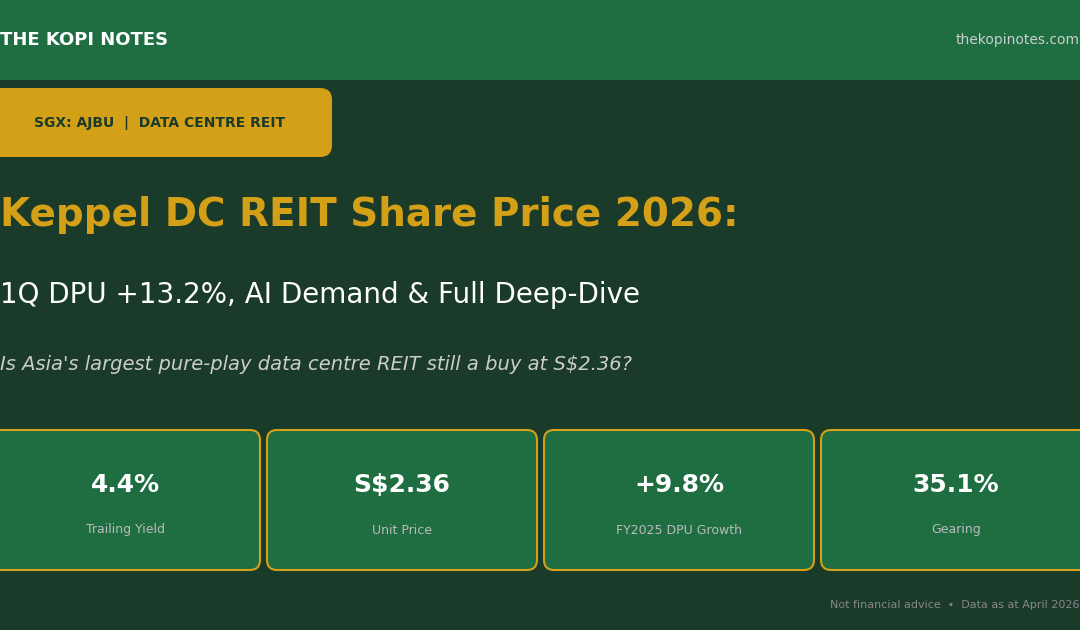

Keppel DC REIT Share Price 2026: 1Q DPU +13.2%, AI Demand & Full Deep-Dive

Keppel DC REIT (SGX: AJBU) is Asia’s largest pure-play data centre REIT, riding the structural tailwind of AI compute demand, cloud migration and digital infrastructure spending. In this deep-dive we break down the 1Q 2026 results, DPU history, portfolio composition, balance sheet health and whether the current share price of S$2.36 offers value for Singapore investors.

Disclaimer — This article is for informational purposes only and does not constitute financial advice. All data as at April 2026 unless stated otherwise.

Table of Contents

Contents — Click to expand

- Keppel DC REIT at a Glance

- Share Price Performance & Valuation

- 1Q 2026 Results Breakdown

- DPU History (2016–2025)

- Portfolio Deep-Dive: 25 Data Centres Across 10 Countries

- Balance Sheet & Gearing Analysis

- Growth Catalysts: AI, Hyperscale & Rental Reversions

- Peer Comparison: How Does Keppel DC Stack Up?

- Key Risks to Watch

- Should You Buy Keppel DC REIT in 2026?

- FAQ

1. Keppel DC REIT at a Glance

Listed on the SGX in December 2014, Keppel DC REIT was the first pure-play data centre REIT in Asia. It is managed by Keppel DC REIT Management Pte. Ltd., a wholly-owned subsidiary of Keppel Ltd — one of Singapore’s largest conglomerates with deep infrastructure expertise.

| Metric | Value |

|---|---|

| SGX Ticker | AJBU |

| Unit Price (Apr 2026) | S$2.36 |

| Market Cap | ~S$6.2B |

| NAV per Unit | S$1.71 |

| P/NAV | 1.38× |

| FY2025 DPU | 10.381¢ |

| Trailing Yield | ~4.4% |

| Gearing | 35.1% |

| Portfolio AUM | S$6.3B |

| Properties | 25 data centres, 10 countries |

| WALE | 6.5 years |

At a trailing yield of ~4.4%, Keppel DC REIT trades at a premium to the broader S-REIT sector (~5.7% average). That premium reflects the market’s confidence in data centre demand, which is being supercharged by AI training workloads and cloud adoption across Asia Pacific.

2. Share Price Performance & Valuation

Keppel DC REIT’s unit price traded at S$2.36 as at 16 April 2026, giving it a price-to-NAV ratio of 1.38×. This compares to the broader S-REIT sector average P/NAV of ~0.9×, underscoring the premium investors are willing to pay for secular growth in data centres.

The consensus 12-month analyst target price stands at S$2.53–S$2.61, with a range of S$2.30 (low) to S$2.82 (high). All 13 covering analysts carry a “Buy” or equivalent rating — reflecting strong conviction in the REIT’s growth trajectory.

Key valuation context:

- P/NAV of 1.38× is the highest among Singapore-listed REITs — justified by 10 consecutive years of DPU growth and the AI-driven demand tailwind

- Forward yield of ~4.7–4.9% (FY2026–28F consensus) vs risk-free 10-year SGS yield of ~2.3% — a spread of ~2.4–2.6%

- Digital Core REIT (SGX: DCRU), the only other pure-play data centre REIT on SGX, trades at a 7.2% yield but with a smaller, North America-focused portfolio

For investors building a best S-REITs portfolio, Keppel DC REIT occupies the “growth at a premium” slot — lower yield, but structurally higher DPU growth visibility than traditional retail or office REITs.

3. 1Q 2026 Results Breakdown

The 1Q 2026 operational update (released 16 April 2026) showed continued momentum across all key metrics:

| Metric | 1Q 2026 | 1Q 2025 | YoY Change |

|---|---|---|---|

| Gross Revenue | S$121.0M | S$102.2M | +18.4% |

| Net Property Income | S$105.2M | S$88.1M | +19.4% |

| Distributable Income | S$74.6M | S$61.8M | +20.7% |

| DPU | 2.833¢ | 2.503¢ | +13.2% |

| Portfolio Occupancy | 95.6% | — | — |

The standout figure is the 51% rental reversion achieved in 1Q 2026 — driven by below-market legacy contracts being renewed at current market rates. This is a powerful DPU growth lever that will continue as older leases come up for renewal over the next 2–3 years.

Revenue and NPI growth were supported by the full-quarter contribution of acquisitions completed in FY2025 (~S$1.1 billion in new assets including Tokyo Data Centre 3 and remaining interests in Singapore data centres).

4. DPU History (2016–2025)

Keppel DC REIT has delivered DPU growth in 9 of the last 10 financial years — a track record unmatched by most S-REITs. The only dip came in FY2023 (9.383¢ vs FY2022’s 10.214¢), primarily due to the enlarged unit base from the preferential offering and the impact of higher interest rates on borrowing costs.

FY2025 DPU of 10.381¢ marked a new all-time high — up 9.8% YoY despite the enlarged unitholder base following the October 2025 preferential offering. Distributable income surged 55.2% to S$268.1 million on the back of ~S$1.1 billion in accretive acquisitions and strong rental escalations.

For context, the 10-year compound annual DPU growth rate (FY2016–FY2025) is approximately 6.0% per annum — significantly above the S-REIT sector average of ~2–3%.

If you’re tracking DPU across the sector, our S-REIT dividend yield calculator lets you model historical and forward yields for any REIT.

5. Portfolio Deep-Dive: 25 Data Centres Across 10 Countries

As at 31 December 2025, Keppel DC REIT’s portfolio comprised 25 data centres across 10 countries with total assets under management of approximately S$6.3 billion.

Geographic breakdown (by AUM):

- Singapore — 62.7%: The anchor market, housing flagship assets like the Keppel Data Centre Campus on Gul Circle (one of the largest carrier-neutral data centres in Singapore)

- Europe — 15.3%: Properties in the Netherlands, Ireland, UK, Germany and Italy

- Japan — 8.5%: Including the recently acquired Tokyo Data Centre 3

- Australia — 7.2%: Eastern Creek (Sydney) and Intellicentre Campus (Canberra)

- Other Asia — 6.3%: Malaysia and South Korea

Portfolio quality indicators:

- Occupancy: 95.6% (1Q 2026) — robust, though slightly below the 98%+ seen in prior years as the REIT strategically repositions some assets for hyperscale tenants

- WALE: 6.5 years by lettable area — providing strong income visibility

- Rental reversions: +51% in 1Q 2026 — driven by legacy below-market contracts being renewed at current rates

- Client mix: blue-chip tenants including major cloud service providers, internet enterprises, financial institutions and government agencies

The Singapore-heavy portfolio weighting is a strategic advantage — Singapore is one of Asia’s top data centre hubs with constrained land supply, a strong regulatory environment, and proximity to Southeast Asia’s fastest-growing digital economies.

6. Balance Sheet & Gearing Analysis

Keppel DC REIT maintains a conservative balance sheet with aggregate leverage of 35.1% as at 1Q 2026 — well below the MAS regulatory limit of 50% and the higher cap of 60% for REITs with ICR ≥ 2.5×.

| Balance Sheet Metric | Value |

|---|---|

| Aggregate Leverage | 35.1% |

| Average Cost of Debt | 3.0% |

| Debt Headroom (to 50% limit) | ~S$531M |

| NAV per Unit | S$1.71 |

| Interest Rate Hedging | Active hedging programme |

The 35.1% gearing provides approximately S$531 million of debt headroom for future acquisitions — critical given the REIT’s active acquisition strategy (S$1.1 billion deployed in FY2025 alone). The average cost of debt fell to 3.0% in FY2025, supported by favourable floating rates as SORA trended down to ~1.1%.

For a deeper dive into how gearing impacts REIT safety, try our S-REIT Gearing Ratio Calculator.

7. Growth Catalysts: AI, Hyperscale & Rental Reversions

Keppel DC REIT is uniquely positioned to benefit from three structural growth catalysts:

1. AI Compute Demand

The explosion in generative AI training and inference workloads is driving unprecedented demand for data centre capacity. Singapore — as Asia’s premier data centre hub — is seeing major investments from hyperscale cloud providers (AWS, Google Cloud, Microsoft Azure). Keppel’s Singapore-heavy portfolio (62.7% of AUM) captures this demand directly.

2. Hyperscale Pivot

Management has signalled a strategic pivot towards hyperscale-ready assets, repositioning some facilities to serve the largest cloud tenants. While this may temporarily impact occupancy during transition, it unlocks significantly higher rental rates and longer lease terms.

3. Rental Reversion Tailwind

The 51% rental reversion achieved in 1Q 2026 highlights the substantial mark-to-market opportunity in legacy leases. Many of Keppel DC REIT’s older contracts were signed at rates well below current market — as these expire over the next 2–3 years, organic DPU growth should remain robust even without acquisitions.

4. Sponsor Pipeline

Keppel Ltd, the REIT’s sponsor, has a significant pipeline of data centre development projects across Asia Pacific. This provides a right-of-first-refusal pipeline for future acquisitions at attractive pricing — a key competitive advantage.

8. Peer Comparison: How Does Keppel DC Stack Up?

Among Singapore-listed REITs with data centre exposure, Keppel DC REIT stands out for its scale, geographic diversification and DPU growth consistency:

| REIT | Yield | Gearing | P/NAV | AUM |

|---|---|---|---|---|

| Keppel DC REIT | 4.4% | 35.1% | 1.38× | S$6.3B |

| Digital Core REIT | 7.2% | ~32% | ~0.8× | ~US$1.5B |

| CapitaLand Ascendas REIT* | 5.6% | ~37% | ~1.1× | S$17.0B |

| Mapletree Industrial Trust* | 5.4% | ~39% | ~1.1× | S$9.0B |

*CLAR and MIT have diversified portfolios including but not limited to data centres

9. Key Risks to Watch

No investment is without risk. Here are the key factors that could impact Keppel DC REIT’s share price and DPU:

1. Valuation Premium Risk

At P/NAV of 1.38× and a trailing yield of 4.4%, Keppel DC REIT is priced for perfection. Any disappointment in DPU growth — or a broader de-rating of growth-style REITs — could trigger a sharp correction.

2. Interest Rate Sensitivity

While SORA has trended down to ~1.1%, global interest rate volatility (driven by US Fed policy, Trump tariff uncertainty, and persistent inflation in some economies) could push borrowing costs higher. The REIT’s average cost of debt of 3.0% provides some buffer, but rising rates compress yield spreads.

3. Tenant Concentration

Data centre REITs often have fewer, larger tenants than traditional REITs. A single tenant non-renewal or downsizing could have an outsized impact on revenue — particularly during the hyperscale repositioning phase.

4. Technology & Obsolescence Risk

Data centres require continuous capital expenditure to stay current. Older facilities may need significant investment to support next-generation AI/GPU workloads — eating into distributable income.

5. Geopolitical Exposure

With properties across 10 countries including Europe, the REIT is exposed to cross-border regulatory changes, currency fluctuations and geopolitical risks — though Singapore’s 62.7% anchor provides stability.

10. Should You Buy Keppel DC REIT in 2026?

Keppel DC REIT is a high-quality growth REIT trading at a premium valuation. The investment case rests on three pillars:

Bull case:

- AI-driven data centre demand is structural, not cyclical — lease-up timelines are shortening across Asia

- 1Q 2026 rental reversions of +51% signal a multi-year organic DPU growth runway

- Conservative gearing (35.1%) with S$531M acquisition headroom + Keppel sponsor pipeline

- 10-year track record of DPU growth — FY2025 DPU of 10.381¢ is an all-time high

Bear case:

- 4.4% yield is below the S-REIT average (~5.7%) — income-focused investors can find better yield elsewhere

- P/NAV of 1.38× leaves limited margin of safety if macro conditions deteriorate

- Hyperscale repositioning creates near-term occupancy uncertainty

Our take: For investors with a 3–5 year horizon who prioritise DPU growth over current yield, Keppel DC REIT remains one of the strongest secular growth plays on the SGX. The AI compute tailwind, rental reversion opportunity, and sponsor pipeline provide multiple DPU growth levers that most traditional S-REITs simply don’t have.

If you’re building a diversified S-REIT portfolio, consider pairing Keppel DC REIT (growth) with higher-yielding names like ESR-LOGOS REIT (9.4% yield) or Starhill Global REIT (6.6% yield) for a barbell strategy.

To model how Keppel DC REIT’s DPU growth compounds in your portfolio, use our Dividend Portfolio Yield Calculator or Compound Interest Calculator.

11. Frequently Asked Questions

FAQ — Click to expand

What is Keppel DC REIT’s current share price?

As at 16 April 2026, Keppel DC REIT (SGX: AJBU) trades at approximately S$2.36 per unit.

What is Keppel DC REIT’s dividend yield?

Based on the FY2025 DPU of 10.381 cents and a unit price of S$2.36, the trailing dividend yield is approximately 4.4%. Forward consensus yield for FY2026 is estimated at 4.7–4.9%.

How many data centres does Keppel DC REIT own?

As at 31 December 2025, the REIT owns 25 data centres across 10 countries in Asia Pacific and Europe, with total assets under management of approximately S$6.3 billion.

Is Keppel DC REIT a good buy in 2026?

Keppel DC REIT offers strong DPU growth (FY2025 +9.8%, 1Q 2026 +13.2%) and exposure to the AI-driven data centre boom. However, its 4.4% yield and P/NAV of 1.38× price in significant growth expectations. It suits investors seeking capital appreciation and DPU growth over pure yield.

What is Keppel DC REIT’s gearing ratio?

As at 1Q 2026, aggregate leverage is 35.1% — well below the MAS regulatory limit of 50%. This provides approximately S$531 million of debt headroom for future acquisitions.

Does Keppel DC REIT benefit from AI demand?

Yes. Keppel DC REIT is a direct beneficiary of AI compute demand, which is driving unprecedented growth in data centre capacity requirements across Asia Pacific. Its Singapore-heavy portfolio (62.7% of AUM) is especially well-positioned as Singapore is Asia’s premier data centre hub.

This article was researched with the help of AI. While we strive to keep all information accurate and up to date, there may be errors. If you notice any discrepancies, please contact us.