

|---|---|---|---|

| Maybank Research | BUY | S$1.50 | +12.8% |

| CGS International | ADD | S$1.52 | +14.3% |

| Consensus Average | BUY | S$1.56-S$1.57 | ~17% |

Source: MarketScreener, SGinvestors.io analyst consensus, June 2026.

TKN Verdict: HOLD / Selective BUY. MPACT FY2026 DPU dip was a one-off; the underlying picture is more constructive. Lower gearing (36.5%), lower cost of debt (3.16%), stronger ICR (3.2x), and Singapore delivering consistent rental uplifts all point to improved distribution quality. Existing holders: HOLD at ~6% yield with improving balance sheet. New investors: Selective BUY at S$1.30-S$1.38, with awareness of overseas FX risk. Not financial advice. Consult a licensed financial adviser before investing.

Frequently Asked Questions

What is MPACT dividend yield in 2026?

As at June 2026, MPACT (SGX: N2IU) offers a trailing dividend yield of approximately 6.0%, based on the FY2025/26 full-year DPU of 7.97 Singapore cents and a share price of around S$1.33. Distributions are paid quarterly. The 4Q FY2025/26 DPU of 1.90c was payable on 17 June 2026.

How often does MPACT pay dividends?

MPACT pays distributions quarterly – four times per year. The typical schedule is August (1Q results), October/November (2Q), January/February (3Q), and June (4Q/full-year). Unitholders must be on the register by the ex-dividend date to qualify.

Why did MPACT DPU fall in FY2026?

The FY2025/26 DPU of 7.97c was 0.6% lower than FY2024/25 8.02c, mainly due to a one-off S$8.3 million tax charge recognised upon completion of the Festival Walk Tower divestment. Excluding this one-off, underlying distributable income would have been marginally higher YoY, supported by reduced finance expenses (-15.3%) and VivoCity +7.6% NPI growth.

Can I buy MPACT using CPF funds?

Yes. MPACT (N2IU) is CPFIS-OA eligible. CPF members can invest up to 35% of investible CPF OA savings (balance above S$20,000) in MPACT through CPFIS-approved brokers such as FSMOne or DBS Vickers. Distributions are received in a designated bank account, not credited back to CPF directly.

What is MPACT gearing and is it safe?

MPACT aggregate leverage stands at 36.5% as at 31 March 2026, well below the MAS regulatory cap of 50%. The ICR is 3.2x, meaning operating income covers interest payments more than three times over. This provides a comfortable buffer against rising rates or income volatility.

What happened to Festival Walk in MPACT portfolio?

MPACT divested the office component of Festival Walk (Festival Walk Tower) and two other non-core overseas assets in FY2025/26, raising S$328.1 million. Proceeds were used to reduce borrowings. MPACT retains full ownership of the Festival Walk retail mall (588,890 sq ft), which remains 100% committed post-divestment.

How does MPACT compare to CICT and Frasers Centrepoint Trust?

MPACT (~6.0% yield, 36.5% gearing) offers higher income than CICT (~5.5%, 39.6%) and FCT (~5.9%, 38.8%), with lower gearing than CICT. The trade-off is that MPACT carries overseas currency exposure (HKD, JPY, KRW, RMB) which introduces FX risk absent from CICT and FCT. Investors seeking pure domestic retail REIT exposure may prefer FCT; those comfortable with a pan-Asia overlay may prefer MPACT for the yield premium.

What are analysts target prices for MPACT in 2026?

Analyst consensus target price as at June 2026 is S$1.56-S$1.57, implying ~17-18% upside from ~S$1.33. Maybank Research rates MPACT BUY (TP S$1.50); CGS International rates it ADD (TP S$1.52). MPACT also trades at P/NAV of ~0.77x, a notable discount to book value of S$1.73.

Is MPACT suitable for retirement income?

MPACT can form part of a retirement income strategy for Singapore investors given its quarterly distributions (~6% yield), CPF/SRS eligibility, and large-cap SGX liquidity. Diversify across REIT sectors and geographies to reduce concentration risk. Use the Singapore retirement planning calculator to model how MPACT quarterly distributions interact with CPF LIFE and other income sources.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.