HOME → GUIDES → INSURANCE

Insurance in Singapore 2026: The Complete Guide

Your authoritative resource for understanding life insurance and investment insurance in Singapore — data-driven analysis, not sales pitches.

Last updated: May 2026 · 15 min read · By The Kopi Notes

📍 Start Here

New to insurance? These are the guides our readers find most useful.

What This Guide Covers

Insurance in Singapore falls into two broad categories that serve fundamentally different purposes. Life insurance — including term life, whole life, and universal life — exists to protect your family financially if you die or become permanently disabled. Investment insurance — including endowment plans and investment-linked policies (ILPs) — combines a smaller protection element with savings or investment components.

The Monetary Authority of Singapore (MAS) regulates all 28 licensed life insurers operating here. As at 2026, Singaporeans can also purchase Direct Purchase Insurance (DPI) through compareFIRST.sg without going through an agent — often at lower premiums.

This hub page provides a high-level overview of both categories and helps you navigate to the detailed guides for each insurance type. We focus on data-driven comparisons, real cost calculations, and practical decision frameworks — not product recommendations.

Not financial advice. All figures are for educational reference only. Data as at May 2026 unless noted.

Insurance Types at a Glance

Life Insurance

Life insurance protects your family’s finances if you die or become permanently disabled. The core question isn’t whether you need it — if anyone depends on your income, you do. The question is what type and how much. Term life gives you the most coverage per dollar. Whole life adds a forced savings component at 5–10x the cost. Universal life offers flexibility but complexity.

Our life insurance guide covers the term vs whole life decision, how to calculate your coverage needs (typically 9–12x annual income), provider comparisons with actual premium quotes, and the DPI option that lets you skip agents entirely.

Investment Insurance

Investment insurance products — ILPs and endowment plans — combine protection with wealth accumulation. The trade-off: higher fees than direct investing, surrender penalties if you exit early, and (for ILPs) market-dependent returns without the cost efficiency of index funds. Endowments offer some guarantees but typically deliver 2–3% p.a. net returns — below what a simple bond portfolio achieves.

Our investment insurance guide breaks down the real costs (including distribution charges, fund management fees, and insurance charges), compares projected returns against ETF and robo-advisor alternatives, and explains the specific scenarios where these products might still make sense.

Which Insurance Type Is Right for You?

Decision Framework

Do you have dependants (spouse, children, elderly parents)?

→ Yes: You need life insurance. Start with term life for maximum coverage per dollar.

Do you want forced savings with guaranteed returns?

→ Consider endowment plans — but compare against SSBs and fixed deposits first.

Do you want market-linked returns with insurance coverage?

→ Read our ILP guide — in most cases, term life + ETFs delivers better outcomes.

Do you need lifetime coverage (e.g., estate planning)?

→ Whole life or universal life may be appropriate. See our life insurance guide.

Are you single with no dependants?

→ You likely don’t need life insurance yet. Focus on health insurance (MediShield Life + IP) and investing directly.

All Insurance Articles

Browse all our insurance guides and analysis.

Insurance Articles

Guides on life insurance, investment insurance, endowment plans, ILPs, and more for Singapore residents.

If nobody relies on your income, life insurance can feel pointless. But "single" doesn't always mean "no financial risk.

Read article

A side-by-side look at endowment plans and Singapore Government Securities (SGS) bonds — with real 2026 rates, worked examples, and who each one actually suits.

Read article

Same $500 a month, two completely different paths -- we ran the actual 20-year numbers.

Read article

Documents, timelines, and payout rules straight from LIA's official claims guidelines

Read article

Both come wrapped in an insurance policy. Only one of them guarantees you anything.

Read article

7 major insurers' whole life plans compared side by side — features, riders, and the real cost vs term life, plus how LIA's illustrated rate caps affect your projected returns.

Read article

Two very different tools that get compared for the wrong reasons — here's how they actually work.

Read article

Two Singapore insurers let you get something back if you outlive your term policy — but they don't pay back the same thing. Here's the difference, with real product terms.

Read article

Endowment plans guarantee ~1.81% p.a., unit trusts offer higher potential returns with market risk. We compare fees, a S$20,000 3-year worked example, and which fits your goals.

Read article

What keeps your life insurance policy alive if you're diagnosed with a critical illness and can't pay the premiums yourself.

Read article

Guaranteed Returns vs Flexible, Liquid Growth — Which Wins for Your Idle Cash?

Read article

A plain-English guide to how TPD riders really work — the age-based definitions, the accelerated payout structure, and what it costs in 2026.

Read article

How to buy up to S$400,000 of term life cover directly from an insurer — no adviser, no commission

Read article

A side-by-side look at endowment plans against globally diversified ETFs like VWRA and CSPX — guaranteed rates, real historical returns, fees, tax, and who should pick which in 2026.

Read article

A Singapore investor's real-numbers comparison of endowment plan guaranteed returns against S-REIT dividend yields, tax treatment, and a worked S$20,000 growth scenario.

Read article

AIA's newest critical illness plan launched in May 2026 — here's what it covers, what it costs, and why it isn't open to everyone.

Read article

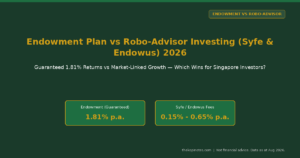

Comparing a guaranteed 1.81% p.a. endowment plan against Syfe and Endowus robo-advisor portfolios — fees, projected growth, and which fits your risk profile in 2026.

Read article

Singapore 2026 — the three fine-print rules that decide if your CI claim actually gets paid

Read article

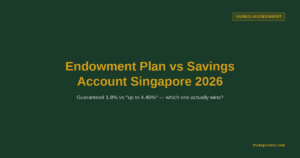

High-yield savings accounts advertise up to 4.45% p.a., but most Singaporeans never hit that rate. Here's the real guaranteed-returns comparison against endowment plans in 2026.

Read article

TPD protection to age 84, four different term plans for four different budgets — here's how Singapore's largest home-grown insurer's term life lineup stacks up.

Read article

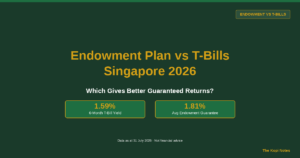

The 6-month T-bill's yield has risen for three straight auctions, hitting 1.59% p.a. on 30 July. The average Singapore endowment plan still guarantees more, at 1.81% p.a.

Read article

Your DPS baseline, the DIME method, and Singapore's S$373 billion protection gap — a step-by-step way to find your real number.

Read article

CPF's Special/Retirement Account floor pays 4% p.a. guaranteed. The average Singapore endowment plan guarantees just 1.8%. Here's the full breakdown — including whether you can actually use CPF to buy one.

Read article

TPD protection to age 86, renewal to 90, and a rider suite that covers early and severe-stage critical illness — here's what Etiqa's flagship term plan gets right, and where it doesn't fit.

Read article

An independent look at Singlife's newest capital-guaranteed savings plan — what it guarantees, what it doesn't, and how it fits after Secure Saver was discontinued.

Read article

GREAT Term 2's real cost vs 4 other insurers, its critical illness rider, and why Singapore's oldest life insurer isn't the cheapest — but might still be worth it.

Read article

A real 2026 premium comparison, and what actually drives the price

Read article

Guaranteed monthly or yearly payouts, plus the real 2023-2025 Par Fund return data Tokio Marine doesn't put on its own product page.

Read article

The LIA's 4x-income rule, real SGD treatment costs, and a step-by-step framework to find your number.

Read article

1.6% p.a. guaranteed over 2 years, 100% capital guarantee at maturity — but the current tranche is sold out. Here's what's inside, and what to do while you wait.

Read article

SaveForward, FlexiCash Growth, and the truth about the "10% guaranteed cash benefit" — verified against China Life's own product pages.

Read article

LIA Singapore's Q1 2026 results reveal the highest first-quarter payout in six years — here's what it means for your coverage

Read article

Etiqa's full savings plan lineup reviewed — capital-guaranteed endowments from just $125/month, with real numbers from official product pages.

Read article

How April 2026’s Integrated Shield Plan rider overhaul shifts your out-of-pocket risk — and what it means for your critical illness coverage.

Read article

Guaranteed capital, real declared bonus rates, and what the reported Allianz sale could mean for your policy.

Read article

PRUActive Term's real cost vs 6 other insurers, its critical illness riders, and when PRUVital Cover or the DIY DIRECT plan beats it on price.

Read article

A plain-English look at AIA's short-term guaranteed #Wealth Savvy tranches and the longer-term Smart Wealth Builder Series, with real numbers pulled straight from AIA's own policy documents.

Read article

CPF's Dependants' Protection Scheme gives you free term life cover — but for most working adults, it covers only a fraction of what their family actually needs.

Read article

Guaranteed 1.70% p.a. over 3 years, a par-fund plan that locks capital after 10 years, and how both stack up against CPF, SSB and T-bills.

Read article

A plain-English look at PRUActive Protect and Prudential's five other critical illness plans — coverage, riders, and who each one actually fits.

Read article

CPF, SRS, SSB, T-Bills, Endowment Plans & Robo-Advisors — Compared Side by Side

Read article

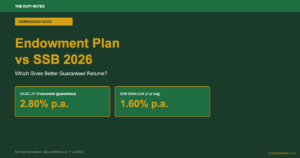

OCBC's 2-Year Endowment Plan guarantees 2.80% p.a. today. The latest Singapore Savings Bond averages just 1.60% over the same two years. Here's the full breakdown, plus the one thing the SSB does better than any endowment plan.

Read article

Real 2026 rates, a S$20,000 worked example, and an honest verdict on which guaranteed option actually pays more.

Read article

Real premium comparisons, the DPI shortcut, and the exact moves that lower your quote — without cutting the coverage you actually need.

Read article

Guaranteed returns, participating bonuses, fees and how Singapore's oldest insurer's endowment plans actually work

Read article

A complete breakdown of AIA's flagship term life plan — premiums, riders, AIA Vitality discounts, and how it stacks up against FWD, Singlife and Manulife.

Read article

Actual AIA, Prudential, Manulife and GreatLink fund factsheet data — plus the pricing quirk that quietly eats your first-year returns.

Read article

A 2026 employer's guide to group medical insurance in Singapore — costs, top providers, and how it fits with IRAS tax rules and MOM requirements.

Read article

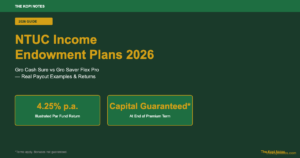

Gro Cash Sure vs Gro Saver Flex Pro vs Gro Capital Ease — real payout examples, guaranteed vs non-guaranteed returns, and who each plan actually suits.

Read article

What's compulsory, what's optional, and how SME owners and HR teams should set up employee cover in 2026.

Read article

Goal 2026, IncomeGen, IncomeSecure, GrowSecure and WealthGen compared side by side — guaranteed returns, minimum premiums and who each plan suits.

Read article

INVESTMENT INSURANCE GUIDE

Read article

Manulife term life insurance in Singapore centres on the ManuProtect Term (II) — a flexible plan covering death and terminal illness for 5 to 40 years, renewable to age 85 without a medical examination.

Read article

Compare Singapore's best endowment plans in 2026 — NTUC Income, Etiqa, Manulife, AIA & GE. Returns 3.5–4.2% p.a., vs T-bills 1.50%, FD 1.45–1.60%. SRS strategy & buyer's guide.

Read article

From $16/month for $500,000 coverage — our honest assessment of FWD's term life plans, premiums, and claims service.

Read article

A practical side-by-side comparison to help you choose the right life insurance in Singapore.

Read article

Term insurance covers you for a fixed period — typically 10 to 30 years — and pays a lump sum only if you die within that term. Whole life insurance covers you for your entire life and builds a cash value you can access later.

Read article

Everything you need to know before committing your savings to OCBC's short-term endowment plan.

Read article

Most Singapore employees have group term life insurance through work — but many do not know the coverage limits, portability risks, or when they need their own individual policy.

Read article

How ILPs work, what they cost, and whether buying one makes sense for you — honest breakdown for Singapore investors.

Read article

The best savings plans in Singapore 2026 compared — endowment, CPF SA, SSB, T-Bills, robo-advisors and high-yield savings accounts. Find the right plan for your goals and risk appetite.

Read article

Your complete guide to LIA Singapore — the industry body that voices the interests of members, addresses industry issues through engagement with stakeholders, and works with members to develop guidelines and codes of practice.

Read article

An honest, data-driven look at Singlife — MAS-licensed, digitally-native, and growing fast. Here's everything Singaporeans need to know before buying a policy.

Read article

Compare the right plan for your stage of life — clear premiums, payouts, and honest trade-offs.

Read article

Is this short-term endowment worth it — or do T-bills and savings bonds beat it hands down?

Read article

Universal life insurance offers flexible premiums and cash value growth — but is it right for Singaporeans? We break down the real costs, pros, cons, and cheaper alternatives for 2026.

Read article

Compare term CI, whole life CI, and multipay critical illness plans from AIA, Prudential, Great Eastern, and Singlife — with real premium data for Singapore residents.

Read article

Compare term CI, whole life CI, and multipay critical illness plans from AIA, Prudential, Great Eastern, and Singlife — with real premium data for Singapore residents.

Read article

Singlife Multipay Critical Illness II covers 135 conditions with up to 900% payout. Here's how it compares to AIA, Manulife, Prudential and FWD multi-pay CI plans.

Read article

A complete guide to buying and selling pre-owned insurance policies on Singapore's secondary market — how it works, what it costs, and whether it makes financial sense for you.

Read article

A life insurance savings plan combines protection with wealth-building. This guide compares the best plans in Singapore 2026 — returns, fees, and who should buy.

Read article

Complete guide to insurance nominations in Singapore. Learn the difference between revocable and trust nominations, how to nominate online since 2024, and why every policyholder needs one.

Read article

A plain-English comparison of every CI plan type available in Singapore — with real premium estimates, worked examples, and a decision framework.

Read article

A neutral, data-driven comparison — real fees, worked SGD examples, and what r/singaporefi actually says about both approaches.

Read article

Compare FWD, Singlife, Manulife, AIA, Prudential & NTUC Income — side by side, with real 2026 premium data.

Read article

How to calculate your surrender value, when it's worth surrendering, and what you'll actually lose — explained in plain English.

Read article

6 Insurers • Term, Whole Life & Critical Illness • CPF Medisave Tips

Read article

An honest, independent review — product specs, surrender penalties, Reddit questions answered, and how it compares to SSBs, T-bills, and fixed deposits.

Read article

Term, Whole Life, Critical Illness & DPS — What You Need, How Much Cover, and How to Buy

Read article

A complete guide to Manulife's participating fund — par fund mechanics, bonus history, returns, and how it compares to alternatives for Singapore investors in 2026.

Read article

Compare AIA, Manulife, Singlife, Prudential and Great Eastern — prices, coverage, and our verdict for each type of buyer.

Read article

Your complete guide to capital guaranteed insurance savings plans — how they work, which insurers offer the best returns, and whether they belong in your Singapore financial plan.

Read article

Get paid at diagnosis — not just at the final stage.

Read article

Updated June 2026 · 8 min read

Read article

How multi-pay CI works, what stages are covered, and whether the higher premium makes sense for you.

Read article

An honest, data-driven comparison of Singapore's top ILPs — so you can decide if one belongs in your financial plan.

Read article

Whole life premiums, cash value, best plans and the honest verdict — for Singapore residents in 2026.

Read article

Compare 2-year and 3-year endowment plans from Singapore's top insurers — projected returns, capital guarantees, and who should buy.

Read article

TM Term Assure II, FlexiAssurance & FlexiCover compared — with real premium data and a plain-English verdict

Read article

Compare investment linked policy Singapore plans from AIA, Prudential, Great Eastern, Manulife and NTUC Income — with a clear fee breakdown and honest ILP vs ETF verdict.

Read article

Compare the best critical illness insurance plans in Singapore 2026. FWD Big 3 CI from S$198/yr, Manulife multi-pay, AIA Power Critical Care — premiums, conditions covered, and who should buy each plan.

Read article

Everything you need to know before putting a lump sum into a single premium endowment plan.

Read article

Protect up to 75% of your salary if illness or injury stops you working — here's everything you need to know about DI insurance in Singapore.

Read article

Compare the top ISPs in Singapore — guaranteed returns, projected yields, SRS tax savings, and who should buy in 2026.

Read article

Compare the best term life insurance plans in Singapore 2026. Real premium tables by age and insurer, how much cover you need, and a step-by-step buyer's guide.

Read article

Looking for a capital-guaranteed way to grow your savings while getting life insurance coverage? An insurance savings plan in Singapore combines disciplined saving with guaranteed returns — but the devil is in the details.

Read article

Compare guaranteed yields, capital protection, and how short term endowment plans stack up against T-bills and fixed deposits in 2026.

Read article

We compare all 13 major Singapore insurers' endowment plans by guaranteed return, term, and minimum premium — updated 28 July 2026, including Singlife's Secure Saver discontinuation.

Read article

A critical illness diagnosis can derail your finances in weeks. Critical illness insurance Singapore pays a tax-free lump sum on diagnosis — giving you cash to cover treatment…

Read article

A complete guide to the Dependants' Protection Scheme (DPS) — Singapore's CPF-linked group term life insurance covering millions of working Singaporeans.

Read article

Universal life insurance combines lifelong death benefit protection with a cash-value savings component — but is it the right fit for Singapore investors? This guide covers how…

Read article

Critical illness insurance Singapore is one of the most important financial safety nets you can have — yet most Singaporeans are dangerously underinsured.

Read article

If you want a capital-guaranteed way to grow your savings in Singapore — without the volatility of stocks — an endowment plan could be your answer.

Read article

Read the full article on The Kopi Notes.

Read article

The most cost-effective way to protect your family’s financial future — how term life works, how much coverage you need, and the best options available in Singapore.

Read article

A clear-eyed look at how endowment plans work, what returns to realistically expect, and whether your money could be working harder elsewhere.

Read article

Understand how ILPs work, what they really cost, and whether they make sense for your financial goals — a no-nonsense Singapore investor’s perspective.

Read articleFrequently Asked Questions

How much life insurance do I need in Singapore?

A common rule of thumb is 9–12x your annual income, minus existing assets and CPF. For a 30-year-old earning $5,000/month with a mortgage and young children, that typically works out to $500,000–$1,000,000 in coverage. Our life insurance guide includes a step-by-step calculation framework.

Is an ILP better than buying term insurance and investing the rest?

In most cases, no. The “buy term and invest the rest” (BTIR) strategy typically outperforms ILPs over 20+ years due to significantly lower fees. ILPs charge distribution costs, insurance charges, and fund management fees that compound over time. Our investment insurance guide includes a detailed cost comparison.

Should I buy insurance through an agent or directly?

For straightforward term life insurance, Direct Purchase Insurance (DPI) through compareFIRST.sg often offers lower premiums since there’s no agent commission. For complex needs (estate planning, business insurance, large policies), an independent financial adviser can add value. Avoid captive agents tied to a single insurer.

What’s the difference between endowment plans and ILPs?

Endowment plans offer guaranteed returns plus non-guaranteed bonuses over a fixed term (typically 10–25 years). ILPs invest your premiums in sub-funds with entirely market-dependent returns and no guarantees. Endowments are lower risk but lower potential return; ILPs carry market risk plus high fees. Our investment insurance guide compares both in detail.

Do I still need insurance if I’m single with no dependants?

Life insurance primarily protects dependants, so if nobody relies on your income, you likely don’t need it yet. However, you should still have adequate health insurance (MediShield Life + Integrated Shield Plan) and may want critical illness coverage. Some people lock in whole life at a young age for lower premiums, but this ties up capital that could be invested.

Want more insurance analysis?

Browse all our insurance articles, comparisons, and brand reviews.