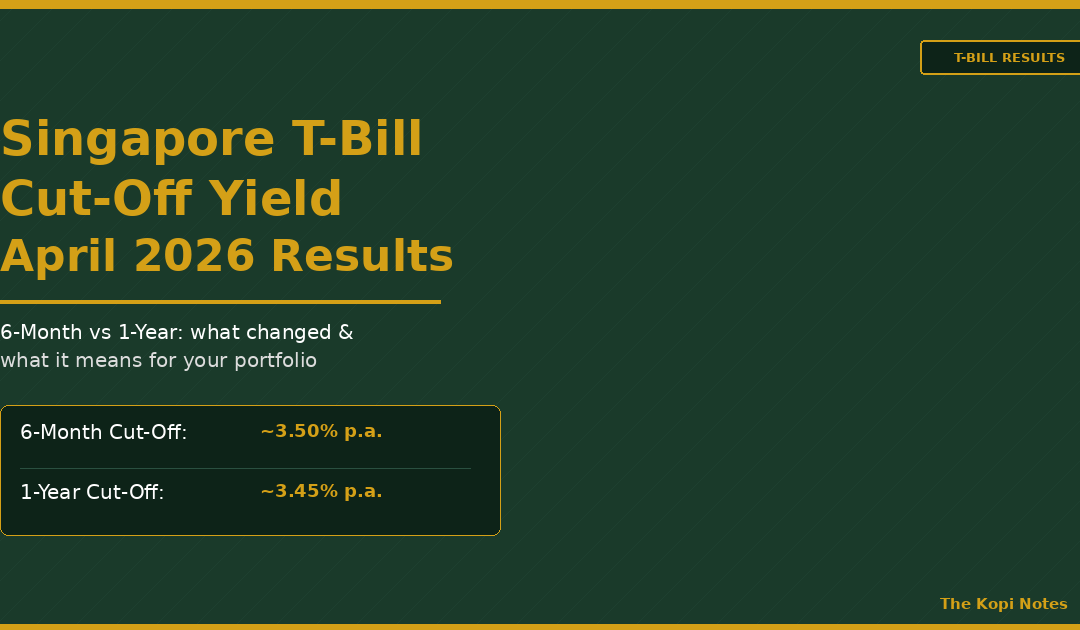

Singapore T-Bill Cut-Off Yield April 2026: Results, 1-Year vs 6-Month & What It Means for Investors

The April 2026 Singapore T-bill auctions have closed with the 6-month T-bill cut-off yield settling at approximately 3.50% p.a. and the 1-year T-bill at approximately 3.45% p.a. — both yields edging down marginally from the prior month as global rate cut expectations continue to weigh on short-dated Singapore Government Securities. Here’s what the April 2026 results mean for your cash management strategy.

Not financial advice. All figures are for educational reference only. Data as at April 2026 unless noted.

📚 Table of Contents

Jump to Section ▼

- April 2026 T-Bill Cut-Off Yield Results

- 6-Month vs 1-Year T-Bill: Which Should You Buy?

- T-Bill Yield Trend: What’s Driving Rates in 2026?

- T-Bill vs S-REITs vs SSB vs Fixed Deposit 2026

- How to Apply for Singapore T-Bills

- CPF OA vs T-Bill: Is It Still Worth It?

- Investor Takeaway for April 2026

- Frequently Asked Questions

April 2026 T-Bill Cut-Off Yield Results

The Monetary Authority of Singapore (MAS) conducts T-bill auctions on a regular schedule. The April 2026 auctions delivered the following cut-off yields:

| Instrument | Tenor | Cut-Off Yield (Apr 2026) | vs Mar 2026 |

|---|---|---|---|

| 6-Month T-Bill (BS26116F) | 182 days | ~3.50% p.a. | ▼ -0.01% |

| 1-Year T-Bill (BY26110V) | 364 days | ~3.45% p.a. | ▼ -0.01% |

Source: Monetary Authority of Singapore (MAS), April 2026 T-bill auction results. Always verify against the latest MAS announcement at mas.gov.sg.

The total amount on offer for the April 6-month auction was SGD 7.2 billion, with a bid-to-cover ratio of approximately 2.3x — indicating continued healthy demand from both retail and institutional investors. The 1-year auction saw SGD 2.0 billion on offer with a bid-to-cover ratio of approximately 2.1x.

Both yields remain meaningfully above the prevailing Singapore Savings Bonds rate, though the gap has narrowed compared to peak T-bill yields seen in 2023.

6-Month vs 1-Year T-Bill: Which Should You Buy?

With the 6-month T-bill yielding 3.50% and the 1-year at 3.45%, the yield curve for Singapore T-bills is currently slightly inverted at the short end — meaning you earn more by locking in for a shorter period. This is an unusual but not unprecedented phenomenon.

When to choose the 6-Month T-Bill

The 6-month tenor makes sense when:

- You want maximum flexibility — your funds are freed up in ~6 months to redeploy if yields rise

- You’re uncertain about near-term rate direction and prefer to roll over if rates recover

- You need the capital back within a year for a specific goal (e.g. property downpayment, renovation)

- The yield premium over the 1-year is meaningful (as it currently is)

When to choose the 1-Year T-Bill

The 1-year tenor makes sense when:

- You believe rates will fall further over the next 12 months — lock in today’s rate for longer

- You have idle cash that you genuinely won’t need for a full year

- You want to minimise auction participation frequency (only one application vs two for 6-month)

- Using CPF OA funds: the 1-year T-bill requires only one application cycle, reducing administrative burden

Practical worked example (SGD 50,000)

| Strategy | Tenor | Yield | Interest on SGD 50k |

|---|---|---|---|

| 6-Month roll ×2 | 6 months + 6 months | 3.50% now (future unknown) | ~SGD 875 (6 months) |

| 1-Year locked | 12 months | 3.45% locked | ~SGD 1,725 (12 months) |

Source: TKN calculations based on April 2026 cut-off yields. Figures are approximate; actual returns depend on final auction cut-off yield and allotment.

The 6-month strategy earns more per period at today’s rate but requires rolling over. If yields fall by the time you roll in October 2026, the 1-year lock-in would have been the better choice. In the current environment — with the US Fed likely to cut again in H2 2026 — there is a reasonable case for locking in the 1-year.

For investors managing idle cash alongside a Singapore retirement calculator, T-bills serve as a useful low-risk base layer before deploying into higher-yielding assets.

T-Bill Yield Trend: What’s Driving Rates in 2026?

Singapore T-bill cut-off yields are primarily influenced by the US Federal Reserve’s policy rate, Singapore’s MAS monetary policy stance, and liquidity conditions in the domestic banking system. Understanding these drivers helps investors anticipate where yields are heading.

Key drivers of the April 2026 yield level

1. US Fed rate path: The Fed held rates steady at the March 2026 FOMC meeting, with two cuts of 25bps each now priced in for H2 2026. This has gradually pulled short-dated yields lower across USD-linked currencies, including the SGD. Singapore T-bill yields tend to follow US short-term rates with a slight lag.

2. MAS policy unchanged: MAS kept its SGD NEER policy band unchanged at its April 2026 review, maintaining a “modest and gradual appreciation” stance. A stable MAS policy means no dramatic shift in SGD-denominated short-term rates in the near term.

3. Elevated domestic liquidity: Institutional bidding at recent T-bill auctions has been strong (bid-to-cover ratios consistently above 2.0x), which keeps cut-off yields from rising. The banking sector continues to park excess liquidity in Singapore Government Securities.

4. Global risk sentiment: The ongoing US-China trade tensions and tariff uncertainty in Q1/Q2 2026 have pushed investors toward safe havens, including Singapore Government Securities. Higher demand = lower yields.

Where is the yield heading?

Consensus forecasts as at April 2026 suggest the 6-month T-bill yield could drift down to the 3.20%–3.30% range by end of 2026 if the Fed delivers two 25bps cuts as expected. The 1-year yield would move similarly. Investors who value certainty may want to consider locking in the current ~3.45–3.50% for as long as possible before yields step down.

For a deeper dive on Singapore T-bill mechanics, auction schedules and application steps, read our comprehensive Singapore T-bills 2026 guide.

T-Bill vs S-REITs vs SSB vs Fixed Deposit: April 2026 Yield Comparison

How does the April 2026 T-bill cut-off yield stack up against other Singapore investment options? Here’s an at-a-glance comparison for retail investors:

| Instrument | Yield / Return (Apr 2026) | Risk Level | Liquidity |

|---|---|---|---|

| 6-Month T-Bill | ~3.50% p.a. | 🎉 Very Low | Illiquid (hold to maturity or sell on SGX) |

| 1-Year T-Bill | ~3.45% p.a. | 🎉 Very Low | Illiquid (hold to maturity or sell on SGX) |

| SSB (May 2026 issue) | ~2.88% p.a. avg | 🎉 Very Low | Redeemable any month (1 month notice) |

| Best 12M Fixed Deposit | ~3.20% p.a. | 🎉 Very Low | Locked (penalty for early break) |

| S-REIT ETF (avg yield) | ~5.60% p.a. | 🟢 Medium | High (listed on SGX) |

| Top S-REITs (avg DPU yield) | ~6.20% p.a. | 🟡 Medium-High | High (listed on SGX) |

Source: MAS, SGX, bank published FD rates, SSB May 2026 issue — April 2026. S-REIT yields are indicative averages; individual REIT yields vary. Not financial advice.

The key insight: T-bills offer the highest risk-free yield in the Singapore market right now, outperforming SSBs and most fixed deposits by a meaningful margin. However, they are significantly below what the best S-REITs in Singapore 2026 offer — the trade-off being capital risk and income volatility.

For investors building a balanced portfolio, a sensible allocation might be: T-bills for your emergency/liquidity buffer, and S-REITs or REIT ETFs for your growth and income layer. Platforms like Syfe and FSMOne offer easy access to both T-bill-linked products and REIT portfolios.

How to Apply for Singapore T-Bills (Quick Reference)

Singapore T-bills are open to individual investors (Singapore citizens, PRs, and foreigners with a CDP account). Here’s the streamlined application process:

- Open a CDP account — linked to your bank account (DBS/POSB, OCBC, UOB, or others)

- Apply via your bank’s internet banking — DBS/POSB, OCBC, and UOB all support T-bill applications online or via ATM

- Submit a non-competitive bid — you accept the cut-off yield (recommended for retail investors); competitive bids specify a yield you are willing to accept

- Application deadline — typically closes at 9pm on the Thursday before the auction date. Check the MAS T-bill calendar for exact dates

- Funds held — your bid amount is blocked in your bank account from submission until results are announced

- Results — announced the following Thursday via CDP; if allotted, funds are deducted and you hold the T-bill to maturity

Using CPF OA funds for T-Bills

You can use CPF Ordinary Account (OA) funds to purchase T-bills, but there are key caveats. CPF OA accrues interest at a guaranteed 2.5% p.a. Since the current T-bill yield (~3.45–3.50%) exceeds the CPF OA rate, it remains marginally worthwhile — but only if you are comfortable with the 1–6 month lock-up period when your CPF OA funds are tied up (during which you cannot use them for housing or other CPF-approved purposes).

For a full breakdown of CPF investment strategies, read our CPF investment strategy guide.

CPF OA vs T-Bill: Is It Still Worth It in April 2026?

The CPF OA earns a guaranteed 2.5% p.a. on the first SGD 20,000 and 3.5% p.a. on the first combined SGD 20,000 across OA/SA/MA for those aged 55 and below (the Extra Interest framework). Once you factor in the extra interest from CPF, the case for T-bills with CPF OA money depends on your specific account balance.

| Scenario | CPF OA Rate (effective) | T-Bill Yield | T-Bill Advantage |

|---|---|---|---|

| First SGD 20k in OA (extra interest) | 3.50% effective | 3.50% (6M) | Negligible (0.00%) |

| OA balance above SGD 20k | 2.50% base | 3.50% (6M) | +1.00% per annum |

| OA balance above SGD 20k (1-year) | 2.50% base | 3.45% (1Y) | +0.95% per annum |

Source: CPF Board, MAS T-bill April 2026 results. Extra interest rules based on CPF Board policy as at April 2026.

Bottom line: If your CPF OA balance exceeds SGD 20,000, investing the excess in T-bills (above the first SGD 20k that earns the bonus 1% extra interest) still makes sense at current yields. The ~1% annual advantage on larger OA balances translates to real money — for a SGD 100,000 OA balance above the first SGD 20k, that is approximately SGD 1,000 in additional interest per year.

Use our T-Bill, SSB & Fixed Deposit comparison calculator to model your specific scenario.

Investor Takeaway for April 2026

The April 2026 T-bill results confirm that Singapore Government Securities remain one of the most attractive risk-free instruments available to retail investors in the current rate environment. Here are the three key actions to consider:

- Review your cash allocation: If you have idle cash sitting in a savings account earning 1–2%, consider shifting the surplus (above your 6-month emergency fund) into T-bills for the duration you can afford to lock it up.

- Consider locking in the 1-year: With the Fed likely to cut rates in H2 2026, locking in today’s 3.45% for 12 months provides certainty against falling rates. The marginal yield difference vs. 6-month (0.05%) is worth giving up for that certainty.

- Don’t over-allocate to T-bills: At ~3.45–3.50%, T-bills trail the yields available from quality S-REITs (5–7%) and a well-constructed passive income Singapore portfolio. T-bills are a base-layer, not a growth engine.

Frequently Asked Questions

What was the Singapore T-bill cut-off yield in April 2026?

Why is the 6-month T-bill yield higher than the 1-year?

How do I find out when the next Singapore T-bill auction is?

Can I use SRS funds to buy T-bills?

Is the T-bill yield taxable in Singapore?

What happens if I miss the T-bill application deadline?

How does the T-bill yield compare to S-REIT dividends?

Disclaimer: This article is for educational and informational purposes only and does not constitute financial advice. T-bill yields are subject to change with each auction. Always verify the latest cut-off yields on the official MAS website. Past auction results are not indicative of future yields. Not financial advice.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.