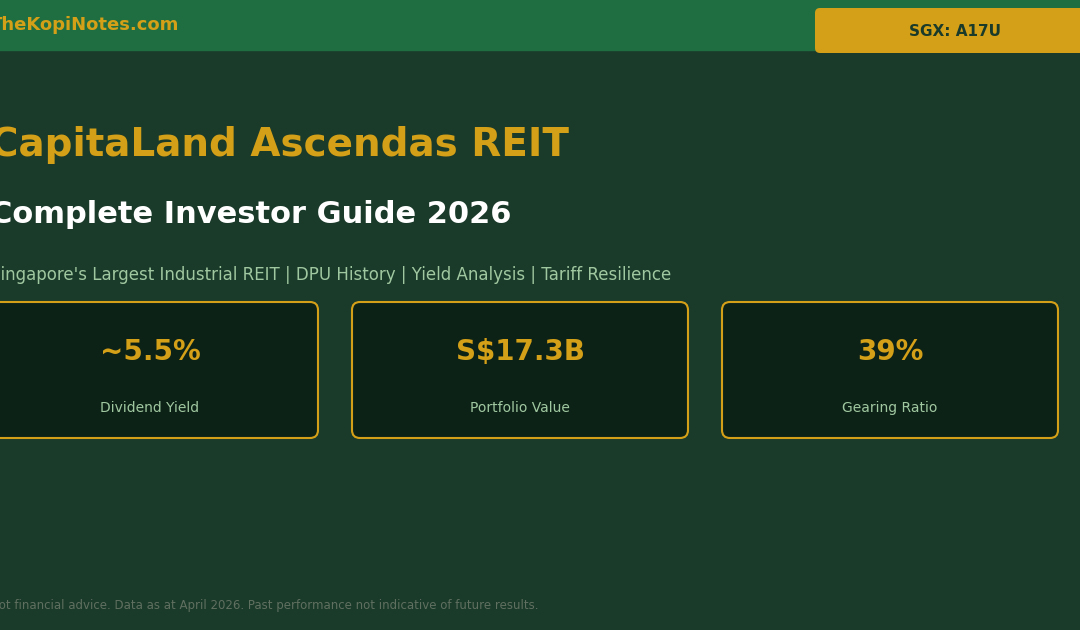

CapitaLand Ascendas REIT (A17U): Complete Investor Guide 2026

Singapore’s largest industrial REIT — S$17.3B portfolio, ~5.5% yield, 220+ properties across Asia-Pacific, Europe & USA. Everything you need to know before investing.

CapitaLand Ascendas REIT (SGX: A17U, formerly Ascendas REIT) is Singapore’s largest industrial REIT and the country’s first and largest business space and industrial REIT. Managed by CapitaLand Investment Limited (CLI), it is one of the foundational S-REITs that every Singapore dividend investor should understand.

As at April 2026, A17U trades at approximately S$2.75 per unit, offering a trailing dividend yield of around 5.5%. With a portfolio value of S$17.3 billion across 220+ properties, A17U provides direct exposure to logistics, business parks, hi-tech industrial, and data centre assets in Singapore, Australia, the United Kingdom, Europe, and the United States.

This guide is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Always conduct your own due diligence before investing.

Table of Contents

Contents — Click to expand

- Key Facts & Quick Stats (April 2026)

- What Is CapitaLand Ascendas REIT?

- Portfolio Overview: 220+ Properties Across 6 Markets

- DPU History & Dividend Track Record

- Yield Comparison: A17U vs S-REIT Peers

- Financial Health: Gearing, ICR & Debt Profile

- Tariff & Macro Resilience: Why Industrial REITs Hold Up

- Investment Thesis: Bull vs Bear Case

- How to Invest in A17U via CPF/SRS

- FAQ

Key Facts & Quick Stats (April 2026)

| Metric | Value |

|---|---|

| SGX Ticker | A17U |

| Full Name | CapitaLand Ascendas REIT (formerly Ascendas REIT) |

| Share Price (Apr 2026) | ~S$2.75 |

| Market Capitalisation | ~S$11.4B |

| Portfolio Value (AUM) | S$17.3B |

| Number of Properties | 220+ across 6 countries |

| Trailing DPU (FY2024) | 15.108 Singapore cents |

| Dividend Yield | ~5.5% (trailing) |

| Gearing Ratio | ~39% |

| Distribution Frequency | Semi-annual (2x per year) |

| Manager | CapitaLand Investment Limited (CLI) |

| CPF/SRS Eligible | Yes (CPF Investment Scheme) |

What Is CapitaLand Ascendas REIT?

CapitaLand Ascendas REIT was launched in 2002 as Ascendas Real Estate Investment Trust — Singapore’s first listed business space and industrial REIT. In 2021, following CapitaLand’s restructuring, the REIT was renamed to CapitaLand Ascendas REIT (CLAR). It trades on the SGX under ticker A17U.

Unlike retail S-REITs (malls) or hospitality REITs, A17U owns business and industrial real estate — properties that house manufacturing, logistics, data infrastructure, and knowledge-economy businesses. This gives it a fundamentally different demand driver: industrial and technology-driven tenancy rather than consumer spending.

Key property types in the CLAR portfolio include:

- Logistics & Distribution Centres — Last-mile delivery hubs and warehouses

- Business Parks & Science Parks — High-specification office/lab spaces for tech and biomedical firms

- Hi-Tech Industrial — Manufacturing and R&D facilities with heavy power loads

- Data Centres — Hyperscale and colocation facilities in Singapore and overseas

- Suburban Offices — Mixed-use business space in decentralised locations

Its sponsor, CapitaLand Investment Limited (CLI), is one of Southeast Asia’s largest real estate investment managers, listed on the SGX. CLI provides deal pipeline, asset management expertise, and balance sheet support — a key structural advantage for CLAR’s long-term growth.

Portfolio Overview: 220+ Properties Across 6 Markets

As at end-2024, CapitaLand Ascendas REIT holds 222 properties valued at approximately S$17.3 billion. The portfolio is diversified across Singapore, Australia, the United Kingdom, the United States, Europe, and select Southeast Asian markets.

Geographic Breakdown (by AUM)

| Geography | % of Portfolio | Key Assets |

|---|---|---|

| Singapore | ~59% | LogisPark, Science Park, Changi Business Park |

| Australia | ~21% | Business parks in Sydney, Melbourne, Brisbane |

| UK/Europe | ~13% | Logistics parks, R&D campuses in UK and Europe |

| USA | ~7% | Data centres, life science parks |

Asset Type Mix (by AUM)

| Asset Type | % of Portfolio |

|---|---|

| Logistics & Distribution | ~26% |

| Business & Science Parks | ~28% |

| Hi-Tech Industrial | ~28% |

| Data Centres | ~18% |

The occupancy rate across the portfolio stood at approximately 91–92% as at end-2024, with Singapore properties at a higher occupancy (~94%) due to strong local industrial demand. The WALE (weighted average lease expiry) is approximately 3.8 years, providing near-term income visibility.

DPU History & Dividend Track Record

CapitaLand Ascendas REIT distributes dividends semi-annually. Below is the annual DPU (Distribution Per Unit) track record in Singapore cents.

| Financial Year | DPU (SGD Cents) | YoY Change |

|---|---|---|

| FY2019 | 15.62¢ | — |

| FY2020 | 13.38¢ | −14.3% (COVID-19) |

| FY2021 | 14.288¢ | +6.8% (recovery) |

| FY2022 | 15.258¢ | +6.8% |

| FY2023 | 15.468¢ | +1.4% |

| FY2024 | 15.108¢ | −2.3% (higher interest costs) |

| FY2025e | ~15.2¢ (est.) | +0.6% (consensus) |

The FY2020 dip was COVID-induced — A17U granted rental rebates to industrial and logistics tenants affected by the pandemic. The FY2024 slight decline reflected higher borrowing costs as the REIT refinanced debt in a higher interest rate environment. With the US Federal Reserve cutting rates from 2024 and the MAS easing SGD NEER policy, DPU pressure from financing costs is expected to ease in FY2025–2026.

Yield Comparison: A17U vs S-REIT Peers

How does CapitaLand Ascendas REIT’s yield stack up against other Singapore REITs? The table below compares trailing dividend yields as at April 2026.

| S-REIT | SGX Ticker | Sector | Yield (Apr 2026) |

|---|---|---|---|

| CapitaLand Ascendas REIT | A17U | Industrial/Diversified | ~5.5% |

| Keppel DC REIT | AJBU | Data Centre | ~4.2% |

| Mapletree Logistics Trust | M44U | Logistics | ~6.4% |

| MPACT | N2IU | Retail/Commercial | ~6.1% |

| Frasers Centrepoint Trust | J69U | Retail | ~5.3% |

| Suntec REIT | T82U | Office/Retail | ~5.1% |

| Starhill Global REIT | P40U | Retail/Hotel | ~6.7% |

A17U sits in the mid-range of S-REIT yields. At ~5.5%, it does not offer the highest distribution among its peers, but it compensates with institutional quality, a large diversified portfolio, and sponsor backing from CLI. The lower yield relative to MLT or Starhill reflects the market’s perception of CLAR’s lower risk profile and its data centre/high-tech exposure.

You can compare S-REIT yields interactively using our S-REIT Yield vs SGS Bond Spread Calculator and our REITs Dividend Yield Calculator.

Financial Health: Gearing, ICR & Debt Profile

Strong balance sheet management is critical for any S-REIT investor. MAS regulations cap S-REIT gearing at 50% (with conditions), with a 45% limit as the standard threshold. Here is CLAR’s financial health snapshot as at end-2024.

| Metric | FY2024 | Assessment |

|---|---|---|

| Gearing Ratio | ~39% | Comfortable — 6% headroom to MAS limit |

| Interest Coverage Ratio (ICR) | ~3.7x | Above MAS 1.5x minimum threshold |

| Weighted Avg. Debt Cost | ~3.7% p.a. | Manageable; improving with rate cuts |

| % Debt Fixed Rate | ~77% | Good rate protection |

| Weighted Avg. Debt Tenor | ~3.7 years | Well-laddered maturity profile |

With 77% of its debt on fixed rates and a well-laddered debt maturity profile, CLAR has reduced its sensitivity to floating interest rate movements. The gearing at ~39% is comfortably below the MAS 45% aggregate leverage limit, giving management flexibility for acquisitions without needing to issue new units (which would dilute existing unitholders).

Use our S-REIT Gearing Ratio & ICR Calculator to model how changes in property values would affect A17U’s gearing headroom.

Tariff & Macro Resilience: Why Industrial REITs Hold Up

With the 2026 US tariff shock rattling global supply chains, many Singapore investors are wondering how S-REITs will fare. CapitaLand Ascendas REIT’s industrial and logistics focus gives it a nuanced resilience profile.

Why CLAR is More Resilient Than Retail REITs

- Industrial demand is structural: Tariffs accelerate supply chain regionalisation. Companies are increasing their warehouse and logistics footprints in Southeast Asia to buffer against trade disruptions — directly benefiting logistics REIT landlords in Singapore.

- Data centre assets are tariff-agnostic: Cloud, AI, and digital infrastructure demand is driven by technology adoption, not trade flows. CLAR’s ~18% data centre weighting provides a defensive growth pillar.

- Long lease terms: CLAR’s industrial leases average 3–5 years, with many multi-national tenants on longer leases. Short-term macro volatility has limited immediate impact on DPU.

- Geography diversification: With 41% of AUM outside Singapore (Australia, UK, USA), CLAR is not fully correlated to Singapore’s trade cycle.

Risks to Monitor

- Currency risk: ~41% overseas assets means AUD, GBP, EUR, and USD fluctuations affect SGD-reported DPU. A strong SGD headwinds overseas income.

- Occupancy softening in business parks: Singapore’s suburban business park space has faced some tenant exits as MNCs rationalise office footprints post-pandemic.

- Interest rate duration risk: Even with 77% fixed-rate debt, the remaining 23% floating exposure and debt maturities mean higher rates for longer would compress DPU margins on refinancing.

Investment Thesis: Bull vs Bear Case

Bull Case for A17U

- Rate cycle tailwind: As US Fed and MAS ease monetary conditions, refinancing costs fall, directly improving DPU. Every 50bps rate decline adds approximately 0.3–0.5¢ per unit to DPU.

- AI/data centre growth: Singapore is positioned as Southeast Asia’s data centre hub. Demand for power-dense industrial and data centre space is structurally growing, and CLAR has existing assets and pipeline from CLI to capitalise.

- Sponsor pipeline advantage: CLI’s massive global real estate portfolio provides CLAR with a visible acquisition pipeline at fair valuations — a key advantage over internally managed REITs.

- Supply chain nearshoring: Tariff-driven supply chain shifts are creating industrial demand in Australia and Southeast Asia, where CLAR has significant exposure.

Bear Case / Risks

- Premium unit price: At ~S$2.75, A17U trades near book value. There is limited discount to NAV, unlike some smaller S-REITs. Capital appreciation potential may be capped.

- Business park vacancy: Suburban office / business park demand has been uneven. If tech MNCs continue to downsize Singapore office footprints, this segment could see higher vacancies.

- Rights issue risk: If interest rates stay elevated and properties need capital recycling, CLAR may need to raise equity (dilutive to unitholders).

For most Singapore long-term dividend investors, A17U’s bull case outweighs the bear risks. Its large diversified portfolio, sponsor backing, and structural exposure to logistics and data centres make it a core S-REIT holding. Compare it against the broader S-REIT landscape in our Best S-REITs Singapore 2026 Guide.

How to Invest in A17U via CPF/SRS

CapitaLand Ascendas REIT (A17U) is eligible under the CPF Investment Scheme (CPFIS), meaning Singapore residents can use CPF Ordinary Account (OA) savings to purchase units on the SGX. This is a significant advantage for CPF investors seeking higher yields than the 2.5% OA rate.

Step-by-Step: Buying A17U via CPF

- Ensure your CPF OA balance exceeds S$20,000 (minimum retained balance requirement for CPFIS)

- Open a CPFIS investment account with a participating broker (DBS, OCBC, UOB, or robo-advisors like Endowus)

- Search for ticker A17U on the SGX or your broker’s platform

- Place a buy order — minimum 1 lot (100 units) = ~S$275

- Dividends paid semi-annually will flow back to your CPFIS account

Using SRS to Buy A17U

A17U is also purchasable using SRS (Supplementary Retirement Scheme) funds via most brokerage platforms. Combining SRS contributions with S-REIT distributions is a powerful strategy for tax-efficient retirement income. Use our SRS Tax Savings Calculator to quantify your savings.

For a broader robo-advisor approach to S-REIT investing without single-stock selection, consider Syfe Income+ or the Singapore REIT ETF (NikkoAM-StraitsTrading Asia ex Japan REIT ETF).

If you are planning your full retirement income strategy, our Retirement Planning Calculator can show you how A17U distributions fit into your projected passive income target.

Frequently Asked Questions

What is CapitaLand Ascendas REIT?

What is A17U's current dividend yield?

What is CLAR's gearing ratio?

What is CLAR's gearing ratio?

How does the tariff environment affect CapitaLand Ascendas REIT?

What is the minimum investment in A17U?

How often does CapitaLand Ascendas REIT pay dividends?

Start Investing Smarter in S-REITs

Open a brokerage account and get started with S-REIT investing. Our referral partners offer fee rebates and cashback for new accounts.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.