Is MariBank Safe? What Singapore Users Need to Know (2026)

Is MariBank Safe?

Yes, MariBank is safe for Singapore depositors. It holds a full digital bank licence issued by the Monetary Authority of Singapore (MAS), operates under the Banking Act, and is a member of the Singapore Deposit Insurance Corporation (SDIC) — meaning your deposits are insured up to SGD 100,000 per depositor. Owned by Sea Group (parent of Shopee and Garena), MariBank is subject to the same regulatory requirements as traditional banks in Singapore.

Not financial advice. All figures are for educational reference only. Data as at June 2026 unless noted.

When digital banks first appeared in Singapore, many users understandably asked the same question: “Is this actually safe?” With MariBank, the short answer is yes — but the longer answer reveals why the regulatory framework matters as much as the bank’s financial backing. This guide breaks down everything you need to know about MariBank’s safety, from its MAS licence to its deposit insurance and security features.

MAS Licence and Regulatory Oversight

MariBank Singapore Pte. Ltd. received its full digital bank (retail) licence from MAS — the highest tier of banking licence available in Singapore. This is not the same as a payment services licence or a capital markets licence. A full bank licence means MariBank can take deposits from retail customers and is bound by the Banking Act (Cap. 19), just like DBS, OCBC, and UOB.

MAS announced in December 2020 that Sea Limited (MariBank’s parent company) was one of two successful applicants for full digital bank licences in Singapore. MariBank officially launched its savings account in 2022. As of June 2026, it operates under active MAS supervision, subject to capital adequacy requirements, anti-money laundering (AML) obligations, and regular regulatory reporting.

You can verify MariBank’s licence status directly on the MAS Financial Institutions Directory. Search for “MariBank” to confirm its active full bank licence.

Key Regulatory Facts

| Factor | Detail |

|---|---|

| Regulator | Monetary Authority of Singapore (MAS) |

| Licence Type | Full Digital Bank (Retail) — highest tier |

| Governing Act | Banking Act (Cap. 19), Singapore |

| Parent Company | Sea Limited (NYSE: SE) — Shopee, Garena |

| Launched | 2022 (retail savings account) |

| SDIC Member | Yes — deposits insured up to SGD 100,000 |

Source: MAS Financial Institutions Directory, SDIC member list, June 2026

SDIC Deposit Insurance: Your Money is Protected Up to SGD 100,000

One of the most important safety nets for MariBank customers is the Singapore Deposit Insurance Corporation (SDIC). As a full bank licence holder, MariBank is a compulsory member of SDIC. This means if MariBank were to fail (an extremely unlikely scenario given MAS oversight), your eligible deposits would be insured up to SGD 100,000 per depositor.

This is exactly the same protection you get at DBS, OCBC, and UOB. The SGD 100,000 limit applies per depositor, per bank — meaning if you have SGD 80,000 in MariBank and SGD 80,000 in DBS, both are fully covered separately.

Eligible deposits include savings accounts, fixed deposits, and current accounts in SGD. The SDIC scheme is backed by the Singapore government and has never had to pay out a claim — a reflection of MAS’s robust regulatory framework.

Source: SDIC Singapore, MAS MariBank licence details, June 2026

What SDIC Covers at MariBank

| Account Type | SDIC Coverage | Notes |

|---|---|---|

| MariBank Save (savings) | Yes — up to SGD 100,000 | Fully eligible deposit |

| MariBank FlexiLoan | N/A (loan product) | Loans not covered by SDIC |

| Foreign currency deposits | Not covered | SDIC only covers SGD deposits |

Source: SDIC Singapore eligibility rules, June 2026

MariBank Security Features

Beyond regulatory protection, MariBank uses several layers of in-app security to protect your account and transactions:

Biometric authentication: Face ID and fingerprint login are supported on both iOS and Android. You cannot log in with just a password — multi-factor authentication is required.

Singpass login: MariBank requires Singpass Face Verification for account opening, which links your account to your verified NRIC. This significantly reduces impersonation risk compared to banks that allow sign-up with just email.

Transaction limits and cooling-off periods: New payee transfers have a default 12-hour cooling-off period. You can set daily transfer limits within the app. Large transfers trigger an additional OTP or biometric confirmation.

In-app fraud alerts: MariBank sends real-time push notifications for all transactions. If you don’t recognise a transaction, you can freeze your account instantly from the app — no phone call required.

Anti-scam features: In line with MAS guidelines, MariBank participates in Singapore’s national anti-scam framework, including ScamShield compatibility and the ability to lock accounts from within the app if you suspect you’ve been scammed.

MariBank vs Traditional Banks: Safety Comparison

A common concern is whether a digital bank is as safe as an established bank like DBS or OCBC. From a regulatory standpoint, the protections are identical — same MAS oversight, same Banking Act, same SDIC insurance. The practical differences are operational:

| Feature | MariBank | DBS / OCBC / UOB |

|---|---|---|

| MAS Full Bank Licence | ✅ Yes | ✅ Yes |

| SDIC Insurance (up to SGD 100K) | ✅ Yes | ✅ Yes |

| Physical branches | ❌ App only | ✅ Yes |

| ATM card / cash withdrawal | ❌ No ATM | ✅ Yes |

| Biometric + Singpass login | ✅ Required | ✅ Available |

| Instant account freeze (in-app) | ✅ Yes | ⚠️ Varies by bank |

| Base savings rate (no conditions) | 2.88% p.a. | 0.05% p.a. |

Source: Bank websites, MariBank app, MAS, SDIC, June 2026

The main trade-off with MariBank versus a traditional bank is not safety — it’s physical accessibility. MariBank has no ATMs, no branch network, and no debit card for everyday spending. It works best as a high-yield savings vehicle, not as a primary transaction account. For a comprehensive view of Singapore’s digital banking landscape, see our passive income Singapore guide which covers how digital bank savings fit into a broader wealth-building strategy.

MariBank Interest Rate and Returns (2026)

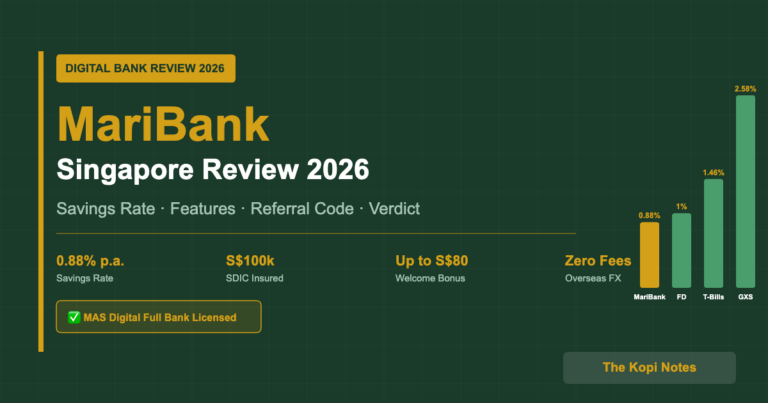

As of June 2026, MariBank’s Save account offers 2.88% p.a. on balances up to SGD 50,000, with no minimum balance requirement and no salary credit condition. This is significantly higher than the base rates of traditional Singapore banks, which typically offer just 0.05% p.a. without fulfilling spending or salary credit conditions.

Source: Bank websites, MariBank app, June 2026. Traditional bank rates shown are unconditional base rates.

To put this in practical terms: a Singapore investor parking SGD 30,000 in MariBank earns approximately SGD 864 per year (SGD 30,000 × 2.88%) with no strings attached. The same amount in a traditional bank savings account at 0.05% p.a. earns just SGD 15 annually.

MariBank rates are variable and can change based on interest rate movements. Use our Singapore retirement calculator to model how high-yield savings contributes to your long-term financial goals. If you want to spread your savings across platforms, the Endowus referral code page covers how to get started with cash management via Endowus, and Syfe referral code and sign-up bonus covers Syfe Cash+ which is another popular cash management option.

MariBank Referral Code (2026)

If you’re opening a MariBank account, use referral code 2DCT80WQ at sign-up to potentially receive a welcome bonus. Referral terms are updated periodically — check the MariBank app for the current offer before applying.

Risks to Be Aware Of

MariBank is safe from a regulatory perspective, but that doesn’t mean it’s risk-free in every sense. Here are the practical risks to consider:

App-only access: If your phone is lost, stolen, or damaged, you need another device to access your funds. There’s no branch you can walk into. This is the most cited inconvenience among MariBank users. The mitigation: set up trusted device recovery options and keep a secondary bank account with a debit card for emergencies.

Variable interest rate: MariBank’s 2.88% p.a. rate is not locked in. If MAS raises or lowers the benchmark rate, MariBank may adjust accordingly. For fixed, locked-in returns, consider Singapore T-bills 2026 or Singapore Savings Bonds which provide guaranteed returns for a fixed term.

Limited product range: As of June 2026, MariBank’s retail product suite is smaller than traditional banks — no investment products, no insurance, no credit cards, no joint accounts. If you need a one-stop banking relationship, a traditional bank remains more comprehensive.

Technology risk: Any digital bank is exposed to system outages and cyberattacks. MariBank has had occasional app downtime, though no significant security breaches have been reported. MAS requires all banks to maintain robust IT resilience standards under its Technology Risk Management Guidelines.

Balance above SGD 100,000: If you hold more than SGD 100,000 in MariBank, the excess is not covered by SDIC. For large cash holdings, consider spreading across multiple MAS-licensed banks, each with their own SGD 100,000 SDIC cover. For amounts above what you need in cash, consider low-cost index ETFs — our Singapore REIT ETF guide covers options for growing long-term wealth beyond savings accounts.

Frequently Asked Questions

Is MariBank safe for deposits?

Is MariBank regulated by MAS?

What happens to my money if MariBank fails?

Who owns MariBank?

What is MariBank's interest rate in 2026?

Can I use MariBank as my main bank account?

What is the MariBank referral code?

Disclaimer: This article is for educational purposes only and does not constitute financial advice. MariBank interest rates are variable and subject to change. Always verify current rates and terms directly with MariBank. The Kopi Notes may receive referral fees from links in this article. Please conduct your own due diligence before making any financial decisions.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.