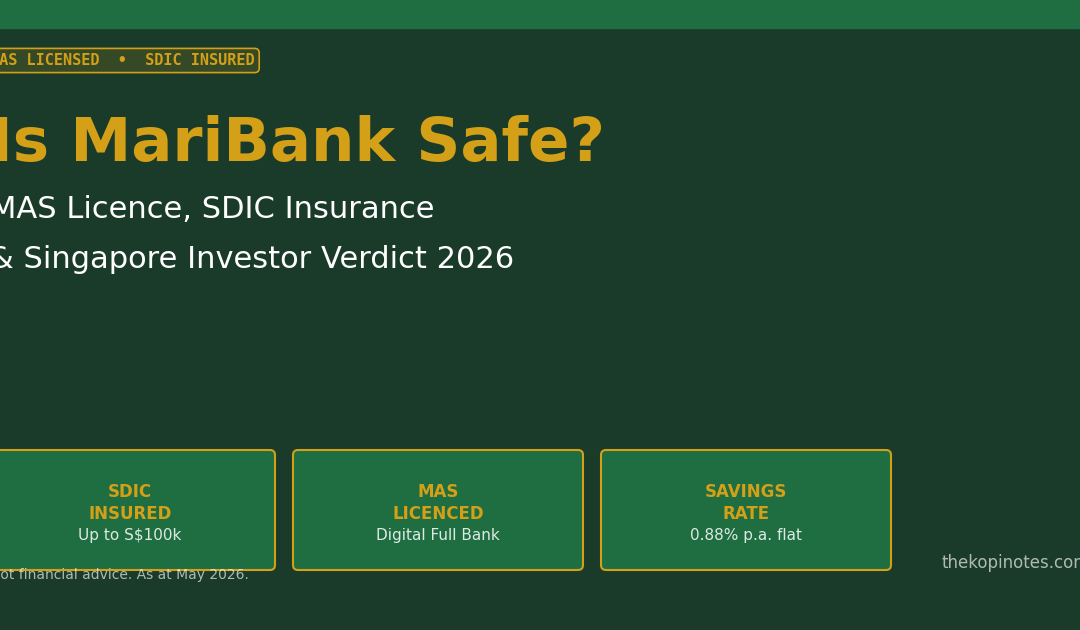

Is MariBank Safe? Your 2026 Guide to Singapore’s Digital Bank

MariBank is MAS-licensed, SDIC-insured up to S$100,000, and backed by Sea Limited — but how does it really stack up for Singapore savers and investors?

Last updated: May 2026 | Not financial advice. Do your own due diligence before depositing.

If you have been scrolling through the App Store reviews or finance forums wondering “Is MariBank safe?”, you are not alone. As a fully digital bank by Sea Limited — the company behind Shopee and Garena — MariBank has attracted both curiosity and scepticism from Singapore savers since its 2023 launch.

The short answer: yes, MariBank is safe by the same regulatory standards as DBS, OCBC, and UOB. It holds a Digital Full Bank (DFB) licence from the Monetary Authority of Singapore (MAS) and is a member of the Singapore Deposit Insurance Corporation (SDIC) scheme, meaning eligible deposits up to S$100,000 per depositor are insured.

But “safe” means different things to different people. In this guide we unpack exactly what protections are in place, where MariBank fits in the Singapore fintech ecosystem, and how it compares to robo-advisors like Endowus, Syfe, and FSMOne for growing your money.

Table of Contents

Contents — Click to expand

- MariBank’s MAS Digital Full Bank Licence

- SDIC Deposit Insurance — What S$100k Protection Means

- Who Owns MariBank? Sea Limited’s Track Record

- MariBank Features: Savings, Fixed Deposit & Mari Invest

- MariBank vs Endowus, Syfe & FSMOne — What Each Is Best For

- What About Trust Bank? Another Digital Bank Option

- The Verdict: Is MariBank Safe for Singaporeans?

- FAQ

1. MariBank’s MAS Digital Full Bank Licence

MariBank is licensed by MAS as a Digital Full Bank (DFB) — one of only two such licences awarded in Singapore (the other went to GXS Bank, backed by Grab and Singtel). This is not a lightweight fintech exemption; DFB licence holders must meet the same core capital, liquidity, and governance requirements as traditional banks.

What this means for you as a depositor:

- MariBank must maintain minimum capital buffers set by MAS.

- It is subject to regular MAS supervisory examinations.

- It must follow the same anti-money-laundering (AML) and know-your-customer (KYC) rules as any bank in Singapore.

- MAS can intervene if MariBank’s financial health deteriorates.

In short, MariBank operates under the same regulatory umbrella as Singapore’s established banks — just without physical branches.

2. SDIC Deposit Insurance — What S$100k Protection Means

MariBank is a full member of the Singapore Deposit Insurance Corporation (SDIC) scheme. Under this scheme:

- Eligible deposits (SGD current and savings accounts, fixed deposits) are insured up to S$100,000 per depositor per bank.

- If MariBank were to fail, SDIC would pay out insured depositors as quickly as possible — historically within a few days for SDIC scheme payouts.

- Foreign currency deposits, structured deposits, and investment products (including Mari Invest) are not covered by SDIC.

For most Singaporeans keeping their emergency fund or savings in MariBank, the S$100k SDIC coverage is more than adequate. If you hold more than S$100k, consider spreading it across multiple SDIC member banks.

3. Who Owns MariBank? Sea Limited’s Track Record

MariBank is a wholly-owned subsidiary of Sea Limited (NYSE: SE), Singapore’s largest technology company and the parent of Shopee, Garena, and SeaMoney. Sea Limited is NYSE-listed, regularly audited, and had a market capitalisation above US$50 billion at its peak.

Sea Limited’s digital financial services arm (SeaMoney) has been operating across Southeast Asia since 2014. MariBank represents its Singapore-specific regulated banking entity, bringing that regional fintech experience under the stricter governance of a MAS-licensed bank.

While Sea’s share price has been volatile — as with most tech companies — MariBank’s deposits are protected by the SDIC scheme regardless of Sea Limited’s stock performance. Regulatory capital and deposit insurance exist precisely to insulate depositors from parent-company risks.

4. MariBank Features: Savings, Fixed Deposit & Mari Invest

Once you are satisfied MariBank is safe, the next question is whether it is actually worth using. Here is what the platform currently offers (as at May 2026):

| Product | Rate / Feature | SDIC Covered? |

|---|---|---|

| Mari Savings Account | 0.88% p.a. flat, no conditions, daily interest crediting | Yes (up to S$100k) |

| Mari Fixed Deposit | Competitive promotional rates; check app for current offers | Yes (up to S$100k) |

| Mari Invest | Unit trusts & money market funds via the app | No (investment product) |

| Mari Debit / Credit Card | Cashback on Shopee & daily spend; no annual fee options | N/A |

*Rates as at May 2026. Always verify current rates in the MariBank app.*

The 0.88% p.a. savings rate is no-frills but genuinely hassle-free — no salary crediting, no minimum balance, no spend requirements. For a pure emergency fund parking spot, it competes favourably against many traditional banks’ base rates.

5. MariBank vs Endowus, Syfe & FSMOne — What Each Is Best For

A common misconception is that MariBank competes directly with robo-advisors like Endowus or Syfe. They serve different purposes. Here is a plain-English breakdown:

| Platform | Type | Best For | CPF Investing? |

|---|---|---|---|

| MariBank | Digital Bank | SDIC-insured savings, fixed deposits, everyday banking | No |

| Endowus | Robo-Advisor / Fund Platform | CPF OA/SA investing, SRS, long-term portfolio building | Yes (only platform) |

| Syfe | Robo-Advisor | REIT+, Income+, Cash+, flexible goal-based investing | No |

| FSMOne | Fund Supermart / Broker | DIY fund investing, ETFs, bonds, RSS investing | Limited (CPFIS) |

The smart Singapore investor typically uses a combination: MariBank or Trust Bank for emergency fund savings, Endowus for CPF and SRS money, Syfe for discretionary income-generating portfolios, and FSMOne for DIY ETF or bond investing.

Referral Codes & Sign-Up Bonuses (May 2026)

If you are ready to sign up for any of these platforms, TKN has dedicated referral code pages with the latest bonuses verified monthly:

6. What About Trust Bank? Another Digital Bank Option

Trust Bank, launched by Standard Chartered and FairPrice Group, is MariBank’s closest peer in the Singapore digital banking space. Like MariBank, Trust Bank is MAS-licensed and SDIC-covered for eligible deposits up to S$100,000.

Key differences worth noting:

- Trust Bank is backed by Standard Chartered — a 160-year-old global bank — which may give some depositors greater comfort.

- Trust Bank’s savings rates and credit card cashback are structured differently — check current offers before deciding.

- Both MariBank and Trust Bank are strong options for your emergency fund; many Singaporeans hold accounts at both.

Read our full Trust Bank referral code and review page for the latest sign-up bonuses.

7. The Verdict: Is MariBank Safe for Singaporeans?

Yes — MariBank is safe by Singapore’s rigorous banking standards. Here is the summary checklist:

- ✅ MAS Digital Full Bank Licence (one of only two awarded)

- ✅ SDIC-insured deposits up to S$100,000 per depositor

- ✅ Backed by Sea Limited, a NYSE-listed company with strong regional operations

- ✅ Industry-standard encryption, 2FA, and fraud monitoring

- ⚠️ Mari Invest products are not SDIC-covered (investment risk applies)

- ⚠️ No physical branches — customer service is app/chat-based only

For parking your emergency fund or short-term savings, MariBank’s no-frills 0.88% p.a. with full SDIC coverage is a solid choice. For growing your wealth through CPF, SRS, or diversified portfolios, pair it with Endowus (CPF OA/SA), Syfe (income portfolios), or FSMOne (DIY ETFs).

Want to learn more about building a well-rounded Singapore investment portfolio? Check our guides on CPF investment strategy, best S-REITs 2026, and the best robo-advisor comparison.

FAQ — Is MariBank Safe?

Is MariBank regulated by MAS?

Is my money in MariBank insured?

What happens to my MariBank deposits if the bank fails?

Is MariBank safe compared to DBS or OCBC?

Should I use MariBank or Endowus for investing?

What is the MariBank savings account interest rate in 2026?

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.