Singapore T-Bill Interest Rate 2026: Latest Auction Results, Historical Rates & What’s Driving Yields

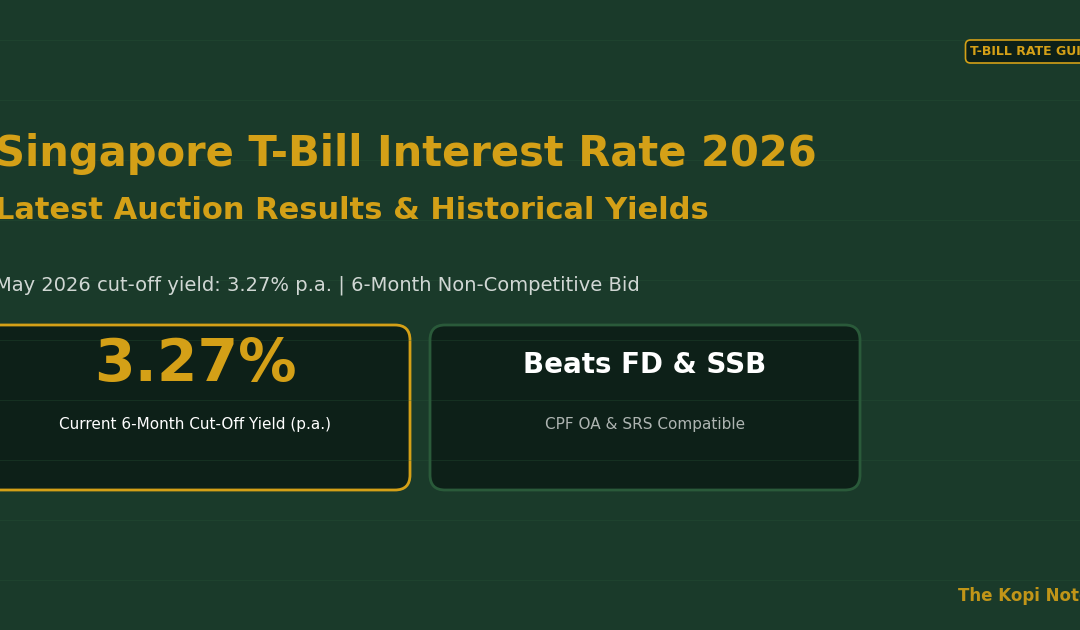

The Singapore T-bill interest rate for the 6-month bill stands at 3.27% p.a. as of the May 2026 auction — a meaningful recovery from the post-Fed-pivot lows of late 2025. Singapore Government Treasury Bills (T-bills) are short-term, risk-free debt instruments issued by MAS, available in 6-month and 1-year tenors. Singapore investors can apply via cash, CPF OA, or SRS, and have consistently used T-bills as a low-risk alternative to fixed deposits since yields spiked in 2022.

Not financial advice. All figures are for educational reference only. Data as at May 2026 unless noted.

📋 Table of Contents

Contents

- Current Singapore T-Bill Interest Rate (May 2026)

- T-Bill Auction Results History 2022–2026

- What Drives Singapore T-Bill Yields?

- 6-Month vs 1-Year T-Bill: Which Rate Is Better?

- T-Bill Rate vs SSB vs Fixed Deposit vs CPF OA

- How to Apply for Singapore T-Bills

- T-Bill Laddering Strategy for Singapore Investors

- FAQ: Singapore T-Bill Interest Rate

Current Singapore T-Bill Interest Rate (May 2026)

The most recent Singapore T-bill auction results (May 2026) show the 6-month T-bill cut-off yield at 3.27% p.a. The MAS conducts 6-month T-bill auctions approximately every two weeks, with 1-year auctions held quarterly. The cut-off yield — the lowest yield at which all bids are accepted — is what most retail investors who apply via non-competitive bids receive.

Here is a snapshot of the latest T-bill auction results for Singapore in 2026:

| Auction Date | Tenor | Cut-Off Yield (p.a.) | Total Amount (S$M) |

|---|---|---|---|

| May 2026 (latest) | 6-Month | 3.27% | S$6,400M |

| Apr 2026 | 6-Month | 3.14% | S$6,200M |

| Mar 2026 | 6-Month | 1.46% | S$6,000M |

| Feb 2026 | 6-Month | 1.32% | S$5,800M |

| Jan 2026 | 1-Year | 2.91% | S$4,100M |

Source: Monetary Authority of Singapore (MAS), May 2026. Cut-off yields shown are annualised. Non-competitive bidders receive the cut-off yield.

The sharp jump from 1.46% in March to 3.27% in May 2026 reflects a significant repricing driven by global macro events — specifically renewed US tariff concerns and a flight to short-duration safe assets that pushed SGS yields higher. Investors who locked in a 6-month T-bill in late April or May 2026 are now earning a yield that beats most bank fixed deposits.

You can always check the latest cut-off yield directly on the MAS T-bills page after each auction result is announced. Results are typically published within 2 business days of the auction close.

T-Bill Auction Results History 2022–2026

Singapore T-bill yields have been on a wild ride since 2022. When the US Federal Reserve began its aggressive rate-hiking cycle, MAS T-bill yields followed — surging from near-zero in early 2022 to a peak of around 3.9% by late 2022 and holding above 3.5% through most of 2023. Then, as the Fed pivoted and began cutting rates in late 2024, T-bill yields in Singapore fell sharply, briefly touching the 1.3–1.6% range in early 2026.

| Period | Approx. Yield Range (p.a.) | Key Driver |

|---|---|---|

| H1 2022 | 0.5% – 1.8% | Fed begins hiking; early rate-rise |

| H2 2022 | 2.8% – 3.9% | Fed hikes aggressively; SGS yields surge |

| 2023 | 3.5% – 3.95% | Fed holds high; T-bill golden era |

| 2024 | 2.7% – 3.7% | Fed signals pivot; yields soften |

| Early 2025 | 2.5% – 3.0% | Fed cuts begin; SGS yields follow lower |

| Late 2025 – Early 2026 | 1.3% – 2.0% | Aggressive Fed cuts; yields near CPF OA floor |

| Apr–May 2026 | 3.14% – 3.27% | US tariff uncertainty; risk-off flight to quality |

Source: MAS Singapore Government Securities historical auction data. Approximate ranges based on cut-off yields.

The key takeaway: Singapore T-bill yields are not set by MAS directly — they are determined by market demand at each auction. When global uncertainty rises (as in Q1–Q2 2026 amid US tariff escalation), demand for safe Singapore Government Securities increases, which can temporarily push yields higher even when the US Fed is in a cutting cycle.

What Drives Singapore T-Bill Yields?

Unlike bank fixed deposits — where the bank sets the rate — T-bill yields in Singapore are determined by competitive market auctions. Understanding what moves these yields helps investors time their applications more effectively.

1. US Federal Reserve Policy. Singapore’s short-term interest rates are closely correlated with US Fed Funds Rate movements. When the Fed raises rates, capital flows into USD-denominated assets, putting upward pressure on Singapore short-term yields to remain competitive. This is why the 2022–2023 Fed hike cycle drove Singapore T-bill yields from near-zero to ~3.9%.

2. MAS Monetary Policy (Exchange Rate, Not Rate). MAS manages monetary policy via the Singapore Dollar exchange rate (the S$NEER policy band), not via interest rates directly. This means MAS does not set T-bill yields — the market does. You can follow MAS monetary policy statements at mas.gov.sg.

3. Global Risk Appetite. During periods of market stress or geopolitical uncertainty (e.g., the US tariff escalation of Q1–Q2 2026), investors globally seek safe-haven assets. Singapore Government Securities benefit from Singapore’s AAA credit rating. Increased demand for T-bills can influence cut-off yields at each auction.

4. Domestic Liquidity and CPF Application Volume. Singapore retail investors applying for T-bills via CPF OA or SRS create significant non-competitive demand. When retail participation surges (as it did in 2022–2023), total bid volume rises, which can affect how competitive institutional bids price the auction.

5. Singapore Savings Bonds (SSB) Rates. SSB rates act as a soft floor for T-bill yields. For a full comparison between T-bills and SSBs, check our Singapore T-bills 2026 guide.

6-Month vs 1-Year T-Bill: Which Rate Is Better?

MAS issues two tenors of T-bills — 6-month and 1-year. Here’s how the two compare in recent auctions:

| T-Bill Tenor | Auction Frequency | Recent Yield (May 2026) | Best For |

|---|---|---|---|

| 6-Month | Every 2 weeks | 3.27% p.a. | Flexibility, yield optimisation, laddering |

| 1-Year | Quarterly | 2.91% p.a. (Jan 2026) | Locking in rate, fewer rollovers, predictability |

Source: MAS auction results. Yields are annualised cut-off yields for non-competitive bidders.

In the current environment (May 2026), the 6-month T-bill wins on yield at 3.27% vs 2.91% for the 1-year. However, if rates are expected to fall further, locking in the 1-year at 2.91% provides certainty over the next 12 months. For most Singapore investors, the 6-month T-bill is the preferred choice — higher yield, auctions every 2 weeks, more entry points, and compatible with CPF OA, SRS, and cash applications.

T-Bill Rate vs SSB vs Fixed Deposit vs CPF OA

The Singapore T-bill interest rate of 3.27% (May 2026) now comfortably beats most bank fixed deposits and the CPF OA floor rate. Here’s the full comparison:

| Instrument | Current Rate (May 2026) | Min. Investment | Liquidity | CPF/SRS Compatible? |

|---|---|---|---|---|

| 6-Month T-Bill | 3.27% p.a. | S$1,000 | Locked 6 months | Yes — CPF OA & SRS |

| Singapore Savings Bonds (SSB) | ~2.7–3.0% (avg 10-yr) | S$500 | Redeemable anytime | No — cash only |

| Bank 6-Month Fixed Deposit | ~2.0–2.8% p.a. | S$20,000–S$50,000 | Locked 6 months | No — cash only |

| CPF Ordinary Account (OA) | 2.5% p.a. (guaranteed) | N/A | CPF locked | Yes — this is CPF |

| CPF Special Account (SA) | 4.0% p.a. | N/A | CPF locked | Yes — this is CPF |

Source: MAS, CPF Board, bank websites. Rates as at May 2026. Fixed deposit rates are indicative — check individual banks for current promotions.

At 3.27% p.a., the T-bill beats all fixed deposit rates and the CPF OA floor by a significant margin. On S$50,000, using CPF OA for T-bills earns approximately S$385 more per year than leaving funds in OA. See our CPF investment strategy guide for the complete OA optimisation framework, and our T-Bill, SSB & Fixed Deposit Comparison Calculator to model your exact returns.

How to Apply for Singapore T-Bills (Step-by-Step)

Singapore T-bills can be applied for through three channels: cash (via internet banking or ATM), CPF OA, and SRS. All retail applications are non-competitive by default.

Step 1: Check the next auction date at the MAS Auctions and Issuance Calendar. Auctions close at 9pm (cash) or 3pm (CPF OA) on the auction date.

Step 2: Choose your funding source — cash via DBS, OCBC, UOB, Maybank, or Standard Chartered; CPF OA via CPF e-Cashier; or SRS via your SRS operator’s internet banking.

Step 3: Submit a non-competitive application. Log in to your bank’s internet banking, navigate to Government Securities or T-bills, enter the face value (in multiples of S$1,000), and confirm. You do not need to specify a yield.

Step 4: Results are published within 2 business days. Interest (the discount) is credited at the issue date; your principal is returned at maturity.

For more detail, see our Singapore T-bills 2026 guide. Investors considering alternatives with daily liquidity — such as Endowus money market funds or Syfe Cash+ Guaranteed — should compare the trade-off between yield and accessibility.

T-Bill Laddering Strategy for Singapore Investors

Given that T-bill auctions occur every two weeks for the 6-month bill, savvy Singapore investors use a T-bill ladder to maintain liquidity while maximising yield. By applying across multiple consecutive auctions, a portion of capital matures every 2 weeks rather than being locked for a full 6 months.

For example, splitting S$100,000 across 5 consecutive auctions (S$20,000 each): once fully established, S$20,000 matures every 2 weeks. At 3.27% p.a., this earns approximately S$1,635 over 6 months with bi-weekly liquidity — far better than most savings accounts. This suits investors parking an emergency fund or near-term capital (e.g., a property downpayment) who still want above-FD returns.

Once your cash tier is optimised in T-bills, use a Singapore retirement calculator to model how the risk-free returns interact with your long-term wealth goals. For investors seeking higher income, our guide to the best S-REITs in Singapore 2026 covers dividend yields of 5–7% that complement a T-bill ladder in a diversified portfolio.

Disclaimer: T-bills are capital-safe but yield-variable — the cut-off rate changes at every auction. Always assess your personal financial situation and consider consulting a licensed financial adviser before investing.

Compare T-Bill Returns vs Other Instruments

Use our free calculator to see exactly how much more the T-bill earns vs your fixed deposit or SSB — in Singapore dollars.

FAQ: Singapore T-Bill Interest Rate

What is the current Singapore T-bill interest rate in 2026?

Is the Singapore T-bill interest rate higher than fixed deposits?

Can I use CPF OA to buy Singapore T-bills?

How often do Singapore T-bill auctions happen?

What is the minimum amount to invest in Singapore T-bills?

Do Singapore T-bills pay interest monthly?

How does the Singapore T-bill rate compare to CPF OA rate?

What happens if the T-bill interest rate falls next auction?

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.