Endowment Plans in Singapore: Are They Worth It?

A clear-eyed look at how endowment plans work, what returns to realistically expect, and whether your money could be working harder elsewhere.

Endowment plans have long been a popular savings and insurance product in Singapore. Marketed as a disciplined way to save for milestones like your child’s education or retirement, these plans promise guaranteed payouts at maturity. But with returns typically ranging from just 2–4% per annum and significant early surrender penalties, are endowment plans actually a good use of your money? This guide explains how they work, compares them to alternatives, and helps you decide.

Not financial advice. All figures are for educational reference only. Data as at May 2026 unless noted.

Table of Contents

Contents — Click to expand

- What Is an Endowment Plan?

- How Do Endowment Plans Work?

- Types of Endowment Plans in Singapore

- What Returns Can You Expect?

- The Pros of Endowment Plans

- The Cons of Endowment Plans

- Endowment Plan vs Fixed Deposit vs Index Fund

- Should You Buy an Endowment Plan?

- Already Have an Endowment Plan?

- Frequently Asked Questions

What Is an Endowment Plan?

An endowment plan is an insurance savings product where you pay premiums over a fixed period — typically 10 to 25 years — and receive a lump-sum payout at maturity. The payout usually consists of two components: a guaranteed component (the insurer contractually promises to pay this amount) and a non-guaranteed bonus component (projected but not promised, and subject to the insurer’s investment performance and discretion).

Most endowment plans also include a basic life insurance component, though the coverage amount is typically modest — often just the total premiums paid or slightly above — compared to dedicated life insurance products like term life insurance which offers far higher coverage per dollar of premium.

Endowment plans are considered participating policies, which means policyholders participate in the insurer’s participating fund and may receive bonuses (also called dividends) based on the fund’s performance. These bonuses are the non-guaranteed component of your maturity payout.

How Do Endowment Plans Work?

When you pay your premiums, the insurer pools your money with other policyholders’ premiums into a participating fund. This fund is invested in a diversified mix of assets — typically 40–60% in bonds and fixed income, 20–40% in equities, and the remainder in property, alternative investments, and cash.

The insurer manages all investment decisions and bears the investment risk for the guaranteed component. The non-guaranteed bonus component fluctuates based on how the participating fund performs relative to the insurer’s assumptions. Insurers declare bonuses annually (reversionary bonuses) and at maturity (terminal bonuses).

The key mechanism is that the insurer smooths returns over time. In good years, the insurer retains some profits to build reserves; in bad years, it uses those reserves to maintain stable bonus payouts. This smoothing is why endowment returns appear stable but are generally lower than what you could achieve by investing directly in a diversified portfolio.

One important detail: once a reversionary bonus is declared and added to your policy, it becomes guaranteed — the insurer cannot take it back. Terminal bonuses, however, are only paid at maturity or upon a valid claim, and the insurer can adjust them based on prevailing market conditions at the time.

Types of Endowment Plans in Singapore

Several types of endowment plans are available in Singapore, each designed for different savings goals and time horizons:

| Type | Typical Tenure | Key Features |

|---|---|---|

| Traditional Endowment | 15–25 years | Regular premium payments, lump-sum payout at maturity. Best for long-term forced savings goals. |

| Single-Premium Endowment | 2–10 years | One-time lump-sum payment. Often used as a fixed deposit alternative with slightly higher returns. |

| Short-Term Endowment | 2–5 years | Shorter lock-up period. Popular as a cash management tool. Returns are lower than longer-term plans. |

| Education Endowment | 15–21 years | Designed to mature when your child reaches university age. Some offer periodic payouts for school fees. |

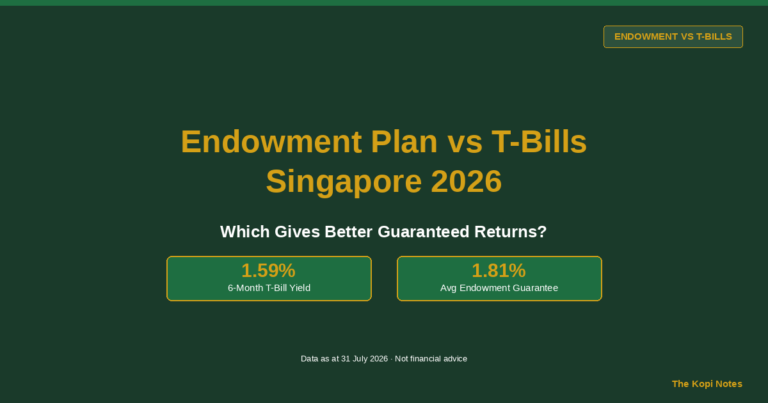

What Returns Can You Expect?

Endowment plan returns in Singapore typically range from 2% to 4% per annum, depending on the plan tenure, insurer, and prevailing interest rate environment. The breakdown usually looks like this:

- Guaranteed component — Works out to approximately 1.0–2.0% p.a. This is what the insurer contractually promises to pay, regardless of market conditions.

- Non-guaranteed bonuses — Adds approximately 1.0–2.0% p.a. on top, but this portion is projected and may not materialise in full.

For context, here is how endowment returns compare to other low-risk alternatives available to Singapore investors:

| Product | Typical Return (p.a.) | Liquidity | Capital Guarantee? |

|---|---|---|---|

| Endowment Plan | 2–4% | Low (locked 10–25 years) | Partially (guaranteed portion only) |

| Singapore T-Bills (6-month) | 2.5–3.5% | High (6-month maturity) | Yes (Singapore Government) |

| Fixed Deposit (12-month) | 2.0–3.0% | Medium (12-month lock) | Yes (SDIC-insured up to $100k) |

| Global Equity ETF (e.g. VWRA) | 7–9% (historical long-term) | High (sell anytime) | No |

| CPF OA | 2.5% | Low (withdrawal restrictions) | Yes (Government-backed) |

The key takeaway: endowment plans offer returns that are comparable to or only slightly better than Singapore T-Bills and fixed deposits, but with significantly less liquidity. For investors with a longer time horizon (10+ years) and some risk tolerance, low-cost equity ETFs have historically delivered meaningfully higher returns.

The Pros of Endowment Plans

- Disciplined savings — Regular premium payments enforce a savings habit. If you struggle to save consistently on your own, the contractual obligation to pay premiums can be a feature rather than a bug.

- Capital protection — The guaranteed component means you will not lose your principal if you hold the plan to maturity. This provides peace of mind for risk-averse savers.

- Simplicity — No need to make investment decisions, monitor markets, or rebalance a portfolio. The insurer handles everything.

- Insurance coverage — Basic life coverage is included, typically covering death and TPD for the sum assured or total premiums paid.

- Tax-free proceeds — In Singapore, endowment maturity payouts and death benefits are not subject to income tax.

The Cons of Endowment Plans

- Low returns — Net returns of 2–4% p.a. are modest, especially over a 15–25 year horizon. Inflation (historically 2–3% in Singapore) can erode the real purchasing power of your maturity payout.

- Illiquidity — Your money is locked up for the full duration of the plan. Early surrender typically results in receiving less than your total premiums paid, especially in the first few years.

- Opportunity cost — The premiums paid into an endowment could potentially earn significantly higher returns if invested in a diversified equity portfolio over the same time horizon.

- Non-guaranteed bonuses may not materialise — The projected maturity value shown in benefit illustrations includes non-guaranteed bonuses that depend on the insurer’s participating fund performance and bonus policy.

- High distribution costs — Endowment plans typically pay the financial adviser a commission of 30–50% of the first year’s premium, which is why they are actively sold. This cost is embedded in the product and reduces your effective returns.

Endowment Plan vs Fixed Deposit vs Index Fund

For risk-averse savers, the choice often comes down to endowment plans, fixed deposits, or T-Bills. The right choice depends on your financial goals, time horizon, and comfort with market volatility.

If your primary goal is capital preservation with modest returns and you want a fixed timeline, a short-term endowment or Singapore T-Bills may be appropriate. T-Bills offer comparable returns with much better liquidity.

If your time horizon is 10+ years and you can tolerate some market volatility, a diversified global equity ETF like VWRA has historically delivered 7–9% p.a. over long periods — roughly double the return of an endowment plan. The trade-off is that equity values fluctuate and there is no capital guarantee.

If you want the best of both worlds, consider splitting your savings: use T-Bills or fixed deposits for short-term goals (1–5 years) and low-cost index funds for long-term goals (10+ years). This approach gives you liquidity, higher expected returns, and more control over your money than an endowment plan.

Should You Buy an Endowment Plan?

Endowment plans may be suitable if you meet all of the following criteria:

- You want a guaranteed, hands-off savings product and are willing to accept modest returns in exchange for capital protection.

- You have a specific savings goal with a fixed timeline (e.g., child’s university fund in 18 years).

- You struggle to save or invest consistently on your own and need the discipline of contractual premium payments.

- You have already secured adequate insurance coverage through term life insurance and are not relying on the endowment plan for protection.

However, if you are comfortable investing on your own and can tolerate some market volatility, you will likely achieve better long-term returns through a diversified portfolio of low-cost index funds. The opportunity cost of locking your money in an endowment plan for 15–25 years at 2–4% p.a. is substantial when the alternative could deliver 7–9% p.a. over the same period.

Already Have an Endowment Plan?

If you already hold an endowment plan, the decision to keep or surrender it depends on how far along you are:

- Early years (first 3–5 years) — Surrendering now will likely result in receiving significantly less than your premiums paid. However, if the opportunity cost of continuing is high and you can deploy the premiums more effectively, cutting your losses early may still be the rational choice.

- Mid-term (5–15 years in) — Your surrender value is closer to your premiums paid. Run the numbers: compare the projected maturity payout against what you could earn by investing the remaining premiums in a low-cost ETF.

- Near maturity (within 3–5 years) — It usually makes sense to hold to maturity to receive the full guaranteed payout plus any terminal bonus.

Request your latest benefit illustration from the insurer to see the current guaranteed and projected maturity values. Compare these against alternative investment scenarios before making a decision.

Frequently Asked Questions

What is a typical endowment plan return in Singapore?

Endowment plan returns in Singapore typically range from 2% to 4% per annum, with the guaranteed portion accounting for roughly 1–2% p.a. and the non-guaranteed bonus component making up the rest. Actual returns depend on the plan tenure, insurer, and the performance of the insurer’s participating fund. Shorter-tenure plans (2–5 years) generally offer lower returns than longer-tenure plans (15–25 years).

Can I withdraw my endowment plan early?

Yes, but early surrender typically results in receiving less than your total premiums paid — especially in the first few years. Insurers impose surrender charges that decrease over time. In the first 2–3 years, you may receive back only 30–70% of your premiums paid. The surrender value gradually increases and typically catches up to your total premiums paid somewhere around the mid-point of the plan tenure. Check your policy’s guaranteed surrender value table for the exact figures.

Are endowment plan payouts taxable in Singapore?

No. In Singapore, maturity payouts and death benefits from endowment plans are not subject to income tax. This is one of the advantages of insurance-linked savings products. However, this tax benefit alone does not make endowment plans superior to alternatives — Singapore also does not tax capital gains from investments such as ETFs and stocks, so the tax treatment is comparable.

Is an endowment plan better than a fixed deposit?

It depends on your priorities. Endowment plans typically offer slightly higher returns (2–4% vs 2–3% for fixed deposits) but require you to lock up your money for much longer (10–25 years vs 12 months). Fixed deposits are SDIC-insured up to $100,000 and offer much better liquidity. For short-term savings (1–3 years), fixed deposits or Singapore T-Bills are generally more suitable. Endowment plans may only make sense for very long-term forced savings goals where you want a guaranteed payout at a specific future date.

Should I use an endowment plan for my child’s education fund?

Education endowment plans are a popular choice for parents who want a guaranteed fund for their child’s university education. The advantage is that you know exactly when the payout will occur and can plan accordingly. However, the returns (2–4% p.a.) may not keep pace with the rising cost of education in Singapore, which has been increasing at 3–5% per year. An alternative approach is to invest in a diversified global ETF portfolio for the first 10–15 years (capturing higher equity returns) and then gradually shift to lower-risk assets like T-Bills or fixed deposits as the university start date approaches.

Explore Better Alternatives

Compare endowment plans against T-Bills, fixed deposits, and low-cost ETFs. Use our guides and referral links to get started.

Get Free Insurance Advice

Speak with a licensed insurance advisor. No obligation, no cost.

By submitting this form, you agree to our Privacy Policy.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.