INSURANCE GUIDE → INVESTMENT INSURANCE

Investment Insurance Singapore 2026: ILPs, Endowments & Better Alternatives

The honest guide to investment-linked insurance — real costs, projected returns, and why ETFs or robo-advisors deliver better outcomes in most scenarios.

Last updated: May 2026 · 20 min read · By The Kopi Notes

📍 Start Here

Jump to the topic most relevant to you.

Investment Insurance Overview

Investment insurance in Singapore includes two main product types: endowment plans and investment-linked policies (ILPs). Both bundle life insurance with a savings or investment component — but at significantly higher costs than buying protection and investments separately.

Endowment plans offer a guaranteed maturity value plus non-guaranteed bonuses over a fixed term (typically 10–25 years). They function like a high-fee fixed deposit with a small insurance component. ILPs invest your premiums in unit trust sub-funds, with returns entirely dependent on market performance — minus layers of fees that can total 3–5% annually.

The fundamental question for both products: does the insurance wrapper add enough value to justify fees that are 2–10x higher than direct alternatives? In most cases, the data suggests not. This guide breaks down exactly why — and identifies the narrow scenarios where investment insurance might still make sense.

Not financial advice. All figures are for educational reference only. Data as at May 2026 unless noted.

ILP vs ETF: Cost Comparison

Over 25 years: On a $500/month investment, the fee difference alone compounds to $80,000–$150,000 in lost returns. This is the “cost of convenience” for buying investments through an insurance wrapper.

Investment-Linked Policies (ILPs)

ILPs invest your premiums in unit trust sub-funds while providing basic life insurance coverage. Returns are entirely market-dependent — there are no guarantees. The key issue is cost: ILPs layer insurance charges, distribution fees, fund management fees, and platform charges that together consume 3–5% of your investment annually.

In the first 1–5 years, a significant portion of premiums (often 30–100% in year 1) goes to distribution costs rather than investment. This creates a deep hole that market returns must overcome before you break even. Most ILP holders who surrender in the first 5 years lose money.

Our detailed ILP guide breaks down the fee structure with real examples, shows projected returns vs direct investing alternatives, and explains the specific limited scenarios where ILPs might still be appropriate.

Endowment Plans

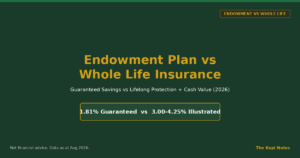

Endowment plans offer a guaranteed maturity value plus non-guaranteed bonuses (participating bonuses and terminal bonuses). They function as medium-term forced savings vehicles with a small death benefit. Typical terms range from 10–25 years with guaranteed returns of 1–2% p.a. and projected total returns of 2.5–3.5% p.a. including bonuses.

The appeal is simplicity and guarantees — you know the minimum you’ll get back. The trade-off: returns are low compared to alternatives, and early surrender means losing principal. Singapore Savings Bonds (SSBs), fixed deposits, and T-bills all offer competitive guaranteed returns without the lock-in period.

Our endowment guide compares real product yields against alternatives, explains bonus structures, and identifies when the forced savings discipline might justify the lower returns.

Should You Buy Investment Insurance?

Decision Framework

❌ Skip if: You can invest directly (even via robo-advisors), you understand basic index funds, or you have a time horizon under 10 years.

⚠️ Consider endowments if: You genuinely cannot save without forced commitments, you need guaranteed returns, and you can lock up funds for 15+ years without needing access.

⚠️ Consider ILPs if: You have very specific estate planning needs, you want dollar-cost averaging with minimal admin, AND you accept paying 2–4% extra annually for that convenience.

✓ Better alternatives for most people: Term life + VWRA/CSPX via IBKR, or term life + Syfe/Endowus robo-advisor. Lower fees, better liquidity, historically superior returns.

All Investment Insurance Articles

Browse our detailed guides on ILPs and endowment plans.

Investment Insurance Articles

ILPs, endowment plans, and investment-linked insurance guides for Singapore.

A side-by-side look at endowment plans and Singapore Government Securities (SGS) bonds — with real 2026 rates, worked examples, and who each one actually suits.

Read article

Same $500 a month, two completely different paths -- we ran the actual 20-year numbers.

Read article

Both come wrapped in an insurance policy. Only one of them guarantees you anything.

Read article

Two very different tools that get compared for the wrong reasons — here's how they actually work.

Read article

Endowment plans guarantee ~1.81% p.a., unit trusts offer higher potential returns with market risk. We compare fees, a S$20,000 3-year worked example, and which fits your goals.

Read article

Guaranteed Returns vs Flexible, Liquid Growth — Which Wins for Your Idle Cash?

Read article

A side-by-side look at endowment plans against globally diversified ETFs like VWRA and CSPX — guaranteed rates, real historical returns, fees, tax, and who should pick which in 2026.

Read article

A Singapore investor's real-numbers comparison of endowment plan guaranteed returns against S-REIT dividend yields, tax treatment, and a worked S$20,000 growth scenario.

Read article

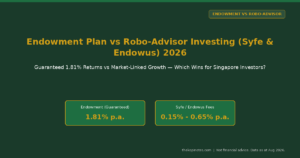

Comparing a guaranteed 1.81% p.a. endowment plan against Syfe and Endowus robo-advisor portfolios — fees, projected growth, and which fits your risk profile in 2026.

Read article

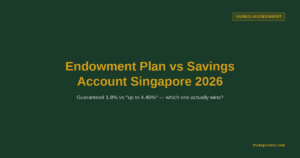

High-yield savings accounts advertise up to 4.45% p.a., but most Singaporeans never hit that rate. Here's the real guaranteed-returns comparison against endowment plans in 2026.

Read article

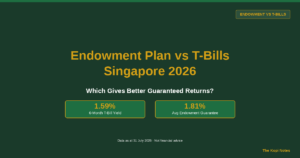

The 6-month T-bill's yield has risen for three straight auctions, hitting 1.59% p.a. on 30 July. The average Singapore endowment plan still guarantees more, at 1.81% p.a.

Read article

CPF's Special/Retirement Account floor pays 4% p.a. guaranteed. The average Singapore endowment plan guarantees just 1.8%. Here's the full breakdown — including whether you can actually use CPF to buy one.

Read article

An independent look at Singlife's newest capital-guaranteed savings plan — what it guarantees, what it doesn't, and how it fits after Secure Saver was discontinued.

Read article

Guaranteed monthly or yearly payouts, plus the real 2023-2025 Par Fund return data Tokio Marine doesn't put on its own product page.

Read article

1.6% p.a. guaranteed over 2 years, 100% capital guarantee at maturity — but the current tranche is sold out. Here's what's inside, and what to do while you wait.

Read article

SaveForward, FlexiCash Growth, and the truth about the "10% guaranteed cash benefit" — verified against China Life's own product pages.

Read article

Etiqa's full savings plan lineup reviewed — capital-guaranteed endowments from just $125/month, with real numbers from official product pages.

Read article

Guaranteed capital, real declared bonus rates, and what the reported Allianz sale could mean for your policy.

Read article

A plain-English look at AIA's short-term guaranteed #Wealth Savvy tranches and the longer-term Smart Wealth Builder Series, with real numbers pulled straight from AIA's own policy documents.

Read article

Guaranteed 1.70% p.a. over 3 years, a par-fund plan that locks capital after 10 years, and how both stack up against CPF, SSB and T-bills.

Read article

CPF, SRS, SSB, T-Bills, Endowment Plans & Robo-Advisors — Compared Side by Side

Read article

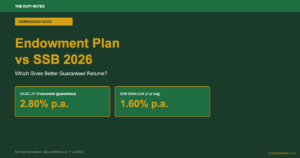

OCBC's 2-Year Endowment Plan guarantees 2.80% p.a. today. The latest Singapore Savings Bond averages just 1.60% over the same two years. Here's the full breakdown, plus the one thing the SSB does better than any endowment plan.

Read article

Real 2026 rates, a S$20,000 worked example, and an honest verdict on which guaranteed option actually pays more.

Read article

Guaranteed returns, participating bonuses, fees and how Singapore's oldest insurer's endowment plans actually work

Read article

Actual AIA, Prudential, Manulife and GreatLink fund factsheet data — plus the pricing quirk that quietly eats your first-year returns.

Read article

Gro Cash Sure vs Gro Saver Flex Pro vs Gro Capital Ease — real payout examples, guaranteed vs non-guaranteed returns, and who each plan actually suits.

Read article

Goal 2026, IncomeGen, IncomeSecure, GrowSecure and WealthGen compared side by side — guaranteed returns, minimum premiums and who each plan suits.

Read article

INVESTMENT INSURANCE GUIDE

Read article

Compare Singapore's best endowment plans in 2026 — NTUC Income, Etiqa, Manulife, AIA & GE. Returns 3.5–4.2% p.a., vs T-bills 1.50%, FD 1.45–1.60%. SRS strategy & buyer's guide.

Read article

Everything you need to know before committing your savings to OCBC's short-term endowment plan.

Read article

How ILPs work, what they cost, and whether buying one makes sense for you — honest breakdown for Singapore investors.

Read article

The best savings plans in Singapore 2026 compared — endowment, CPF SA, SSB, T-Bills, robo-advisors and high-yield savings accounts. Find the right plan for your goals and risk appetite.

Read article

Is this short-term endowment worth it — or do T-bills and savings bonds beat it hands down?

Read article

Universal life insurance offers flexible premiums and cash value growth — but is it right for Singaporeans? We break down the real costs, pros, cons, and cheaper alternatives for 2026.

Read article

A life insurance savings plan combines protection with wealth-building. This guide compares the best plans in Singapore 2026 — returns, fees, and who should buy.

Read article

A neutral, data-driven comparison — real fees, worked SGD examples, and what r/singaporefi actually says about both approaches.

Read article

How to calculate your surrender value, when it's worth surrendering, and what you'll actually lose — explained in plain English.

Read article

An honest, independent review — product specs, surrender penalties, Reddit questions answered, and how it compares to SSBs, T-bills, and fixed deposits.

Read article

A complete guide to Manulife's participating fund — par fund mechanics, bonus history, returns, and how it compares to alternatives for Singapore investors in 2026.

Read article

Your complete guide to capital guaranteed insurance savings plans — how they work, which insurers offer the best returns, and whether they belong in your Singapore financial plan.

Read article

Updated June 2026 · 8 min read

Read article

An honest, data-driven comparison of Singapore's top ILPs — so you can decide if one belongs in your financial plan.

Read article

Compare 2-year and 3-year endowment plans from Singapore's top insurers — projected returns, capital guarantees, and who should buy.

Read article

Compare investment linked policy Singapore plans from AIA, Prudential, Great Eastern, Manulife and NTUC Income — with a clear fee breakdown and honest ILP vs ETF verdict.

Read article

Everything you need to know before putting a lump sum into a single premium endowment plan.

Read article

Compare the top ISPs in Singapore — guaranteed returns, projected yields, SRS tax savings, and who should buy in 2026.

Read article

Looking for a capital-guaranteed way to grow your savings while getting life insurance coverage? An insurance savings plan in Singapore combines disciplined saving with guaranteed returns — but the devil is in the details.

Read article

Compare guaranteed yields, capital protection, and how short term endowment plans stack up against T-bills and fixed deposits in 2026.

Read article

We compare all 13 major Singapore insurers' endowment plans by guaranteed return, term, and minimum premium — updated 28 July 2026, including Singlife's Secure Saver discontinuation.

Read article

Universal life insurance combines lifelong death benefit protection with a cash-value savings component — but is it the right fit for Singapore investors? This guide covers how…

Read article

If you want a capital-guaranteed way to grow your savings in Singapore — without the volatility of stocks — an endowment plan could be your answer.

Read article

A clear-eyed look at how endowment plans work, what returns to realistically expect, and whether your money could be working harder elsewhere.

Read article

Understand how ILPs work, what they really cost, and whether they make sense for your financial goals — a no-nonsense Singapore investor’s perspective.

Read articleFrequently Asked Questions

Should I surrender my ILP and invest in ETFs instead?

It depends on how long you’ve held the policy. If you’re past the high-surrender-charge period (typically 5+ years), switching to term life + ETFs often makes mathematical sense due to the ongoing fee savings. If you’re in years 1–3, you’ll crystallise large losses. Run the numbers: compare your current fund value vs total premiums paid, and project forward with vs without the ongoing fee drag.

Are endowment plan returns guaranteed?

Only partially. Endowments have a guaranteed component (typically 1–2% p.a.) plus non-guaranteed bonuses that depend on the insurer’s investment performance and discretion. The “projected” returns shown in benefit illustrations assume bonus rates that may not materialise. Always evaluate endowments based on the guaranteed return only, and compare that against risk-free alternatives like SSBs or T-bills.

What’s the real return of ILPs after all fees?

If the underlying funds return 7% p.a. (broadly in line with global equity averages), after ILP fees of 3–5% p.a., your net return is roughly 2–4% p.a. The same market exposure via VWRA (0.22% TER) would net you approximately 6.5–6.8% p.a. Over 25 years on $500/month, that difference compounds to $80,000–$150,000 in lost returns.

Is “buy term and invest the rest” always better?

Mathematically, yes — over 15+ year horizons with consistent investing in low-cost index funds. The caveat: it requires discipline. If you’d spend the premium savings instead of investing them, the forced savings of an endowment or ILP has behavioural value. But with robo-advisors offering automated monthly investing for 0.25–0.65% p.a., the “discipline” argument is weaker than it once was.

Part of the Insurance Singapore Guide

Need life insurance instead?

Our life insurance guide covers term, whole life, and how to calculate your coverage needs.